Over the past few weeks, I have taken the time to assess Action's current situation and review the overall investment case for 3i Group ($III.L). I continue to see the long-term potential for Action, alongside additional growth drivers that offer further upside for both Action and 3i Group at the holding level.

Nevertheless, it remains crucial to critically evaluate ongoing developments over the coming quarters. At present, however, I believe that the current trends at Action are tied to broader macroeconomic conditions. Therefore, 3i Group remains an overweight position in my portfolio, with a weighting of ~34%.

In the new article on Substack, I share my thoughts on 3i Group's Q4 FY2026 figures and its future potential.

(NFA)

Over the past few weeks, I have taken the time to assess Action's current situation and review the overall investment case for 3i Group ($III.L). I continue to see the long-term potential for Action, alongside additional growth drivers that offer further upside for both Action and 3i Group at the holding level.

Nevertheless, it remains crucial to critically evaluate ongoing developments over the coming quarters. At present, however, I believe that the current trends at Action are tied to broader macroeconomic conditions. Therefore, 3i Group remains an overweight position in my portfolio, with a weighting of ~34%.

In the new article on Substack, I share my thoughts on 3i Group's Q4 FY2026 figures and its future potential.

(NFA)

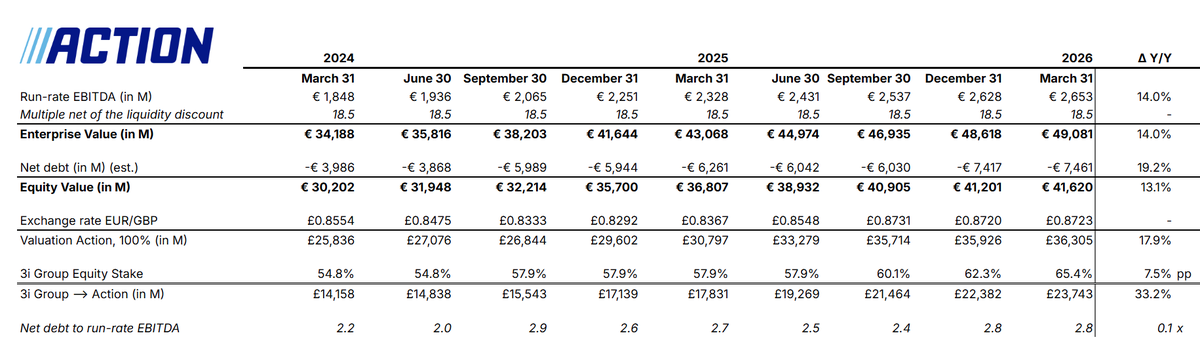

Understanding the underlying components of 3i Group’s NAV calculation is essential. I view their methodology primarily as a directional indicator of NAV/share growth, which is largely driven by Action’s expanding profitability and 3i Group’s increasing ownership stake in the retailer. While I prefer using alternative valuation metrics, I understand the rationale behind applying a fixed 18.5x run-rate EBITDA multiple to capture Action’s future potential. However, it would be rational to expect that this multiple will eventually compress as Action matures and capitalizes on its growth drivers—even if industry peers continue trading at higher valuations. Ultimately, while determining a personal viewpoint of the true fair value of 3i Group's NAV requires independent analysis, 3i Group's reported NAV serves, in my view, as an useful gauge of the asset's overarching trajectory.

3i Group's $III.L NAV per share increased by 19% Y/Y to 3,030p, up from 2,542p on March 31, 2025. This 19% Y/Y surge was primarily driven by the additional purchase of a 7.5% stake in Action and the company's expanding EBITDA.

Currently, $III.L trades at a 28% discount to NAV.

“We believe we have identified the largest actionable total addressable market (“TAM”) in human history. We estimate that our quantifiable TAM is $28.5 trillion, consisting of $370 billion in Space from space-enabled solutions; $1.6 trillion in Connectivity across $870 billion in Starlink Broadband and $740 billion in Starlink Mobile as well as additional opportunities in enterprise and government; $26.5 trillion in AI across $2.4 trillion in AI infrastructure, $760 billion in consumer subscriptions, $600 billion in digital advertising, and $22.7 trillion in enterprise applications. For illustrative purposes of sizing our addressable market opportunity, we exclude China and Russia from our global estimates.”

This will require a massive amount of CapEx in infrastructure.

“We believe that the key constraints in the continued growth of AI are physical chip manufacturing, data center infrastructure, and power generation; the future of AI will be determined by the control of the physical stack.”

— S-1 Space Exploration Technologies Corp. $SPCX (2026)

Yes, I agree with that. Even though I simply view it as operating expenses and not as some excessive costs. Just as Apple has production costs, Netflix has costs related to creating content.

Still, I think that when existing content is fully amortized, it doesn't lose its value entirely. Good movies and series will always retain a certain amount of value. Some fans return to a first season when a second one is released, while other content sits ready in Netflix library for members who might not watch it until a few years later.

With the increasing investments Netflix is making, its library continues to grow. And so does the proportion of high-quality content that Netflix carries forward into the future to create new seasons or even an entire franchise around.

Netflix $NFLX could become an Apple-like buyback machine over the next decade. I believe $NFLX is trading at an attractive valuation considering the vast runway of opportunities the company has over the coming decade. $NFLX currently has a 33%+ weighting in my portfolio.

NFA

Netflix's major costs are indeed related to its investments in content, strengthening its moat with every original it releases. These are, however, capitalized on its balance sheet and flow through its P&L in the form of amortization. Therefore, almost all of its OCF is turning into FCF, which is available to its shareholders and is increasing at a rapid pace.

@guildercapital Yeah, 3i Group's deteriorating share price doesn’t make sense to me. Need to dive deeper into the numbers, but at first glance, the long-term catalysts still hold firm.

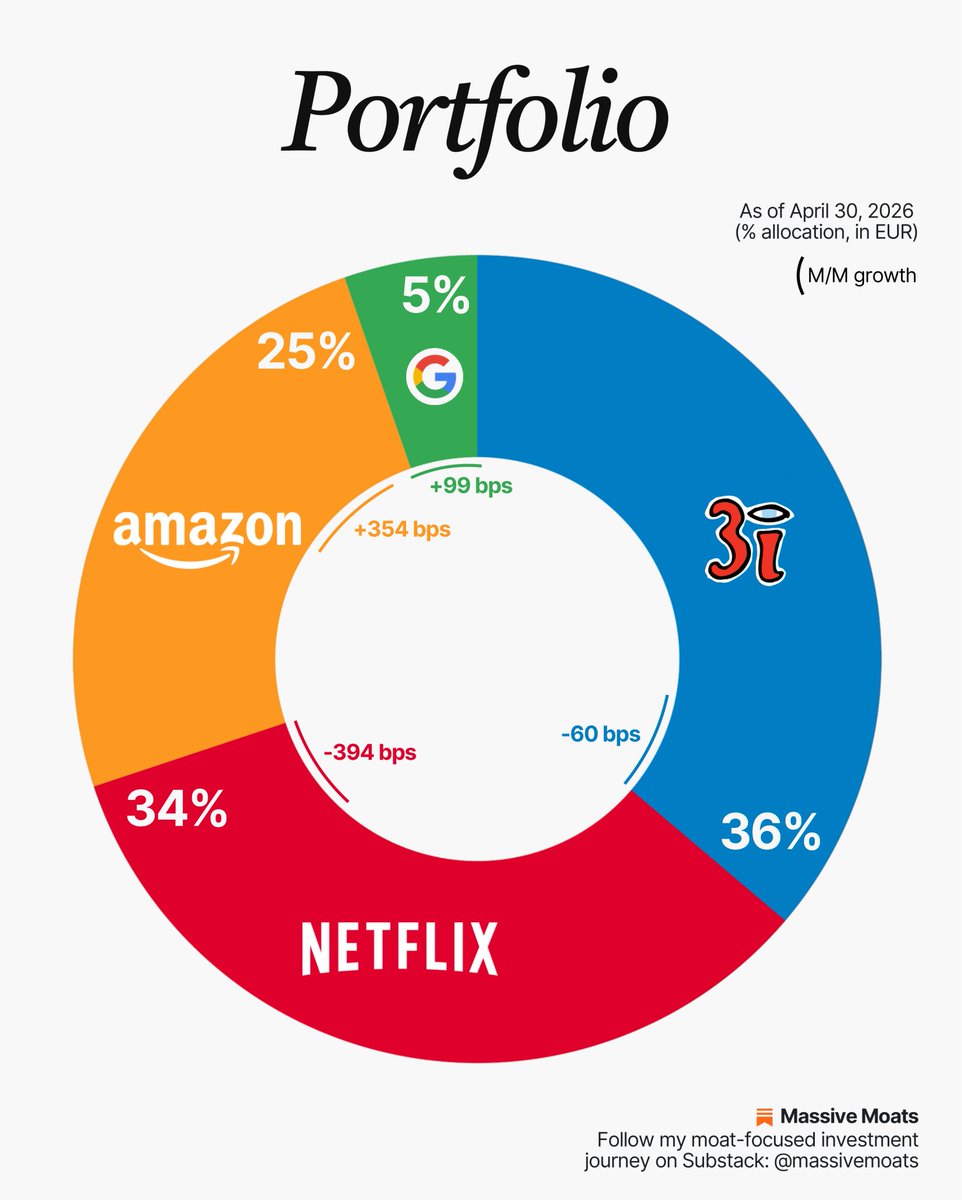

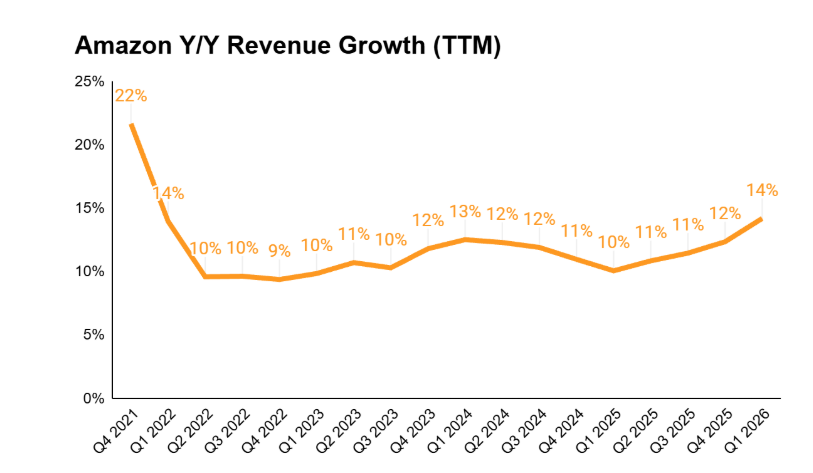

Although I made no transactions in April, the weightings within my portfolio still shifted slightly. Driven by strong price appreciation in $AMZN and $GOOGL shares, these positions have grown in weight, reducing the relative share of $NFLX and $III.L.

Holdings as of April 30, 2026:

- 3i Group $III.L: 36.20%

- Netflix $NFLX: 33.68%

- Amazon $AMZN: 24.78%

- Alphabet $GOOGL: 5.33%

- Cash 0.00%

I am currently fully invested. This marks a new chapter in my journey as an investor, bringing with it a new set of biases and risks. I share some of my thoughts on this transition in the April investor letter.

You can read the full letter via the link in the comments.

On April 29, 2026, Alphabet published its Q1 2026 results. In the article below, I share my interpretation of these figures and outline Alphabet's future potential.

https://t.co/8JtlJxGypZ

Another company creating a massive consumer surplus is Spotify $SPOT. According to the company, I have listened to 9,136 songs since 2014 and spent 138,476 minutes listening to my favorite artist.

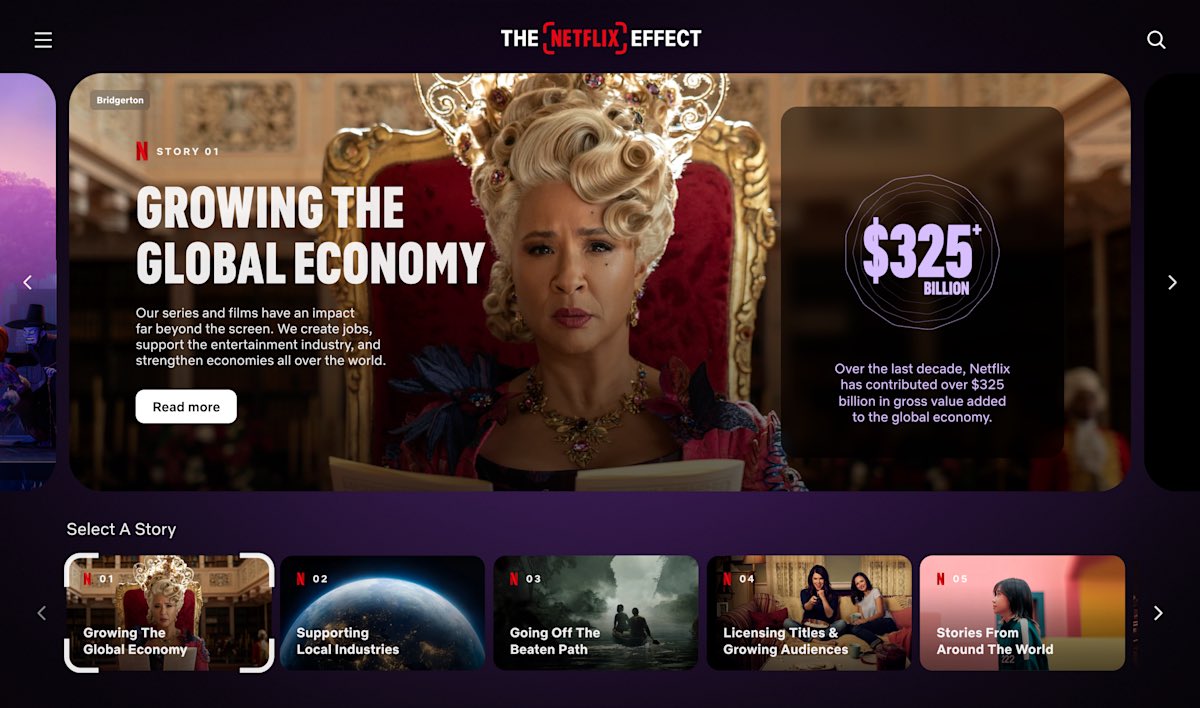

Today, Netflix $NFLX demonstrates the massive consumer surplus it delivers.

Over the last decade, $NFLX has invested more than $135B in films and series, contributed over $325B to the global economy and created more than 425,000 jobs on their productions alone.