#AnthemBiosciences

Anthem Biosciences: The Invisible Engine Behind the World's Next Blockbuster Drugs

The Problem & The Bet

Every few years, a small biotech in Boston or San Francisco announces something extraordinary — a new molecule, a potential cure, a drug that could change medicine. The VC money follows fast. But then comes the question nobody mentions in the press release: who is actually going to make this molecule?

Building a drug is not just chemistry. It is a manufacturing problem of brutal complexity. The molecule needs to be reproduced identically, at industrial scale, in facilities that can pass inspections by the US FDA, the European Medicines Agency, and Japan's PMDA. Most biotech startups have neither the infrastructure nor the expertise to do this. Building it themselves would cost hundreds of millions and take a decade.

This is exactly the gap that Ajay Bhardwaj saw in 2006.

A marketing veteran with over three decades at Biocon, Bhardwaj had watched global pharma from the inside long enough to spot two things simultaneously: Western biotech desperately needed trusted manufacturing partners for their most sensitive molecules, and India had a deep pool of PhD chemists and molecular biologists who could do the same work as their counterparts in New Jersey or Basel at a fraction of the cost. He founded Anthem Biosciences in Bengaluru with a team of fellow Biocon veterans — including Dr. Ganesh Sambasivam, a PhD organic chemist who became the company's CSO — and made a deliberate, contrarian bet: no generics, ever. Only innovator molecules. Only the new, the novel, the patented.

What Bhardwaj understood — and what makes Anthem's business so durable — is what happens once you win a client at the discovery stage.

Anthem's chemists develop the synthesis process for the molecule, document every step, and manufacture clinical batches for Phase I, II, and III trials. At that point, Anthem's facility gets coded directly into the client's regulatory filing with the FDA. Switching to another manufacturer then becomes a regulatory event, not a business decision — requiring a formal amendment, new bioequivalence studies, fresh inspections, 18 to 24 months of delay, and $2 to $5 million in direct costs. Almost no client ever does it.

So they stay. And as the drug succeeds commercially — often after the original small biotech gets acquired by a Pfizer or a Roche — Anthem transitions seamlessly from development partner to commercial API supplier for a global blockbuster. The small contract becomes a long, compounding revenue stream. Over 50% of Anthem's revenue today comes from molecules it originally helped discover years ago. The stickiness is not a feature. It is the entire business model.

The Moat

Anthem's moat rests on five interlocking pillars. Entry barriers are brutal — a greenfield CRDMO requires ₹600–1,200 crore upfront and 36–48 months just to clear regulatory site certifications. Once inside a client's drug filing, switching costs make exit prohibitive: 18–24 months and $2–5 million to change suppliers. On the production side, Anthem runs India's largest fermentation infrastructure at 142 kL — six times its nearest rival — staffed by 1,000+ scientists at 75% lower cost than Western equivalents, driving EBITDA margins of 43%+ against Syngene's ~27%. Its IP sits not in product patents but in proprietary process trade secrets and customised cell lines that cannot be reverse-engineered. And the moat is widening, not holding — each new commercial molecule hardcoded into a client's global regulatory filing deepens the lock-in further, while Unit IV expansion into GLP-1 peptides and ADCs moves Anthem into even higher-barrier territory that most competitors cannot follow.

Overall verdict: Wide moat. 10+ year competitive advantage period.

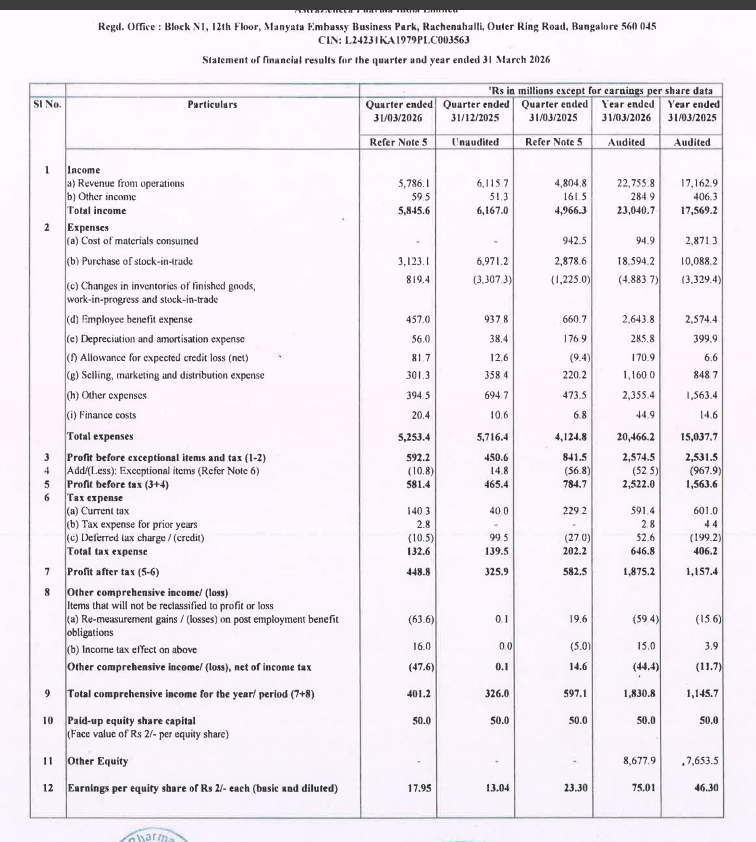

The Numbers Behind the Story

FY26 revenue: ₹2,124 crore. EBITDA: ₹990 crore at a 46.6% margin — against management's own guidance of 38–40%. Net profit: ₹591 crore. Free cash flow: ₹633 crore. Debt-to-equity: 0.05x. The business is essentially self-funding its own expansion.

ROIC of 29.1% against a WACC of 11.2% — that 18-point spread is the arithmetic of genuine competitive advantage.

The forward story is where it gets interesting. EPS grows from ₹10.51 in FY26 to a projected ₹17.75 by FY28 as Unit IV capacity absorbs and new commercial molecules scale. At ~₹770, the stock looks expensive at 71x trailing — but compresses to ~43x on FY28 earnings. For a business with these margins, this moat, and a $51B biologics CDMO TAM growing at 11–13% annually, that forward multiple is what you are paying for.

The runway is long. Anthem's current market share across its addressable segments is under 0.35%. The capacity to grow without diluting quality is already being built.

The People Running the Engine

Scientists, not financiers. That is the first thing that sets Anthem's management apart.

CEO Ajay Bhardwaj spent 35 years inside pharma before building Anthem. CSO Dr. Ganesh Sambasivam runs 1,000+ scientists doing chemistry most competitors cannot touch. COO K.R. Ravindra keeps the factories certified and the audits clean. This is an operator-led business, not a promoter-managed one.

Skin in the game is real: 68% promoter holding, zero shares pledged, compensation capped below 4.5% of net profits, related-party transactions under 0.8% of sales. The governance architecture is clean — 50% independent board, credible auditors, transparent segment disclosures.

There was a tax survey in earlier years and a ₹25.4 crore one-time labor code provision in FY26. Neither moved the needle on profitability. Footnotes, not red flags.

The most telling proof: they guided 38–40% EBITDA. They delivered 46.6%. No fanfare. Just execution.

Closing Note:

Anthem is not a flashy business. It makes no consumer-facing drug, carries no famous brand, and courts no retail investor headlines. What it has built instead — quietly, over two decades, from an industrial corridor in Bengaluru — is a near-irreplaceable position inside the global drug supply chain.

Growth triggers to watch

Unit IV at Harohalli is the single biggest catalyst — 275 kL of new capacity dedicated to GLP-1 peptides and ADCs, the two hottest segments in global pharma. As those lines commission through FY27, six newly active commercial molecules move from development into full-scale supply, each one a compounding revenue stream. Europe regulatory approvals add an estimated ₹380 crore in incremental opportunity. And the China+1 tailwind — global pharma actively diversifying away from Chinese API supply — is structural, not cyclical. Anthem sits directly in its path.

Red flags to track

Customer concentration is the number that demands respect: top 5 clients generate 64–70% of revenue. One late-stage clinical failure among them creates instant, painful overcapacity. The DavosPharma channel amplifies this — a single commercial partner controlling over 50% of North American revenue is a single point of failure that no moat fully insulates against. Unit IV itself is a ₹1,200 crore bet; if GLP-1 or ADC timelines disappoint, that capacity sits idle and ROIC contracts sharply. And there is no public succession plan for three founding scientists who carry the bulk of the institutional knowledge, client relationships, and regulatory credibility the business is built on.

The bull case is straightforward: execution on Unit IV, stability in the top client base, and the GLP-1/ADC wave arriving on schedule. If those three things hold, the FY28 earnings trajectory makes the current valuation look reasonable in hindsight.

The bear case is equally clear: concentrated clients, a concentrated channel, and a capital-heavy expansion cycle — all arriving at the same time.

Watch the quarterly commentary on Unit IV commissioning milestones and Davos Pharma revenue contribution. Those two data points will tell you everything about whether the story is on track.

[Not investment advice, DYOR]

If a father bathes his children, both laugh. If a son bathes his father, both cry.

🎥 A Separation, one of the greatest films ever made in Iranian cinema

Solar Group Chairman Satyanarayan Nuwal receives Padma Shri

He deserves 10 more Padma Shri awards, a truly remarkable person, nationalistic who is contributing 200% for Atmanirbhar Bhārat

a lot of replies to this are "how do you compete against that?"

you don't. that's the point.

if you're getting into algo trading, you are not going to beat Jane Street at market making. you are not going to out-speed them on order book inefficiencies. you are not going to win at anything that requires sub-millisecond execution.

that is not how you win.

here's how you actually find something you can win in:

1. trade on higher timeframes where speed doesn't matter. trend following, momentum, mean reversion on daily or weekly bars, none of these require nanosecond execution.

2. go where the big funds can't. less liquid markets, newer asset classes, niche sub markets. the capital they manage is too large for those markets to matter to them, but they can matter to you.

3. harvest risk premiums. that doesn't get arbitraged away very fast and can persists because the underlying risk is real.

the biggest mistake I see newer algo traders make is spending months building something that "tries" to compete directly with firms like this. it's a fun project, but it's not going to work.

know which game you're playing. and more importantly, know which game you're not.

![ramesh_vd's tweet photo. #AnthemBiosciences

Anthem Biosciences: The Invisible Engine Behind the World's Next Blockbuster Drugs

The Problem & The Bet

Every few years, a small biotech in Boston or San Francisco announces something extraordinary — a new molecule, a potential cure, a drug that could change medicine. The VC money follows fast. But then comes the question nobody mentions in the press release: who is actually going to make this molecule?

Building a drug is not just chemistry. It is a manufacturing problem of brutal complexity. The molecule needs to be reproduced identically, at industrial scale, in facilities that can pass inspections by the US FDA, the European Medicines Agency, and Japan's PMDA. Most biotech startups have neither the infrastructure nor the expertise to do this. Building it themselves would cost hundreds of millions and take a decade.

This is exactly the gap that Ajay Bhardwaj saw in 2006.

A marketing veteran with over three decades at Biocon, Bhardwaj had watched global pharma from the inside long enough to spot two things simultaneously: Western biotech desperately needed trusted manufacturing partners for their most sensitive molecules, and India had a deep pool of PhD chemists and molecular biologists who could do the same work as their counterparts in New Jersey or Basel at a fraction of the cost. He founded Anthem Biosciences in Bengaluru with a team of fellow Biocon veterans — including Dr. Ganesh Sambasivam, a PhD organic chemist who became the company's CSO — and made a deliberate, contrarian bet: no generics, ever. Only innovator molecules. Only the new, the novel, the patented.

What Bhardwaj understood — and what makes Anthem's business so durable — is what happens once you win a client at the discovery stage.

Anthem's chemists develop the synthesis process for the molecule, document every step, and manufacture clinical batches for Phase I, II, and III trials. At that point, Anthem's facility gets coded directly into the client's regulatory filing with the FDA. Switching to another manufacturer then becomes a regulatory event, not a business decision — requiring a formal amendment, new bioequivalence studies, fresh inspections, 18 to 24 months of delay, and $2 to $5 million in direct costs. Almost no client ever does it.

So they stay. And as the drug succeeds commercially — often after the original small biotech gets acquired by a Pfizer or a Roche — Anthem transitions seamlessly from development partner to commercial API supplier for a global blockbuster. The small contract becomes a long, compounding revenue stream. Over 50% of Anthem's revenue today comes from molecules it originally helped discover years ago. The stickiness is not a feature. It is the entire business model.

The Moat

Anthem's moat rests on five interlocking pillars. Entry barriers are brutal — a greenfield CRDMO requires ₹600–1,200 crore upfront and 36–48 months just to clear regulatory site certifications. Once inside a client's drug filing, switching costs make exit prohibitive: 18–24 months and $2–5 million to change suppliers. On the production side, Anthem runs India's largest fermentation infrastructure at 142 kL — six times its nearest rival — staffed by 1,000+ scientists at 75% lower cost than Western equivalents, driving EBITDA margins of 43%+ against Syngene's ~27%. Its IP sits not in product patents but in proprietary process trade secrets and customised cell lines that cannot be reverse-engineered. And the moat is widening, not holding — each new commercial molecule hardcoded into a client's global regulatory filing deepens the lock-in further, while Unit IV expansion into GLP-1 peptides and ADCs moves Anthem into even higher-barrier territory that most competitors cannot follow.

Overall verdict: Wide moat. 10+ year competitive advantage period.

The Numbers Behind the Story

FY26 revenue: ₹2,124 crore. EBITDA: ₹990 crore at a 46.6% margin — against management's own guidance of 38–40%. Net profit: ₹591 crore. Free cash flow: ₹633 crore. Debt-to-equity: 0.05x. The business is essentially self-funding its own expansion.

ROIC of 29.1% against a WACC of 11.2% — that 18-point spread is the arithmetic of genuine competitive advantage.

The forward story is where it gets interesting. EPS grows from ₹10.51 in FY26 to a projected ₹17.75 by FY28 as Unit IV capacity absorbs and new commercial molecules scale. At ~₹770, the stock looks expensive at 71x trailing — but compresses to ~43x on FY28 earnings. For a business with these margins, this moat, and a $51B biologics CDMO TAM growing at 11–13% annually, that forward multiple is what you are paying for.

The runway is long. Anthem's current market share across its addressable segments is under 0.35%. The capacity to grow without diluting quality is already being built.

The People Running the Engine

Scientists, not financiers. That is the first thing that sets Anthem's management apart.

CEO Ajay Bhardwaj spent 35 years inside pharma before building Anthem. CSO Dr. Ganesh Sambasivam runs 1,000+ scientists doing chemistry most competitors cannot touch. COO K.R. Ravindra keeps the factories certified and the audits clean. This is an operator-led business, not a promoter-managed one.

Skin in the game is real: 68% promoter holding, zero shares pledged, compensation capped below 4.5% of net profits, related-party transactions under 0.8% of sales. The governance architecture is clean — 50% independent board, credible auditors, transparent segment disclosures.

There was a tax survey in earlier years and a ₹25.4 crore one-time labor code provision in FY26. Neither moved the needle on profitability. Footnotes, not red flags.

The most telling proof: they guided 38–40% EBITDA. They delivered 46.6%. No fanfare. Just execution.

Closing Note:

Anthem is not a flashy business. It makes no consumer-facing drug, carries no famous brand, and courts no retail investor headlines. What it has built instead — quietly, over two decades, from an industrial corridor in Bengaluru — is a near-irreplaceable position inside the global drug supply chain.

Growth triggers to watch

Unit IV at Harohalli is the single biggest catalyst — 275 kL of new capacity dedicated to GLP-1 peptides and ADCs, the two hottest segments in global pharma. As those lines commission through FY27, six newly active commercial molecules move from development into full-scale supply, each one a compounding revenue stream. Europe regulatory approvals add an estimated ₹380 crore in incremental opportunity. And the China+1 tailwind — global pharma actively diversifying away from Chinese API supply — is structural, not cyclical. Anthem sits directly in its path.

Red flags to track

Customer concentration is the number that demands respect: top 5 clients generate 64–70% of revenue. One late-stage clinical failure among them creates instant, painful overcapacity. The DavosPharma channel amplifies this — a single commercial partner controlling over 50% of North American revenue is a single point of failure that no moat fully insulates against. Unit IV itself is a ₹1,200 crore bet; if GLP-1 or ADC timelines disappoint, that capacity sits idle and ROIC contracts sharply. And there is no public succession plan for three founding scientists who carry the bulk of the institutional knowledge, client relationships, and regulatory credibility the business is built on.

The bull case is straightforward: execution on Unit IV, stability in the top client base, and the GLP-1/ADC wave arriving on schedule. If those three things hold, the FY28 earnings trajectory makes the current valuation look reasonable in hindsight.

The bear case is equally clear: concentrated clients, a concentrated channel, and a capital-heavy expansion cycle — all arriving at the same time.

Watch the quarterly commentary on Unit IV commissioning milestones and Davos Pharma revenue contribution. Those two data points will tell you everything about whether the story is on track.

[Not investment advice, DYOR]](https://pbs.twimg.com/media/HLeYFWUacAAq4mZ.png)