I vividly remember you doing this and I also recall thinking, “what 20-something-year-old even thinks about doing this?” Definitely a harbinger of things to come.

$FOUR Trades at the cheapest Trailing Gross Profit ratio at 3.7x than any time in its history by a multiple factor of 2-3x

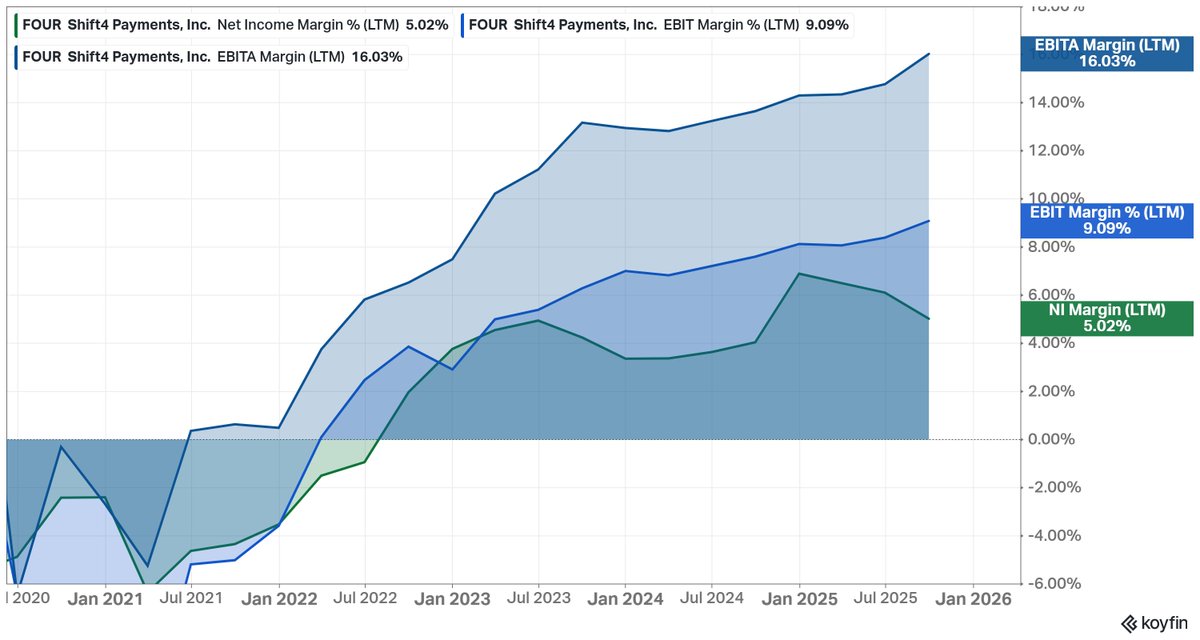

I've never really seen a business transition from 20-25% gross profit margins to 35-40%+ sustainable gross profit margins, with the potential to increase further...

In that same time, the stock price is level. EBITA margins to account for M&A non-cash write downs has underlying consolidated business unit economics increasing from barely profitable to converting 50%+ of Gross Profit to EBITA from 5% to 19%, that is all being aggressively reinvested via: Organic Growth, M&A, and buybacks

Today, the business trades at the lowest valuation multiple on every key margin metric, except for net income (PE). However, on all the real business tracking unit economic measures, it's actually probably 50-75% more profitable on an underlying basis than it's actually trading, once you add back M&A non-cash expenses for amortized asset write-downs

If you were to take off Goodwill from the balance sheet ($2.5B vs $9B in Total Assets) and increase net income margins to even 7.5%... this business is producing ROE of 30% from the actual LTM value of 14% that is baked into results. This also takes no margin improvement from GB or forward growth, both of which seem extremely probable after this quarter's ridiculous incremental 500 bps improvement on EBITA margins Y/Y after one quarter of Global Blue luxury processing and Tax-free product margins

This is why management just announced a $1B repurchase agreement. The company is trading at around "real" 10-12% forward cash flow margins and it can nearly fund the buyback from cash flows that reduces diluted shares outstanding 17% with the $6B diluted market cap valuation

However, management also indicated that capital allocation is one of their strengths. Hence, issuing 5.5% EUR denominated convertible notes expiring in 2033 so acquire the stock at a higher yield than the notes with all the organic growth not even baked in. They'll purchase a significant amount of stock and negate the dilution from nearly the past 5-years

This $FOUR management team is building a behemoth right in front of our eyes and it's trading at the same price as 5-years ago when it first came on my radar

I'm buying long dated calls on this. I think it rerates and quickly, and I want to own the equity long-term as the business quality gets recognized over the following 2 year timeframe

this excerpt from Einhorn is one of the cleanest summaries of equity investing; esp why "good business" and "good stock" are not the same

"Really bad things happen to earnings when a 25% ROE turns into a 10% ROE. Great things happen to earnings when a 10% ROE becomes a 15% ROE."

Great video from @mjmauboussin on Intangibles and Modern Value Investing

On why we should care about this topic, and another reason why you need to be careful when looking at the S&P 500 multiple today compared to the past

"If we apply these data adjustments to the S&P 500, our analysis indicates that S&P earnings are actually 10% to 15% higher than what's reported as stated operating earnings.

This automatically means that multiples are around 10% lower than their headline figures. Therefore, when comparing historical data, it's crucial to be mindful that you're not always comparing "apples to apples" beyond a certain point."

🧵The S&P500 is notoriously difficult to beaT, especially in quant strategies.

But a factor that shines? Return on Invested Capital (ROIC)

Take 50 $SPY stks with highest ROIC (trail'g):

CAGR 16% vs $SPY 13%

Last 10 yrs (qtr rebal, eq weight), allowance for intangibles.

👇

1/ Chris Hohn (TCI) spoke at the recent Norges conference (starts at 1h45: https://t.co/w9lHcU2WOx). +9% alpha per year over 21 years. His talk was a rare, clear window into to scale public markets alpha at institutional size. Here’s what stood out:

$ABB

Interesting slide from ABB, Investor’s largest holding

Plans to spin-off Robotics division, will make the reminding ABB group have 19% EBITA margin and 24% ROCE. Not that many industrial companies with that combination.

ABB also spun off Accelleron in 2022

Management expect 2025 to deliver mid-single digit top line growth and further EBITA margin improvement + book to bill >1

If you've ever wanted to easily search my @mjmauboussin index, @CogniCarbon built a custom GPT on all 170+ of his research papers over 30 years across CS First Boston, Legg Mason, Credit Suisse, Blue Mountain, and Counterpoint.

Check it out here:

https://t.co/igLQDa8kKB

https://t.co/NJdi8QkQaE

Time to get long Russia? Head of Russian sovereign wealth fund saying sanctions will be lifted and US companies returning. Hmmm

@theone34824249@stonkmetal reasonable multiple for quality and growth - market doesn't love that it's a little levered and they didn't generate much FCF last year but that was b/c of one-off growth investment - should be like 7% fcf yield on 2-3 years out

@theone34824249@stonkmetal Aircraft maintenance repair and overhaul (MRO). IPO'd last fall (Carlyle portfolio company). Lots of secular tailwinds related to commercial aviation growth, high return on tangible capital, recurring revenue and moat-esque advantages related to technical expertise