@PrimaryVision and I are launching a new show called "Third Party Opinion" where we will cover everything from U.S. shale and domestic activity to global macro economics. This will be the full round up you don't want to miss!

Trucking spot rates have never moved up this fast, ever - including early COVID.

The weekly average for truckload spot rates moves to a new all-time high of $3.71/mile.

It took 43 weeks for spot rates to increase by $1.38/mile during early COVID (April - Feb 2021).

It has taken only 29 weeks to achieve the same increase (Nov 2025 - June 2026).

For those that called it "Arab Spring", the rest of the world called it "wheat wars." Don't be shocked when theirs a global food shortage in the next 18 months.

Breaking News: 🚨🚨🚨

Market chatter is building that China is actively price-checking — and selectively buying — U.S. corn and sorghum. The rumors have legs.

Heavy rains damaged northern China's corn crop, leaving large quantities moldy and unusable. Domestic corn prices are up ~10% year-over-year, squeezing feed producers and making imports increasingly attractive.

Chinese buyers have booked at least 3.0 MMT of U.S. sorghum in recent months, roughly 3x all of 2025

Chinese buyers have booked 500K of Argy Corn in the last week.

July Corn CIF was up 5 to 90N yesterday.

SONAR’s truckload rejection rates surge overnight to cycle highs: 16.36%.

Capacity is tighter today than it was during Roadcheck week or Memorial Day.

As we heard yesterday on FreightWaves Today, Estes and the Port of LA are seeing higher demand coming from consumer retail freight than forecasted earlier this year.

🇺🇸U.S. corn and soybean health is below both analyst expectations and recent averages. Spring wheat ratings fell below all pre-report estimates.

Corn and soybean planting is wrapping up, and winter wheat harvest has just begun.

This is a significant story. There are many carriers that exclusively rely upon CH Robinson for freight. They will be looking for new brokers to work with.

https://t.co/jvfEDXhNs0

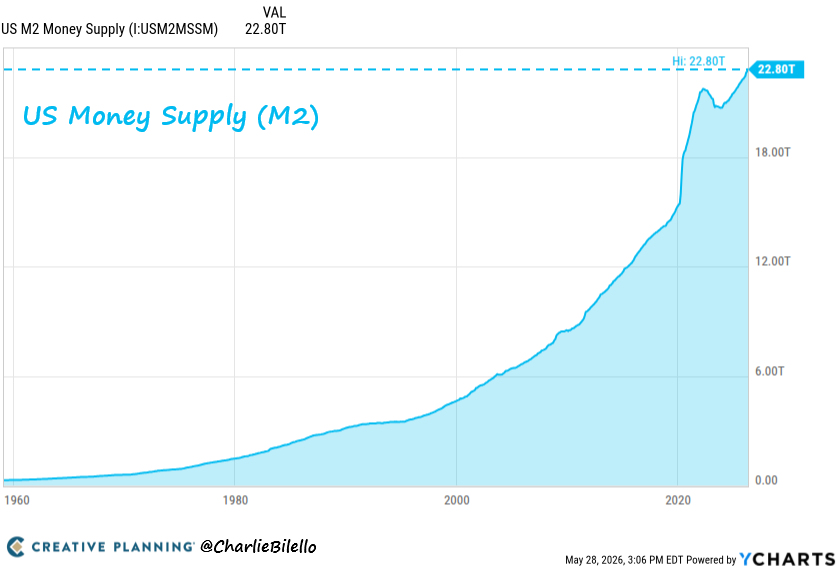

It's amazing to see Univ of Michigan data on Consumer Confidence hitting all time lows, but confidence in the stock market is at all time highs. Free money and QE really broke people's view of reality.

The Fed expanded the money supply by nearly $9 trillion under Powell.

Inflation has averaged >4% per year over the past 6 years.

Powell's explanation? It was nearly all due to rolling “supply shocks" over which the Fed has no control.

The truth: this inflation was made in Washington as it always is - from too much government borrowing/spending and too much government creation of money.

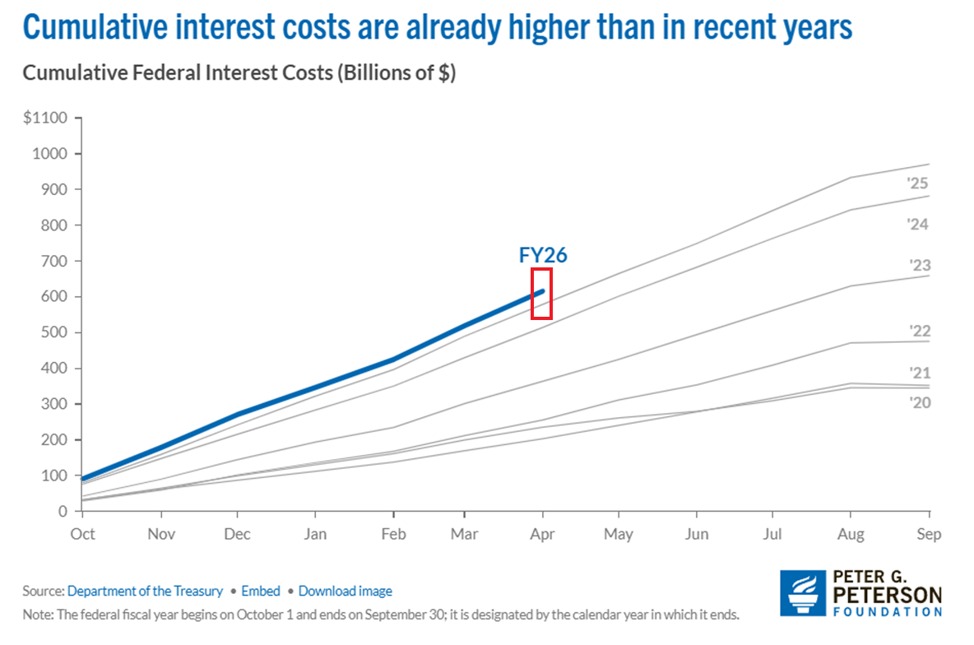

We are on an unsustainable fiscal path:

Interest costs on US public debt rose +$37 billion YoY in the first 7 months of FY2026, or +6.4%, to a record $616 billion.

Interest has more than TRIPLED for this time of the year since 2021.

As a result, interest payments are now the fastest-growing portion of the entire federal budget and the 2nd-largest spending category, surpassing Defense and Medicare, only behind Social Security.

The Congressional Budget Office projects annual net interest payments to more than DOUBLE from $1.0 trillion in 2026 to $2.1 trillion by 2036.

Over the next 10 years, interest costs are expected to total a massive $16.2 trillion.

As a proportion of GDP, interest is projected to reach 3.2% this year, surpassing the previous record set in 1991, and surging further to 4.6% of GDP by 2036.

The cost of US government debt has never been this high.

⚠️US student loan CRISIS is deepening:

Delinquent federal student loan debt jumped +$12.2 billion in Q1 2026, to a record $171.4 billion, surpassing the prior peak of $166.8 billion set in Q4 2019.

This figure has DOUBLED since 2012, reflecting a decade-long deterioration in the ability of borrowers to service their debt.

This comes as 2.6 million borrowers defaulted on student loans in Q1 2026 alone, following 1.0 million in Q4 2025.

The average borrower entering default is now nearly 40 years old, up from 36.4 before the 2020 pandemic, meaning the student debt crisis is increasingly hitting middle-aged Americans, not just recent graduates.

The student debt crisis shows no signs of easing.

I’ve been grinding away trying to map out China’s recent crude plays, but after going through today's report, I have to hand it to OIES—they scripted the plumbing way better than me.

Here is my quick breakdown after running through their print, alongside the Chinese refinery throughput chart to help connect the dots.

-

Three months into the Hormuz crunch, and Beijing is completely blindsiding the market with its crude playbook. A heavyweight that easily sucked in 11mb/d over the last five years just saw its import prints plunge to 9.3mb/d in April. Now, the forward data says May and June seaborne arrivals are about to crater straight into the gutter at 6.5mb/d.

Instead of running its usual playbook of panic-dumping the SPR to backstop the market during a supply crisis, Beijing just completely cock-blocked refiners from touching the strategic vaults, only greenlighting commercial stock draws.

To make it worse, refiners aren't even willing to bleed their own commercial inventories, while state traders are acting like total penny-pinchers—happily flipping premium WAF cargoes back into the market and hoarding dirt-cheap Russian barrels instead.

This is a complete 180 from the 2021 power crunch, when Beijing panicked and ordered everyone to grab supply 'at any cost.' The heavyweights and policymakers in Beijing clearly think they can outmaneuver this supply shock and keep the economic damage locked down by playing a few smart, tactical micro-levers.

China’s true red line for freezing out imports is hardwired to the scale of their run cuts. If they try to copy-paste their five-year average throughput of 14.1mb/d, the exact moment seaborne arrivals drop below 9.2mb/d, they’re trapped—they either have to open the strategic taps wide or start chasing expensive market barrels. Instead, chopping runs by 5% down to a 13.4mb/d baseline is hands-down their most realistic, long-term survival play.

In this setup, if domestic crude extraction and pipeline taps keep humming, they can easily coast for a few months without taking a single economic hit, even with seaborne prints scraping a measly 7.9–8.5mb/d, because transportation fuels like gas and diesel will still be taken care of.

However cranking run cuts to a nuclear 10% scenario means they could survive without chasing a single market barrel even if seaborne flows dry up to 7.2mb/d—but they'd have to throw petrochemical feedstocks like naphtha and LPG under the bus just to keep gas and diesel flowing, a desperate move that runs on borrowed time and stalls out after a few months unless the whole economy is in a total tailspin.

To micromanage this whole run-rate circus, China's refining complex is pulling a highly responsive lever: the yield shift.

Beijing explicitly told state majors like Sinopec and PetroChina to ditch chemical feedstocks and prioritize flooding the market with gas and diesel, and these plants immediately saluted by shifting their product yields by several percentage points on a dime.

As a result, the real bloodbath isn't happening at the refining gate—it's completely decimating the downstream petrochemical chain. With Hormuz blocked, their seaborne naphtha inflows were already sliced in half, but a 5% run cut is about to bleed domestic naphtha and LPG supplies by tens of millions of tons a quarter, sending a compounding, fatal shock straight through the petchem feedstock backbone.

They are keeping wheels turning by guaranteeing gas and diesel, but the squeeze on industrial chemical feedstocks is completely running on borrowed time.

To paper over the massive raw material hole in the petchem chain, Beijing is shoving its massive 'Coal-to-Chemicals' complex into the spotlight, branding it as a strategic shield against volatile crude under the 15th Five-Year Plan.

Thanks to dirt-cheap, stable domestic coal, inland plants churning out olefins and methanol are running hot to boost volumes, but this quick fix hits a hard ceiling when it comes to replacing lost barrels at scale due to structural bottlenecks.

The core infrastructure is trapped deep in the northwestern sticks like Inner Mongolia, meaning slamming those products down to the massive manufacturing teeth on the southeastern coast comes with a punishing logistics and freight premium.

Most importantly, coal gasification routes physically cannot clone key aromatics or specialized LPG chemical chains—the feedstock deficit is mathematically locked in.

On top of that, the fact that Beijing is sitting on a massive 1.1-1.3 billion barrel pile without tapping it proves that institutional red tape is locking up the plumbing.

The 100 million barrels buried deep in dark underground rock caverns—completely invisible to satellites—are almost entirely SPR, requiring endless red tape like complex auctions and market disclosures, so Beijing is hoarding it as a nuclear option.

Even for the commercial barrels that are accessible, refiners are terrified to draw down because plotting out the repayment timeframe to replace that crude is a total mathematical nightmare in this chaotic macro environment.

Beijing is pulling off a highly calculated micromanagement script here: they are completely freezing out the inventory draw requests from state-owned heavyweights like Sinopec, who are nakedly exposed to global benchmarks and were the first to aggressively slash throughput.

Instead, they are using the Shandong teapots as a human shield—handing these independent refiners tax breaks and strict run-rate mandates because they have the flexibility to stomach toxic, illicit Iranian and Russian barrels to cushion the margin bleed.

Bottom line, this entire web of macro levers—starving imports, shifting yields, hunting for distressed barrels, and burning through coal-to-chem assets—will keep the lights on and protect the economic skeleton through the peak of summer, but only under that tight 5% run cut baseline that keeps seaborne arrivals pinned at roughly 8mb/d.

But with May and June seaborne prints already locked in at a subterranean 6.5mb/d, the expiration date on this makeshift band-aid play cannot stretch into autumn.

Short of letting their entire national refining infrastructure suffer a catastrophic meltdown, Beijing is running straight into a hard physical wall.

Before late summer wraps up, they will be forced to either open the strategic floodgates and dump their massive stockpiles or make a frantic U-turn right back into the international physical market, chasing heavy volumes aggressively at any price.

#oott #iran

U.S. Credit Card Accounts delinquent by 90+ days have jumped to 13.1%, the highest level in 15 years and closing in on the highest level in history 🚨🚨🚨

Per a recent @Gallup poll, share of Americans who think economic conditions are getting worse rose to 76% in May (highest reading since May 2023) while only 20% say they are getting better

I had a fantastic time speaking at the Manhattan Alternative Investment Network Panel: Commodities in a Volatile Global Market. Here's the link of the discussion- https://t.co/FxDngPgXtq