2025 Portfolio Review (Last one to be published)

Performance: 44.47%

5 Years TWR CAGR: 15.41%

5 Years MWR CAGR: 17.75%

Holdings:

🇳🇿 $TAH.NZ 31%

🇯🇵 $6086.T 22%

🇯🇵 $353A 21%

🇬🇧 $MHA.L 12%

🇺🇸 $FULO 10%

🇺🇸 Cash 4%

Comments, mistakes and metrics can be found in the link in bio

$TAH.NZ continues its impressive performance.

Services provided to 121 ARC Facilities up 34% YoY

Revenue up 18%

EBIT up 24%

NPAT up 25%

Two latest acquisitions under a 3x EBIT multiple

Executive Remuneration tied to ROIC with a reinvestment commitment in $TAH.NZ shares

$EASOR , The recent spin-off from $TNOM just reported an EBITDA -to-EBIT conversion of 14%. I don't think I have ever seen anything like it, not even for a software company.

Between leases and capitalization, using EBITDA under IFRS 16 is becoming a highly risky game.

@Tangible_Bruce@Kreuzmann13 Your way is the smartest/fastest way from a small capital base.

I spend my days trying to find either a great business at cigar-butt prices or a cigar-butt with a great business growing inside.

Best thing about a small base is the avoidance of overextending on valuation.

@Kreuzmann13 The # of companies I have passed on being cheap enough, just because I didn't feel I would join them in a partnership.

Looking back on it, a good % have performed well enough just based on the previously depressed valuation.

No regrets, can't hold without solid conviction.

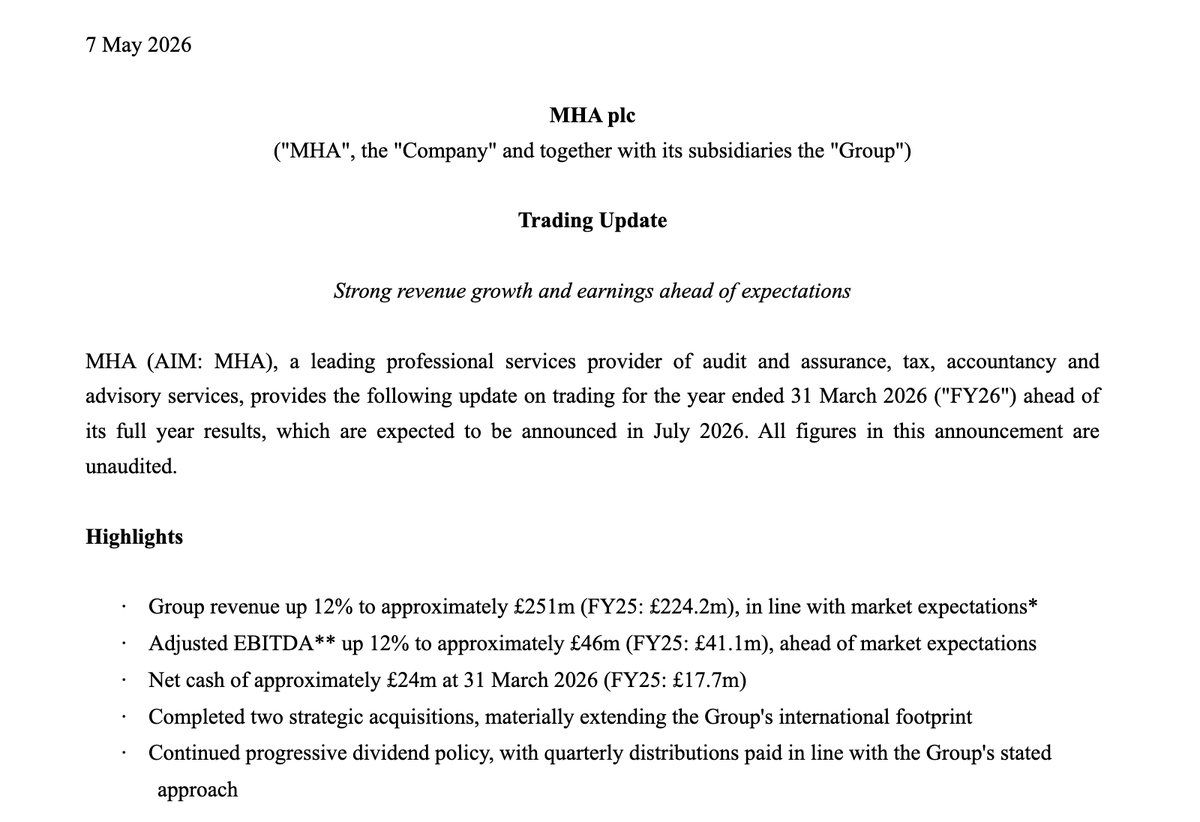

$MHA.L releases another positive trading update. Shares are up ~30% from the below a couple of months ago. Only Revenue and EBITDA released.

Trades at 10x EV/EBITDA after removing lease expenses.

Based on fully diluted shares, $MHA.L now trades at roughly 9x EV/PBT & 11x EV/FCF of the year ending March 26.

Given HSD organic growth and the drag from acquisitions, the numbers drop to 8x PBT and 10x FCF on FY27, for an 87% recurring business with very low capital needs.

@always_invest No opinion on other ops, however the P&C insurance market is plummeting, seeing rates cut by 25-35% every day on any decent account, softest market I have seen in a decade.

@OldWell17 OPI and EBT are flat for the 4Q, there was a tax credit last year.

Non-Consolidated Operating margin is over 50% and coming from a 241% increase year over year.

These things move quite a bit depending on how and where they allocate expenses, I don't read too much into it.

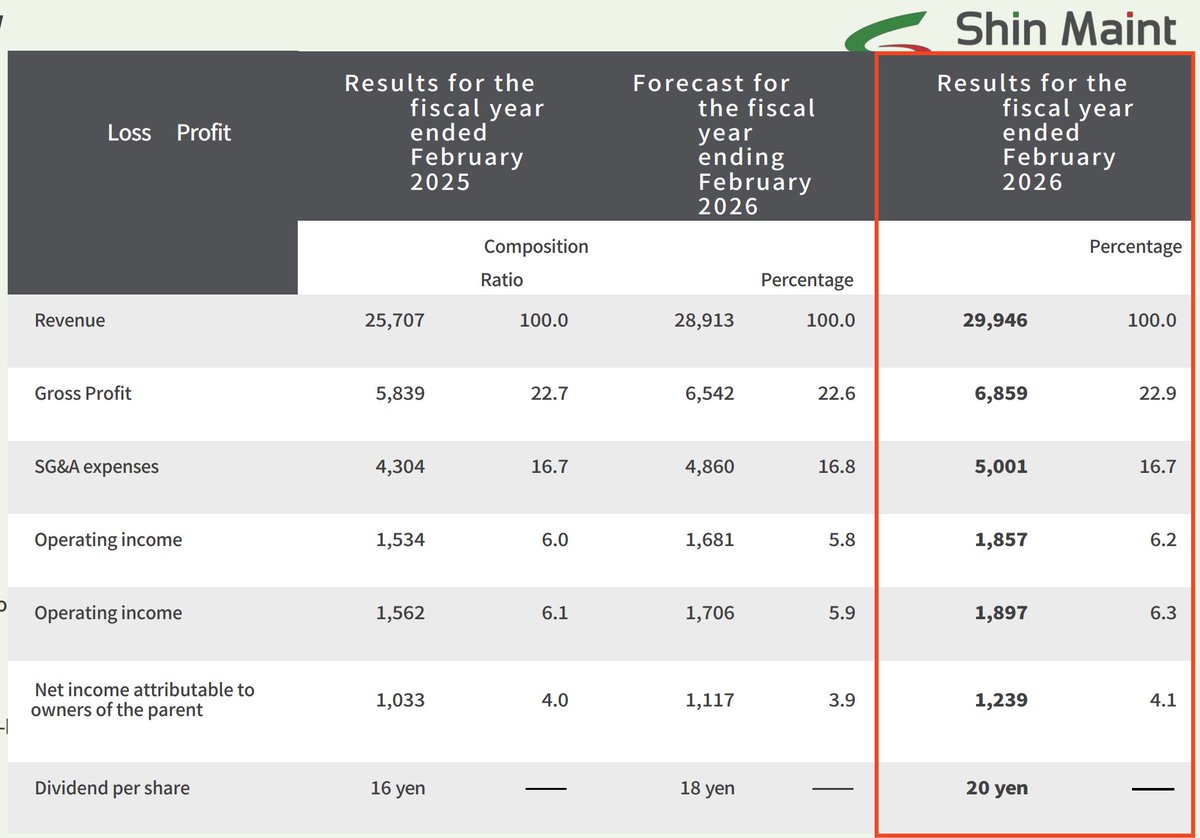

Outstanding FY26 Results for Shin Maint $6086.T

Once again forecasts are surpassed across the board, double digits are achieved in every metric.

Trades at:

8x LTM EV/EBIT

9x LTM EV/FCF

16x LTM MC/NI

Holds over 5% of market share, and owns 9% of its closest competitor.

“laid back” is what high agency ppl look like from the outside when they’ve correctly identified which games are worth playing & simply declined the rest.

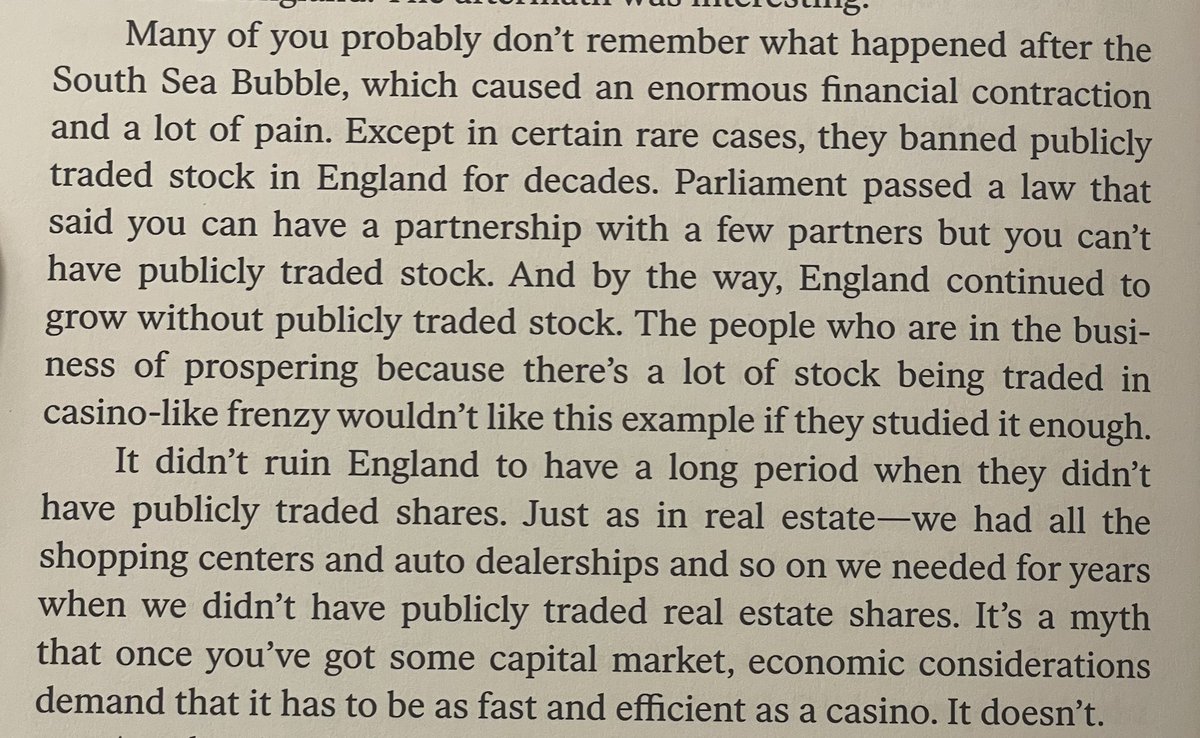

Many of you probably don't remember what happened after the South Sea Bubble.

They banned publicly traded stock.

But England continued to grow.

It's a myth that once you got some capital market, that it has to be as fast and efficient as a casino.

It doesn't.

-Charlie Munger

Just learned about the beautiful personal library of a German mining engineer called Bruno Schröder.

His entire house was covered in custom shelves he built himself, housing his life’s work – a 70,000 book collection.

Bruno died in 2022 at 88, while in the midst of digitally cataloguing his massive collection. Sadly, he had no relatives and the house, including the books, was handed to an estate manager and put up for sale. That’s when his story and these photos surfaced.

Based on fully diluted shares, $MHA.L now trades at roughly 9x EV/PBT & 11x EV/FCF of the year ending March 26.

Given HSD organic growth and the drag from acquisitions, the numbers drop to 8x PBT and 10x FCF on FY27, for an 87% recurring business with very low capital needs.

@JibbyCap That would be interesting, I guess it depends on how they structure it. I rather see $JSEART listed individually as you mentioned. Have you gotten any hint from management on it? They obviously disagree with how things work in SA but not sure if that is enough.

@TheRealJChubby@4_lugas@plainsman_32 I come from Cuba where they did this back in 1959. The part that this utopia misses is that the wealth concentration will just transfer to politicians and their families due to monopolistic power.

Those in turn create 0 jobs, 0 economic output, and a huge drag on society.