According to my estimates, $FUTU and $TIGR should be trading at 12-15x pro-forma earnings.

Having a lower operating leverage and higher mainland exposure, $TIGR is more heavily affected, while having a bigger leeway to further increase their revenue yield and to regain the leverage lost (their bottom line may be much more volatile than FUTU in the next 1-3Y). Any decrease in trading activity should hit TIGR the hardest. Using EV/EBI it’s crazy cheap, but that assumes management will activate their balance sheet meaningfully which I believe it’s highly unlikely since there are reserve requirements and leveraging doesn’t seem an option.

$FUTU is the better business with stronger growth prospects.

I’m not confident on the brokerage business as a whole in the next 1-2Y but believe in the long term growth runway.

@FriendlyCapMgmt@nicolas_a4 Indeed, potentially a much larger % earnings, no marketing needed, fixed OpEx, not sure if they had also different pricing since switching for them is harder than a regular customer.

All brokers are trending to zero commission, it's mainly interest, IPOs, management fees, etc.

@FriendlyCapMgmt Likewise, my estimates were at 15-20% max. MoS shrank significantly in this release. Customer acquisition is also slowing down quarter after quarter.

So far no new market was announced, nonetheless $TIGR can take customers from ~99 countries even though they don't actively market themselves there and don't have a local entity.

There used to be a tiny amount of users from Malaysia + SEA, which should be currently booked through NZ, although this depends from each customer's agreement. Marketing in these countries doesn't seem to break-even as of today, according to FUTU. TIGRs lower operating leverage should make this expansion even less profitable.

An extract from their FY2025 report:

"For consolidated accounts, we carry out customer due diligence... pursuant to the anti-money laundering rules and regulations in New Zealand (...) under consolidated accounts, the Group... recognizes revenue... on a gross basis as the Group is determined to be the primary obligor" (Tiger NZ is the broker of record for most RoW, although this isn't explicitly/clearly disclosed. NZ local customers are a small portion of the NZ booked revenue)

Worth noting is, they have registered trademarks (not licenses) in Malaysia, Indonesia, India, Philippines, Thailand and in the EU.

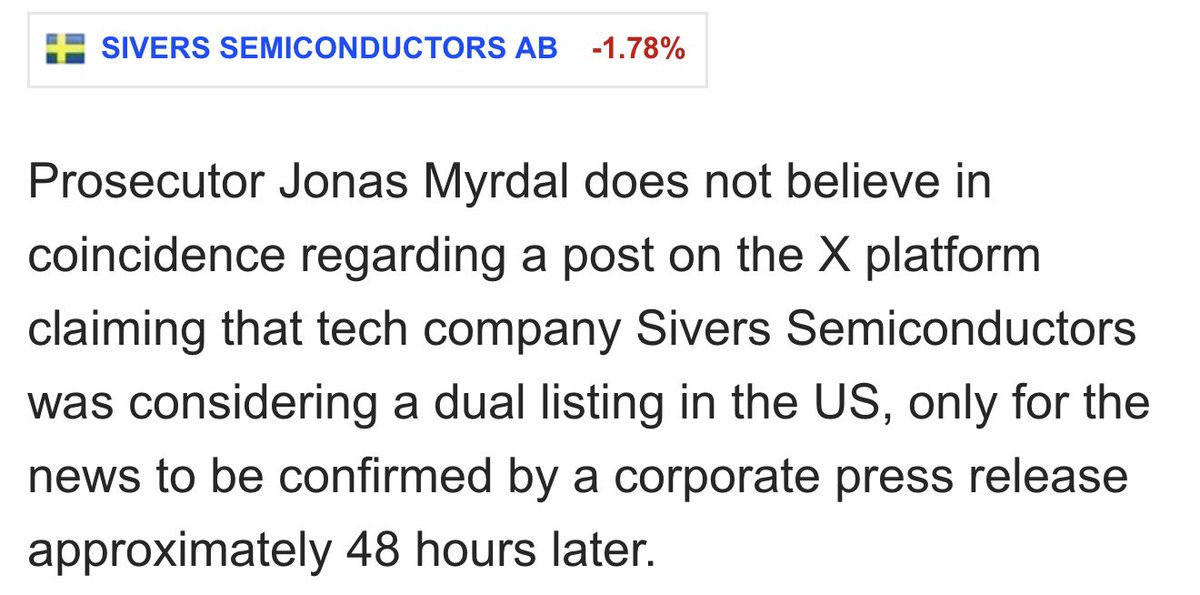

@BillieBillion1 Absolutely insane, funny how they basically re-announced a partnership that was years old already. Not sure at what point of the EV/Pipeline we are haha.

So far no new market was announced, nonetheless $TIGR can take customers from ~99 countries even though they don't actively market themselves there and don't have a local entity.

There used to be a tiny amount of users from Malaysia + SEA, which should be currently booked through NZ, although this depends from each customer's agreement. Marketing in these countries doesn't seem to break-even as of today, according to FUTU. TIGRs lower operating leverage should make this expansion even less profitable.

An extract from their FY2025 report:

"For consolidated accounts, we carry out customer due diligence... pursuant to the anti-money laundering rules and regulations in New Zealand (...) under consolidated accounts, the Group... recognizes revenue... on a gross basis as the Group is determined to be the primary obligor" (Tiger NZ is the broker of record for most RoW, although this isn't explicitly/clearly disclosed. NZ local customers are a small portion of the NZ booked revenue)

Worth noting is, they have registered trademarks (not licenses) in Malaysia, Indonesia, India, Philippines, Thailand and in the EU.

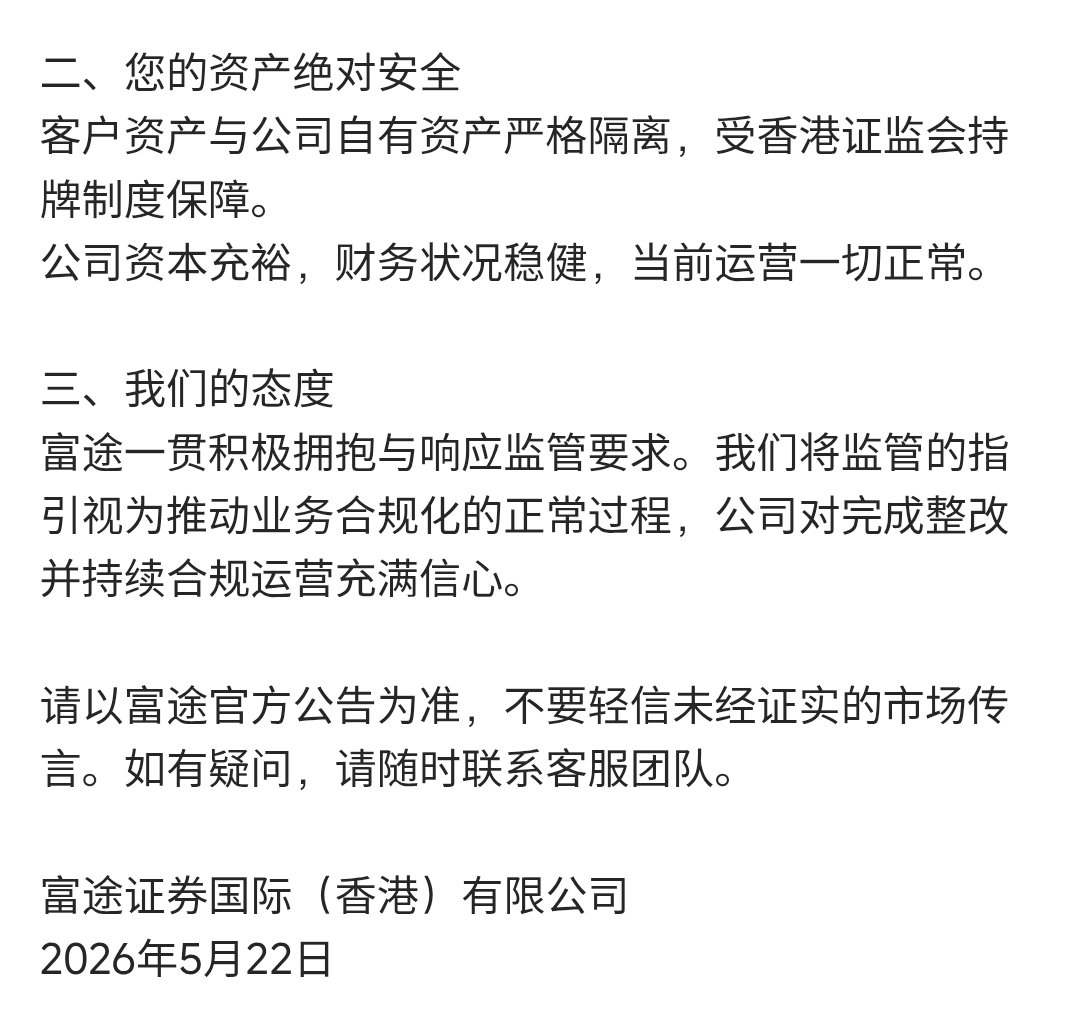

@BillieBillion1 Any thoughts on the EBM investigation for insider trading?

Didn't do too much research but looks like this one has high chances for getting suspended.