@IggyOnInvesting Still following, @IggyOnInvesting ?

Recent industry data of the restaurant industry looks promising. Besides, Tomoyuki Izumi took a large position recently.

$DR.TO casually repurchased 6% of SO in a block trade at the end of May. The stock had its moment on fintwit a while ago, now I barely hear anyone mention it. Yet it's still executing, and it's still cheap

@david_katunaric You could look into $TVK.TO as a second order derivative in recovering transportation demand, where the share price did well in the past but isn’t yet reacting to a capex catch-up from the trucking companies.

@a_chhoy Really thoughtful threads @a_chhoy! How do you think about organic capital deployment? Capex almost quadrupled in the last 5 years with the gap between growth and maint. capex widening. TVK now also has reinvestment opps to drive organic growth which was absent in prior years.

Most investors think conviction means buying with confidence.

The harder part is what comes after — doing nothing while the market spends 12–18 months disagreeing with you.

$TVK.TO — up ~160% since my initial buy at ~C$50 in early 2024. Built to a top holding as Dustin Haw executed the serial acquirer playbook with discipline. Now grinding below the 200MA for the first time in years. 6–9 months of dead money. Every instinct says do something.

But EnTrans — $TVK.TO’s largest acquisition — is a cyclical business. Tank trailer weakness doesn’t last forever — next two earnings the key test. If the compounding machine underneath is intact, the staircase always resumes.

I believe real conviction lives in the waiting, not the buying.

$SPG.DE Solid Q1 2026. Further debt repayment and net leverage of 1.5x now at the lower end of the target range. The company could use its future free cash flow for buybacks which could boost the stock price meaningfully given the low free float. Disc.: long

$SPG $SPG.DE Springer Nature 1Q26 results are very solid. 6.2% organic growth, strong underlying operating profit growth (8%) and >€200m in FCF in 1Q26 alone. This should not be a double-digit fcf yield stock

$DBO.TO

Cinemark's revenue grew 19% YoY to $ 643m. $311 m of that was admissions revenue and DBOX seats grew their share of that 150bps to 5%(!!). Suggests royalties this quarter from just the CNK network alone will be on par with, if not succeed, total royalties YoY. CNK also added 86 DBOX auditoriums in the Q.

I find it notable that CNK is specifically highlighting metrics around DBOX performance in its press releases, while lumping all other PLFs together in a broader category.

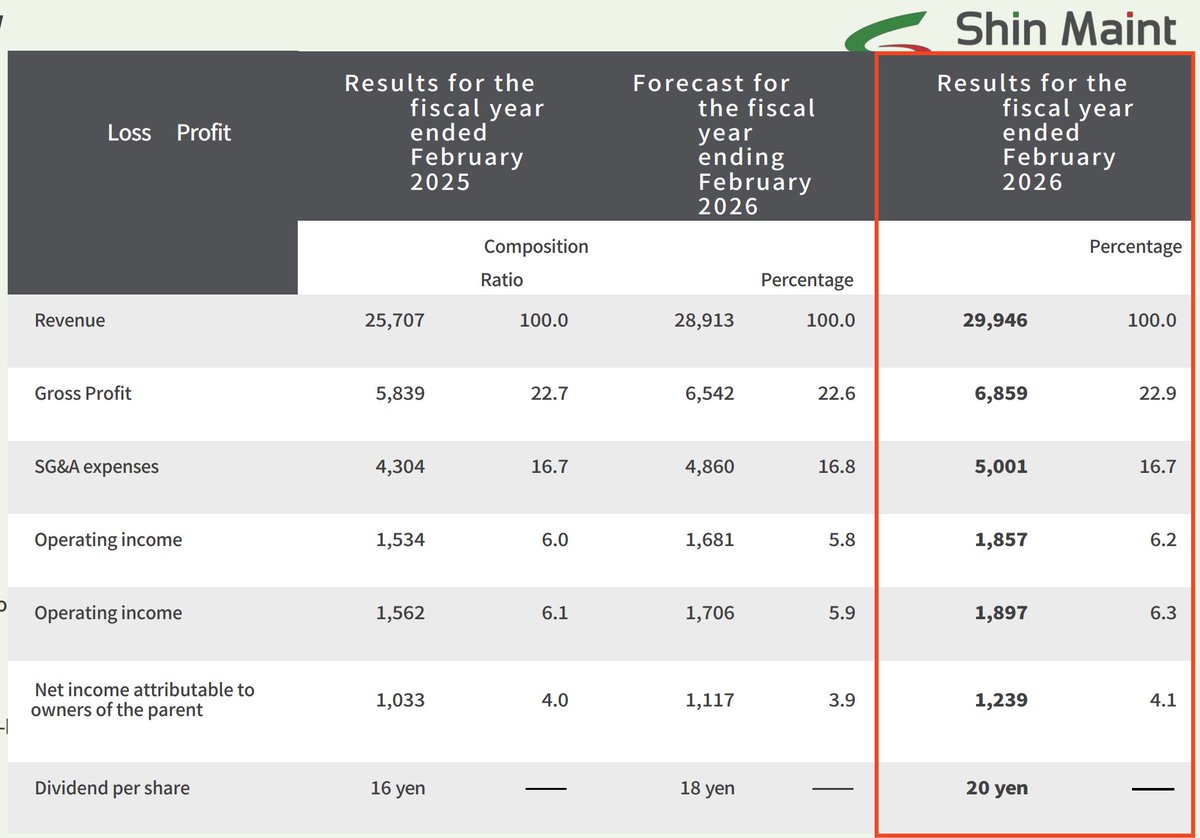

Outstanding FY26 Results for Shin Maint $6086.T

Once again forecasts are surpassed across the board, double digits are achieved in every metric.

Trades at:

8x LTM EV/EBIT

9x LTM EV/FCF

16x LTM MC/NI

Holds over 5% of market share, and owns 9% of its closest competitor.

One of the biggest reasons investors get excited about serial acquirers:

They solve the reinvestment problem.

In most businesses, good reinvestment opportunities are limited. You fund the core projects, maybe expand capacity, invest in product… and after that, the incremental dollar usually earns a lower return.

And cash starts to pile up.

Owners either return the cash to shareholders… or start stretching into lower-quality projects just to put the money to work.

Serial acquirers work differently.

Instead of relying only on internal projects, they build a repeatable machine to acquire businesses that meet strict return thresholds.

Do it well, and you create a long runway to keep deploying capital.

The cash doesn’t sit on the balance sheet.

It gets recycled into the next acquisition. And the next one.

In the best cases, the model allows you to reinvest close to 100% of free cash flow at high rates of returns for many years, even decades.

Excellent analysis by @JibbyCap regarding the favorable tailwinds for Terravest’s subsidiaries. Furthermore, defense contracts are beginning to scale and are expected to reach full capacity in 2026.

TerraVest $TVK.TO share price has been flat for about a year now. That shouldn't come as a surprise, as the valuation ran up a lot from '23-'25.

That said, I've been feeling pretty good about the underlying business lately. There are a lot of drivers pushing in the right direction right now:

* LNG production in Canada continues to ramp. This was already positive, but now even more so d/t the Hormuz situation resulting in an LNG supply crunch. This is good for BC nat gas production -> good for TVK's PE segment.

* Crude oil is up and might stay there for a while. Good for PE, and especially Services. (Although there is a slightly counter-cyclical effect here for propane, as higher crude oil prices result in higher propane prices, which reduces demand.)

* Propane is now in a stronger position domestically as the 'electrify everything' trend has died off. In addition, a harsh winter plus an already existing desire for fleet renewal should provide a positive backdrop for compressed gas.

* US trucking rates are increasing -> positive for trailer demand.

* C-store buildout, data center buildout -> positive for HT/composites.

* The NA chemical sector appears to be inflecting a little bit. This is now being supercharged by the war in Iran, as global competitors are having a rough time sourcing cheap feedstock from the Middle East. Not saying 'the cycle has turned', but at the moment it seems like a hopeful time to be selling chemical containment equipment in North America, where feedstock is cheap and plentiful.

TerraVest has operated in a hostile environment for most of its 'modern' history, usually due to low oil/gas prices or political hostility toward fossil fuels. (E.g. cancelled oil pipelines, drilling permit freezes, heat pumps being subsidized to replace propane heating, increasingly stringent gas/oil boiler efficiency requirements, etc etc etc.) Yet even then TVK thrived. And now it appears that many of those factors are inflecting.

Execution was wonderful when conditions were poor -- what will it be like when the demand backdrop flips?

@longonlybets Thank you for your quick reply. I have the same issues with valuation now. Bel Fuse went from the dog to top of the breed valuation-wise in lockstep with improved financials. But deserving an Amphenol-like valuation demands more than just right-sizing the company.

TerraVest $TVK.TO Q1 results: fun indeed

- Revenue +74% YoY

- aEBITDA +39%

- CAFD +34%

- Organic growth 9% (a little lower in reality, as this includes Wave and Aureus)

- Service/PE/CG all doing well

- Tarriff impact mostly felt on tank trailers

- First time mentioning their data center exposure: feeling strong demand in several of their portfolio companies

- Remember, all these figures are excluding the USD90mn KBK acquisition..

Discl: long

$TVK.TO Q1 25/26 report is out: https://t.co/5JKtKVVrea

- Solid organic growth driven by PE and Service

- Strong cash generation through improved W/C efficiency

- Hiked outlook on strong data center demand, where TVK is benefitting through HT, Simplex and recently acquired KBK