DATA: @Circle’s $USDC accounted for roughly 70% of adjusted stablecoin transaction volume in the first half of 2026, compared with about 25% for @Tether’s $USDT, according to Visa data.

Read the full story by Olivier Acuna on CoinDesk

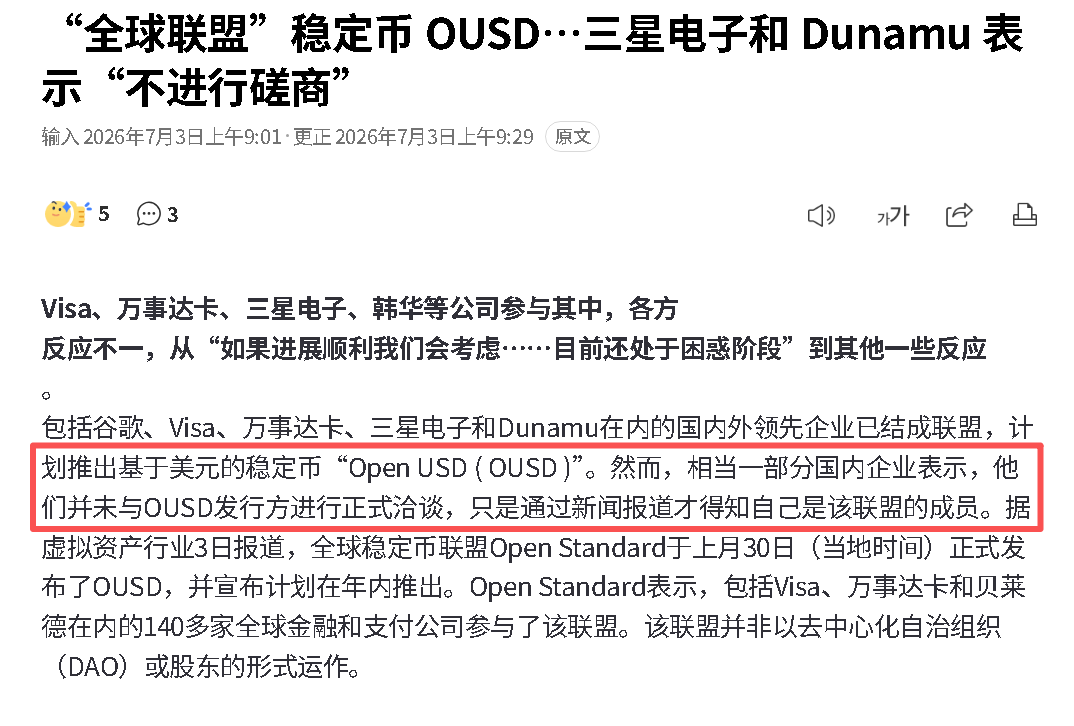

🚨BREAKING: KOREAN FIRMS DENY FORMALLY JOINING OPEN USD ALLIANCE

Several Korean companies listed as Open USD partners say they NEVER officially agreed to join, per Chosun Biz.

Samsung Electronics said it had "NO official talks and NO idea of what role" it would play.

Dunamu, K Bank and Shinhan said Open Standard only asked if they were interested, while one company rep said they only learned they were listed through Korean media.

Open Standard’s own site still lists major Korean names among its 140+ OUSD partners.

We’ve had lots of questions from our investor community looking for thoughts on OUSD, and so I thought I’d share my direct views here for anyone.

Stablecoin networks are platform and network effect businesses that are established over a long period of time, tend towards winner-take-most market structures, and resemble other internet platform utility markets. There are several layers that drive this.

First, stablecoin networks effectively act as public protocols and software layers on the internet and their network strength is a matter of the number and range of applications and services that integrate to the network. Every time a developer or service provider integrates to the network, it brings more network effects. This attracts more developers and adds more utility and more network effects. This then drives demand for the digital currency itself, which then reinforces these network effects through liquidity network effects.

We have realized this at a massive scale with the USDC network today — thousands upon thousands of services integrate with our network, which in turn provides immense utility not just to each application, but to users as a whole who benefit massively from the reach and interoperability that exists. This drives user and developer preference further. We’ve invested in building that ecosystem over nearly a decade, and now it’s accelerating as mainstream institutions come onto the network, connecting their customers and users.

We add to that utility by building software stacks that further expand and strengthen the network — protocols like CCTP and Gateway, which promote interoperability, safety and liquidity around the world. This expands the target surface area for app builders and developers, making it easy for them to tap into the liquidity and network effects that already exist. We are now seeing that stack get pulled into all kinds of chains, permissioned L2s, networks being built by governments, and so much more.

The second layer is that of liquidity network effects. This is fundamental. Liquidity begets liquidity. For a stablecoin to achieve scale and utility, it needs to be highly liquid, both on a primary basis (e.g., through all the major financial market centers in the world, with world class direct banking liquidity) and on a secondary basis both by being available and tradeable for retail and institutional clients in every geography and against every fiat instrument in the world. People who want to access and move value need to be able to easily get in and out of that digital currency. Here, we’ve invested nearly a decade in building out that liquidity, and it is now entrenched in exchanges, DeFI venues, and with PSPs, payments firms, regional exchanges, and so many others. Establishing these liquidity network effects also involves building global regulatory infrastructure and ensuring that the stablecoin is available under various regimes around the world. Today, USDC is in the top 3 most liquid digital assets in the world, and it falls off sharply after that. BTC, USDT and USDC have extraordinary liquidity. The closest other dollar stables are like 10x smaller and that liquidity tends to be concentrated in promotional books in a single exchange, whereas USDC liquidity is dispersed widely across dozens and dozens of surfaces. Building this liquidity has been a nearly decade-long task that we continue.

A third layer of network strength comes from the deep integration with the policy and regulatory environment — in many cases, years of effort to build licensing (e.g., USDC is the only large global stablecoin currently available in all of Europe or Japan), and more regimes for stablecoins are coming online, with Circle leading the way in ensuring that USDC is officially recognized, registered, licensed and accepted in the most important markets in the world. On the back of this is the work of building global banking, reserve management and treasury and liquidity management that can operate this on a nearly 24/7 basis in markets and banking systems globally. This globalization effort is a massive investment that we have made over the years.

All of these investments by Circle and our global ecosystem of thousands of partners have delivered the net result of providing the world’s most trusted and available digital dollar infrastructure—a utility that any user, developer, or business can freely and easily tap into. And we do not intend to slow down.

All of this compounds and shows in the numbers. In Q1 2026, according to third-party analysts (Artemis) who track stablecoin adoption, USDC handled nearly $30T in onchain transactions, representing 80% of all dollar stablecoin transactions on blockchains. USDT handled the remaining 20% of transactions. All of the combined remaining dollar stablecoins handled a total of 0% of transactions (i.e., < 0.5%). While other stablecoins may have some circulation, most of that is through promotions and incentives, the actual usage is extremely limited—because of the extremely limited liquidity and network utility that exists for these coins.

But my thoughts on the competitive landscape are not just about the strength of our network—there are also considerations around any new initiative.

Several perspectives and positioning have been shared about how something like OUSD improves on something like USDC.

1) Free mint and burn. The argument suggests that existing stablecoins charge burn fees, and payments firms should not need to pay these (despite the fact that the entire payment industry is built on small bps fees on various ingress and egress points on their networks). There are structural market realities built around the fact that some stablecoins impose very large redemption fees and have limited redemption facilities – the impact of this is that stablecoins with strong redemption facilities, good liquidity and no fees become the offramp for their competitor stablecoins. It may seem easy to say one will offer unlimited and free redeems, however market reality likely forces other behavior. This can be addressed – and is addressed by Circle – through contractual mechanisms vs. a blanket fee exemption.

2) Everybody wins and shares. While this sounds good in principle, the reality of the market and market opportunity is quite different. Today, Circle shares the majority of its income with its distribution partners, and we continue to lean hard into expanding those partnerships with leading companies across every sector of the market. However, we also retain significant income that allows us to invest in the massive market infrastructure that makes this such a powerful and valuable utility for the world to build on. Giving away all the income is a recipe for starving an infrastructure, systematically underinvesting and ensuring that your platform will remain limited in scope.

Furthermore, Circle believes that the future stablecoin market is likely several orders of magnitude larger than it is today. We’re actively bringing partners into the USDC ecosystem through a diverse and growing set of partnership models that span our work with exchanges, custodians, payments firms, asset issuers and more. We are excited to continue to build with a “big tent mentality” where the entire ecosystem can grow value together.

3) A consortium where everybody has a voice. Perhaps I have a cynical view, but the track record of consortium products achieving scale, P/M Fit or even basic product agility is absolutely dismal, and while there are examples of financial consortia that operate utilities, they are predictably slow moving. Large groups of large companies coordinate poorly, have misaligned incentives, slow things down and rarely create the space for real durable innovation and competitiveness. They also typically, out of their own self-interest, starve the consortium itself on an operating basis. We actually tried this in the early days of USDC, and even with a very small group, ran into endless challenges and complexity. Smaller, tighter strategic collaborations and commercial partnership arrangements with product and platform builders that can drive forward independently will almost always outcompete large consortiums. But oftentimes when these get formed, everyone feels like they should put their logo on the list, kiss the ring, and make noise about openness. But typically those same firms will turn to their operating units and make the best decisions for their customers, which often means partnering with the market leader and building durable win-win partnerships.

There’s also been a bunch of commentary on Circle's partnership with Coinbase and what this all means. Our stablecoin partnership with Coinbase remains as strong as ever, and I think we both see that enormous opportunity ahead to expand the USDC network.

A final comment: Circle remains committed to supporting a wide range of different products and infrastructures, even when we might compete with different aspects of those partners’ products in other areas of our business. With OUSD, we work closely with many of the founding members, and we expect that those same members will remain large USDC partners and customers. At the same time, as Circle has diversified our product and platform stack, expanding across Arc, CCTP, CPN, StableFX, Agent Stack and many other areas, we continue to expand the partnerships and collaboration with many other stablecoin issuers — dozens of them — to help them launch on Arc, leverage our interoperability infrastructure, get supported in our Wallets and become settlement and FX options on CPN and StableFX.

We are huge believers in growth in the stablecoin ecosystem and welcome OUSD as a new member of the community!

Every year we get our consortium style initiative around a stablecoin, we have seen this with Diem, Global dollar and now Open USD. While the set of players here is obviously potent, I remain highly skeptical any of these initiatives can hit scale.

A few thoughts on OpenUSD:

1. Liquidity and the cold-start problem. USDC and USDT have massive network effects across exchanges, payment processors, and brokers. This is always repeated but it's true, there are no BTC/sofiUSD pairs to trade on any of these exchanges or markets. These are not stableocin market makers and participants are willing to hold in size, as you can’t really use them anywhere.

The fair counter is that crypto markets will be far smaller than remittances or equities/bonds. Probably true, I suspect in the medium term, but those markets are still converging on the same stablecoins. Hyperliquid just struck a massive deal with USDC/Coinbase. Every tokenization initiative so far is built around the incumbents too.

2. A consortium of 500 rivals has no precedent for working. The pace of decision-making across 500 competitors is going to be glacial. Not everyone gets a board seat at Open Standard I imagine, so what happens when decisions cut against some of the players? Circle and Tether ship whatever they want, whenever they want, with zero commitment to anyone.

3. Regulatory and antitrust risk at scale. Circle and Tether are willing to absorb enormous pressure, they have being doing so for years. They hold hundreds of licenses they can use to arbitrage markets, Yes GENIUS act gave a lot of breathing room and clarity, but oversees, this is not the same story. The moment this gets hard under regulatory pressure, I think a lot of these partners just walk away. And a bloc of the largest banks and card networks jointly issuing money is an obvious antitrust target.

4. The "socialist" economics starve the issuer. Passing reserve revenue back to partners sounds great in practice, but what does Open Standard actually operate on? Little to no retained capital. People forget Circle doesn't just have marketplace/exchange partnerships; it funds a whole web of rebates across on/off ramps, stablecoin settlement, OTC desks, and more, with each deal being somewhat bespoke depending not he partner. Who funds that at Open Standard? Who decides which deals, on what terms, especially when the counterparty is a rival of an existing member?

Circle GAAP Opex for 2025 were 900M USD, if you strip out one time cost and IPO related cost, its adjusted OPEX is closer to 500M annually. Let’s say open Standard gets 25 bips, which is what other consortium did, At 10B of supply, open standard is making 25M a year… You don’t fund much with that…. You need to become huge very quickly.

5. The announcement is basically a giant LOI. Read the quotes: BlackRock calls it "a constructive step," BNY "looks forward to exploring ways to support," others say it's "interesting." Meanwhile the partners are backing rivals: Stripe owns Bridge and has its own stack, Coinbase is wedded to USDC, banks are building their own deposit tokens, and the card networks support every token out there. They'll hedge across all of them. Distribution only matters if it's exclusive — and it clearly won't be.

6. The "mint/redeem fees are a problem" claim is wrong. In practice every large institution minting and redeeming through Circle and Tether already gets big rebates. The real cost of moving money is FX, not mint/redeem and there's no moat there, because anyone can just match free mint/redeem.

All in all: one to monitor, but I'm deeply skeptical that an organization that looks like a DAO of 500 companies can move fast enough to matter long term. Who decides go-to-market? Capital allocation? Anything?

Ultimately this reminds me of the DAO experiment. The pitch was identical: no single owner, "neutral" governance, aligned incentives, decisions made collectively for the good of the network. In practice DAOs almost universally failed at the thing that actually matters: shipping. Governance turned into endless forum debates and token-weighted voting where nothing decisive got done, capital sat idle because no one could agree how to deploy it, and the projects that won were the ones with a clear owner willing to move fast and take risk. "Owned by everyone" almost always means accountable to no one. Open Standard is a DAO of competitors that are not really committed to anything, and I'd bet on the two operators who can ship unilaterally over a committee that has to ask 500 rivals for permission.

很多人把 Open USD 和 Circle 看成一场「联盟 vs 公司」的战争。

但我觉得真正的竞争,不是谁发行更多稳定币,而是谁能成为稳定币时代的底层支付网络。

Open USD 的优势是渠道、生态和巨头联盟。

Circle 的优势是产品、开发者体验、合规和已经跑通的基础设施。

联盟可以快速带来分发能力,但也会带来治理成本。单一公司可以更快迭代,但也必须面对巨头联盟的渠道压力。

所以问题不是:

Open USD 会不会杀死 USDC?

而是:

未来企业支付、AI Agent、跨境结算和链上金融,最终会默认接入哪一套基础设施。

稳定币只是资产。

支付网络、清算能力、开发者生态和合规体系,才是真正的护城河。

Stablecoin War 背后,本质是 Infrastructure War.

HOLD $CRCL