The sequel to “A Tour of the Architecture of Crisis” is now available at Substack.

“The Flattened Depression” is the answer to what happens next, regardless of whether a peace deal is signed or not. The world is irrevocably changed and we take you on a tour of the consequences.

Going beyond the settlement question, a central theme has risen through this conflict that we are engaging in a detailed piece in the future, and that is the “flattening” of military advantages that technology has caused.

If you adopt the ELM framework to understand that the base layer of value does not consist of currency, claims, or other derivatives, then you can better understand the divergence of views that exist right now on the trajectory of the global economy.

Buried in the noise of the Rorschach Layer, a quiet revelation exists. Our framework for understanding value is very different from the textbook one widely accepted. We thought it was worthy of its own essay and we think you will too.

https://t.co/kBCf68brnL

We examine several examples of theories that come close, but do not capture the entire framework, and the counter convergent theories whose arguments attempt to dispute ELM. Ultimately, it stands up to both and is a unique and qualified framework whose evidence is abundant.

and perhaps there is a second potential outcome in the wings that may or may not materialize, but cannot be ignored based on its consequential nature, a potential kinetic action between China and Taiwan

The “Buyer’s” strike and trapped trade capital are beginning to reverse. It is counterintuitive to the mainstream narrative supported by President Trump where oil goes down and stocks go up after the MOU gets signed, but @amital13 shows the receipts plainly. It reconciles cleanly

Yesterday's OBFR volume amounted to a mere $196 billion... Is the excess liquidity in the markets rapidly disappearing?

To recap: War... high liquidity trapped in the U.S. --> OBFR surges from $180 billion per day to $280 billion... increasing leverage in the U.S... And now, a sharp decline following the agreement to end the war?

The next phase: deleveraging⚡️

#LIQUIDITY #MARGIN

With that hastily agreed to cease fire in place, the end of the blockade, and a 60-day toll-free window, followed by permanent control over the strait by the PGSA and administration by Oman and Iran, the next phase is beginning, call it "Capitulation"

In Early May, we predicted that markets were running a suppression regime that was consuming its fuel until a converging window beginning in June. That window is now here and the predictions have proven mostly true.

https://t.co/o5tGCGiFEp

What was genuinely unpredictable was the Trump administration's response to a near "Tank-bottoms" event where SPR and commercial inventories were low enough to force the nearly complete capitulation to Iranian demands in exchange for re-opening the Strait of Hormuz.

13 dead. The article states this is a restart casualty. Narrative meets reality.

The IMF forecasts Qatar’s GDP shrinks 8.6% in 2026, the worst contraction in the Gulf.

https://t.co/sWZsiBg9TT

My colleagues at Bloomberg News are reporting Qatar plans to restore ~50% of its LNG production in just four weeks after SoH re-opens, and ~80% in two months.

And that's LNG, which requires a lot of work to re-start. Imagine what everyone else is going to do with oil output.

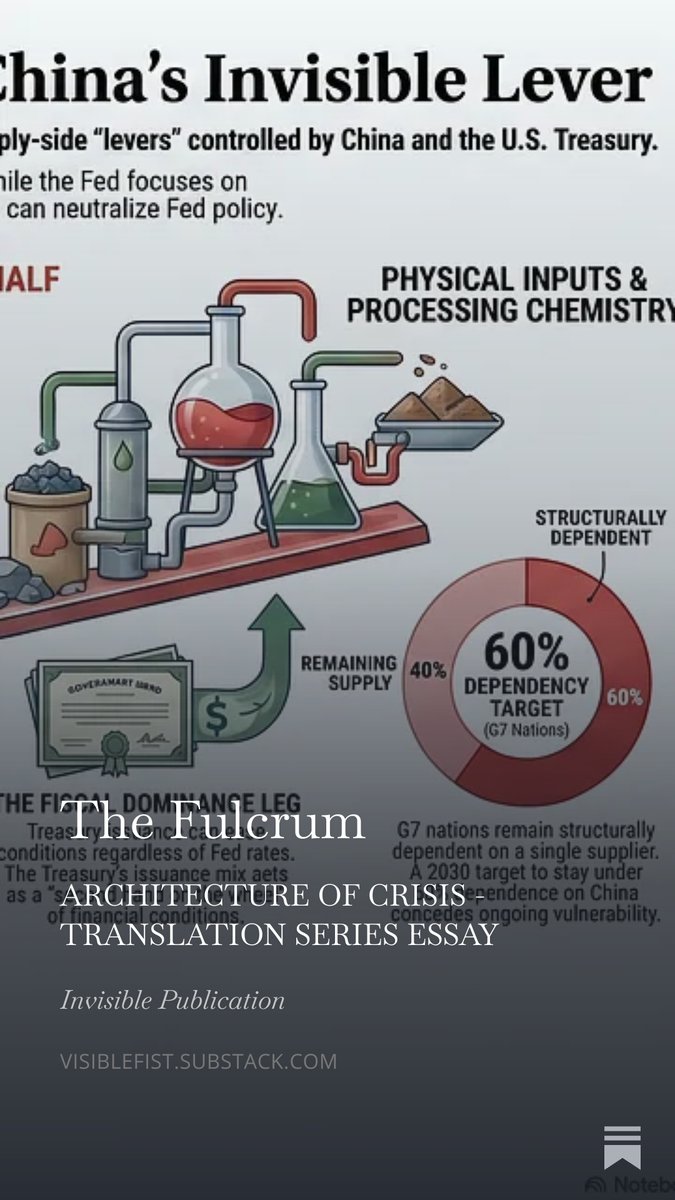

The Fulcrum demonstrates why the Fed is trapped in a cage. Between nearly infinite bid for the physical inputs for the AI buildout and advanced weapons demanded by the war, the tools central banks use do not fix shortages. Read together, they explain the catch-22.

Warsh's FOMC debut: a hawkish hold with easing underneath. He blamed the inflation on the Middle East so he could ease into it. That's the half he chose to measure. The other half, the physical inputs the AI buildout runs on, is a fulcrum Beijing can pull.

https://t.co/K0BXl9cvdm

In part 1 of The Cage we introduced the bifurcated pipe where monetary policy does not flow through from short to long duration rates. In part 2, demand destruction is already showing up despite attempts to maintain accommodative real rates.

The decision is made. 3 doors, all leading back into the same room. The cage is locked and central banks are trapped by inflation and demand destruction beyond the reach of their control.

https://t.co/KT49AgD9N1

The decision is made. 3 doors, all leading back into the same room. The cage is locked and central banks are trapped by inflation and demand destruction beyond the reach of their control.

https://t.co/KT49AgD9N1

Unreal: the symbolism of Trump signing a surrender agreement at Versailles in which the US agrees to pay massive reparations is just too perfect.

I wouldn't be surprised if Macron weaponized Trump's complete ignorance of history and told him something like: "Mr. President, Versailles is where the most consequential deal of the 20th century was signed. Yours deserves the same stage."

Either that or Macron stumbled into the perfect historical parallel through sheer obliviousness - which, knowing him, is actually even more likely.

@EmmanuelMacron There is no possible way that any treaty ever signed in that location could boomerang back on the rest of the world in an unexpected and catastrophic way, ever, right?! RIGHT????

If one only looks at the paper side of the economy, prices look benign. When measured against the physical, where rare earth and supply restricted commodities cannot be sourced at any price, the picture is vastly different.

Warsh's FOMC debut: a hawkish hold with easing underneath. He blamed the inflation on the Middle East so he could ease into it. That's the half he chose to measure. The other half, the physical inputs the AI buildout runs on, is a fulcrum Beijing can pull.

https://t.co/K0BXl9cvdm

Warsh's FOMC debut: a hawkish hold with easing underneath. He blamed the inflation on the Middle East so he could ease into it. That's the half he chose to measure. The other half, the physical inputs the AI buildout runs on, is a fulcrum Beijing can pull.

https://t.co/K0BXl9cvdm