How national security priorities are rewriting global investment rules. From semiconductor wars to energy weaponization, our new paper analyzes the collision of geopolitics and finance. Essential reading for navigating structural shifts.

https://t.co/rZyNM6vFjB

From North Sea to global player: Harbour Energy's transformation through M&A creates a unique value proposition in the E&P sector. Dive into our analysis. https://t.co/8iUNs09uXA

#realassets#EnergyMarkets#Oil

🔥 Energy Opportunity: Harbour Energy (HBR) - Unlocking Hidden Value in European E&P. Projected 15-20% FCF yield, strategic global assets, and leadership by Linda Cook. Undervalued with 98% potential return.

https://t.co/8iUNs09uXA

#EnergyInvesting#realassets#oilandgas

Copper is king, and Zambia is its throne. Learn why this emerging mining hub could be the next big thing for investors in our latest report. 🛠️🌍 #Copper#Investing https://t.co/aB7eFIQLyK

As soon as @massifcap published our review of the current US elections impact on Real Assets, the Harris team releases an industrial policy platform.

The campaign manager should have called to coordinate our doc release. Lucky we mainly focused on a potential Trump Admin.

https://t.co/6QNbvWxYJh

Another Election, Another Non-Revolution: What Real Asset Investors Should (Not) Be Worried About.

In Massif's latest deep-dive report, we examine the presidential election and consider the potential impact of both a Trump and Harris administration.

https://t.co/p6cKdcoKVE

The critical #copper question for the next 2-3 years: Which is greater, the fall in demand from the Chinese real estate sector or the growth of new demand sources (electrification, grids, EVs, AI, etc), and if greater is it sufficiently greater to offset the fall in Chinese RE.

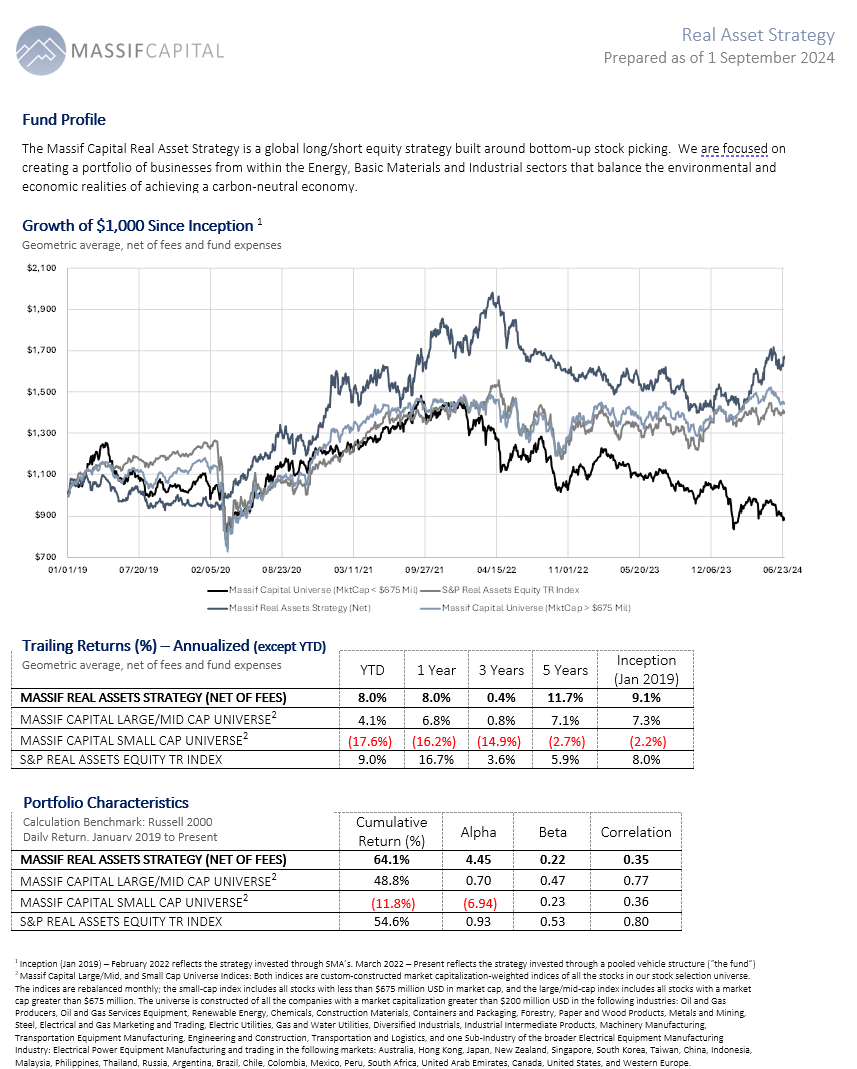

2nd Quarter 2024 Letter to Investors is out today. We discuss our good performance in the first half (up 9.4%), our investments in $ENVX and $ENR, and the importance of investment in the #realasset ecosystem for the broader economy.

https://t.co/ANUVGR93QV

New Post: The Rise of China's Solar Industry

A deep dive into how China's engineering-intensive manufacturing skills are distinct from the West's innovation skill set and crucial for product commercialization. #Manufacturing#RealAssets

https://t.co/hhQSTQ1via

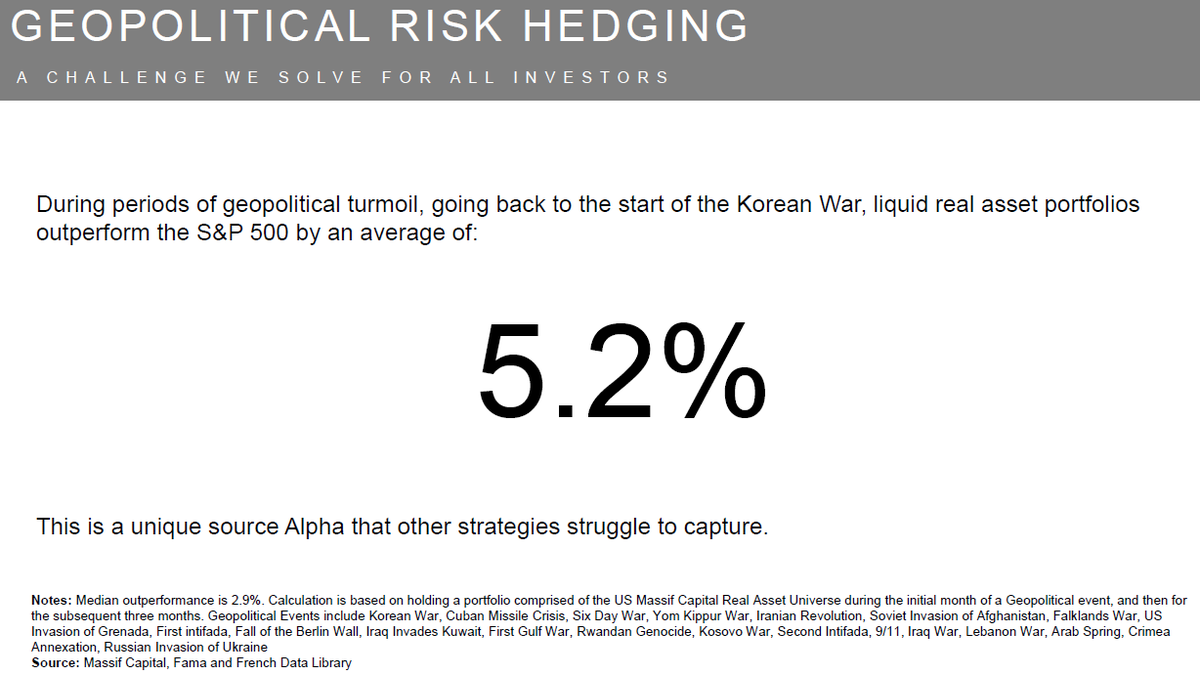

Are you concerned by growing geopolitical risk? You are not alone: https://t.co/nWn6Pko357. Massif Capital focuses on geopolitical risk, which is why our liquid #realasset portfolios outperform during periods of turmoil.

Although I agree with both points, I think they are secondary to the ongoing loss of economic vitality that comes from the slow but steady loss of manufacturing capability (which despite what politicians say is not really about job losses).

At issue is the idea that the knowledge required to manufacture things is either trivial or easily acquired. While that may be true for certain goods, it is not for many energy and industrial goods, products, and processes.

China has become the best place to get an answer to the following question: How can a new product, an invention, be translated into something that can be manufactured or used profitably? That represents a significant loss of value to Western economies, even if it represents a substantial opportunity for specific companies to boost their bottom line through outsourcing (this is management teams thinking economically, but not in terms of political economy).

China is now a manufacturing powerhouse, not because of cheap factors of production; that's only where it started, but because they have mastered a highly innovative and knowledge-intensive proprietary skill set distinct from the capabilities involved in invention and innovation but no less critical.

While most of the profit for some innovations may continue to accrue to Western companies, in some instances, regardless of where the product is manufactured, this skill set has allowed Chinese firms to make inroads with their products of equal and sometimes superior quality to Western products. (See EVs, Solar).

Combined with the large domestic market, that ability to manufacture faster, cheaper, and better acts as a flywheel that enables Chinese firms to level up, enhance productivity, and build sequentially from imitator to peer and finally to leading innovator.

In the 1960s, the Soviet Union's understanding of semiconductors was on par with the US; they fell behind because our companies moved from one-off production of a value-added innovation to mass production. The manufacturing helped create an ecosystem that produced further innovation and demand for innovation…Silicon Valley.

An innovation ecosystem does not need to be co-located, and in the West, they are not, but they do depend on the free exchange of ideas, something that China does not excel at.

Returning to the case of MAN, I have no idea if their turbines represent a security threat, but I do know that China has yet to crack the code for manufacturing high-quality gas turbines. They understand the science, but that is not the same thing as being able to manufacture, for example, a turbine that can start up in 11 minutes, has a blades spinning at 3,600 RPM, in an exhaust stream that is 600c, can but turned on and off a million times and only needs to be serviced every 32,000 operating hours. Knowing the science behind that turbine is different than knowing how to build it, and we are ceding that knowledge to China right and left.

Given the scale of the Chinese market and their incredible ability to manufacture products faster, better, and cheaper, which at this point is second to none, and should not be underestimated, we will need to see more actions like this (see article below) if the West wants to prevent China from swamping our markets with industrial kit.

Gas turbine engineering is an area of significant company-level proprietary knowledge that China has struggled with. Only last year did they produce their first domestic heavy-duty F and H class turbines, classes developed in the West in the 1990s and early 2010s.

I am a strong supporter of Free Markets, but China's market scale and the CCP willingness to use economics as a tool of the state pose an interesting problem that the West has not yet figured out how to address. Until we do so, we should error on the side of caution.

Unfortunately, the management team at MAN energy solutions is not thinking holistically. Most management teams are not, they think in terms of economics not political-economy. They suggested to the German government that the turbines were not a national security issue. The implication being that we lived in a world were politics and economics could exist in nice neat silos. That is simply not the case, economic power is political power, and represents a very real tool of statecraft for the Chinese.

Germany vetoes sale of sensitive turbine unit to Chinese group https://t.co/6JkEYLAy1n

@ypk @wmthomson22 I think the importance of this announcement is that it is further evidence in support of managements claims about potential/capabilities of the battery and equally important the manufacturing process.

@ypk @wmthomson22 We will have some updates to analysis and thesis in our 2ne quarter letter. Headsets were certainly not a variable in our analysis of the market opportunity. Not going to change that at the current time.

@ypk @wmthomson22 Headsets probably increase the market for the batteries in some marginal way but any efforts at quantifying that additional upside would be highly speculative and imply a level of precision in our analysis we are uncomfortable with.