This is a good example of why we should STAY INVESTED in a great business over many years instead of trying to jump in and out of it, hoping to sell high and buy back lower

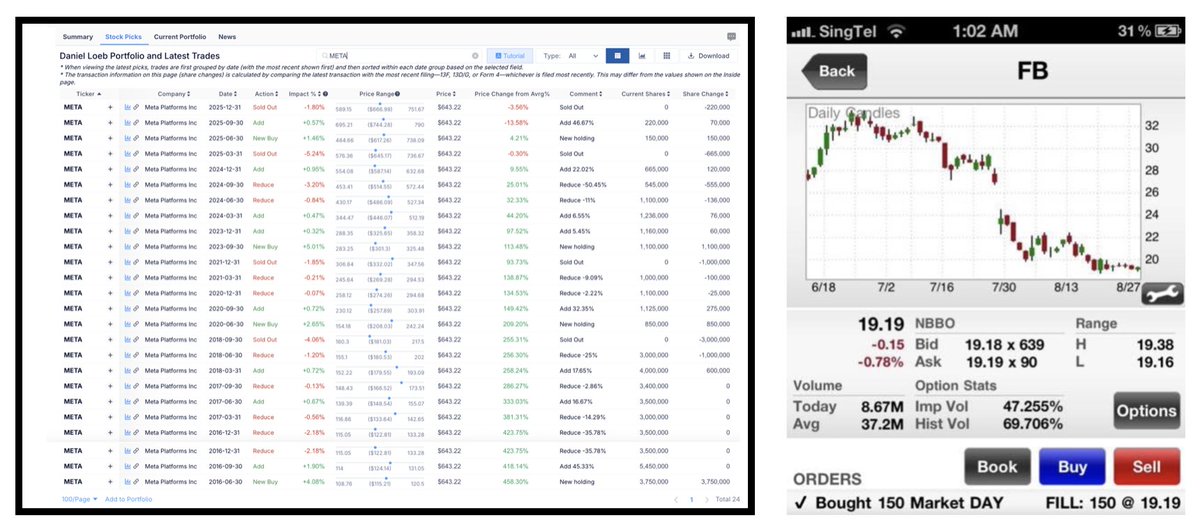

Famed fund manager Dan Loeb (Third Point) bought and sold META 4 times over the last 10 years. He has made a net profit of $595M (+39.6% total Return)

If he simply just held the shares since his first buy in 2016, his profit today will be $2.004 Billion (+491% return), 3.36X more.

This was the same stupid mistake I made early on in my investing career. In fact, I first bought Facebook (FB) at $18 in 2012. See my screenshot! If I held the shares till today, my return would be 3,200% return (33X). Instead, the idiot that I was sold it at $50 for a 177% profit. Today, I would be probably be a billionaire if I had just held all the great stocks I first bought 15-20 years ago.

Lesson: if we are fortunate enough to own a truly great business, the hardest thing to do is

“Doing nothing” . As Charlie Munger said: “The first rule of compounding is to never interrupt it unnecessarily!”

The De-dollarization myth busted!

The de-dollarization theory suggests that foreign nations and investors are diversifying away from the dollar to avoid geopolitical risk and U.S. sanctions. However, this chart shows that Foreign-Held U.S. Equities as a percentage of their total U.S. financial assets have surged to 32.4% as of late 2025. This is significantly higher than the long-term mean of 19.3%.

Foreigners aren't just holding dollars; they are aggressively betting on the growth of U.S. companies. If the world were truly "de-dollarizing" in a meaningful structural sense, we would expect to see a retreat from U.S. capital markets, not a record-breaking influx.

While there may be political posturing about using other currencies for trade, the world's savings are still being poured into the U.S. economy at record rates. The dollar’s role as the global "store of value" through equities appears stronger than it has been in decades.

@SixSigmaCapital If Medicare Advantage stays flat at 0.09% for 2027 $UNH will increase their premiums and/or reduce coverage. Senior citizens are the largest political voting block will come out in droves and vote against this administrations decision.

@qualtrim Backed the truck up and bought more! If Medicare Advantage stays flat at 0.09% for 2027 $UNH will increase premiums and/or reduce coverage. Senior citizens who are the largest political voting block will come out in droves and vote against this administrations decision. 😎

The 🇺🇸 Trump administration is proposing roughly flat rates for Medicare insurers next year, an update that falls well short of Wall Street expectations - WSJ

$UNH stock is currently down by 8% in after-hours on this news

@derekquick1 Oh, I know! You are one of the main reasons $UNH is the third biggest position in my portfolio! Thanks for the in depth videos on YouTube regarding $UNH! Much thanks brother!

AI does not pose a major challenge to the the debt rating businesses of $SPGI and $MCO, in my opinion. $SPGI and $MCO have a large moat because many financial institutions will only buy debt rated by them (or sometimes by Fitch, the third of the major credit rating agency). If debt is not rated by one of these credit rating agencies, fewer financial institutions will purchase the debt, and subsequently interest rates will be higher on the debt, costing the issuer more money. In many situations, the added expense that the issuer would have to pay via higher interest payments is significantly more than the cost of having $SPGI or $MCO rate their debt. Hence, paying $SPGI or $MCO to rate debt can actually save many companies money, hence why businesses are willing to pay them.

One argument I have heard is that AI will be able to rate debt just as well or better than $SPGI and $MCO, so there will be no need for them. Regardless of the ability of AI to judge the riskiness of debt, this line of argument completely misunderstands the moat source of $SPGI and $MCO. Many financial institutions will only buy debt if it is rated by one of the two three biggest credit rating agencies. There are various legal, historical, and reputational, and financial reasons for this. There are, for example, various laws that require that some financial institutions only buy debt rated by one of the Nationally Recognized Statistical Rating Organization, and some financial institutions also may have bylaws requiring that only debt meeting a certain rating by one of the big credit rating agencies can be bought. These requirements are set up to reduce risk, and they are very unlikely, in my opinion, to change anytime soon.

The debt rating agencies essentially serve as a third party that can give a neutral assessment of debt. The internal use of AI by organizations cannot do this. If a pension fund says that they only buy debt rated A or higher by $SPGI or $MCO, that gives more credibility and enhances comprehension than if the pension fund just said they use AI to screen debt. A financial institution could easily manipulate AI to give it whatever assessment it wanted, and hence, internal use of AI cannot be a replacement for the credibility that comes with a rating from one of the big credit rating agencies. Regulators, for example, are incredibly unlikely to be willing to accept a financial institution’s own assessment of the debt it owns when calculating capital requirements in place of relying on the ratings by the credit rating agencies.

This does not mean that AI won’t be used. Financial institutions very well might use AI as an added tool in addition to the debt ratings issued by the credit rating agencies, but it would be a supplement, not a replacement, in most situations. Likewise, $SPGI and $MCO might also use AI, but that would not threaten their moats. Rather, it might make analysts more productive, reducing labor costs and subsequently enhancing profitability for $SPGI and $MCO.

To conclude, in my opinion, the argument that AI is a major competitive challenge to the biggest credit rating agencies relies on a faulty assessment of the role that the credit rating agencies play in the financial system and why the role they play is incredibly difficult to replace. AI might be more of a challenge to some of the other parts of $SPGI and $MCO, but, in my opinion, AI is more likely to be a positive than a negative for the debt rating divisions of $SPGI and $MCO.

This is not financial advice. This is just my opinion.

I am long $SPGI.

30 years from now there will be rich people and poor people.

The poor people will be the ones that put their money into sports betting and prediction markets. The rich will be the ones that bought stocks of highly productive companies.

Choose wisely.

Venezuelan journalist Germania Rodriguez Poleo on Maduro:

“Do not for a moment let your hatred and disdain for Donald Trump…have you defending the dictator of my country…We Venezuelans are very, very happy that our dictator has been arrested.”

I don't think I've ever gone into the end of the year feeling better about my portfolio than I do now.

In order of holding size:

- Mastercard

- Google

- Amazon

- S&P Global

- Netflix

- Microsoft

- ASML

- Intuit

- Costco

- Salesforce

- Moody's

- Equifax

- Texas Roadhouse

- Duolingo

It's a blend of big tech, wide-moat credit rating businesses, universally adopted subscription services, and a few smaller fast-growing bets.

About $530k in gains so far on this $1.4 million portfolio, and we're just getting started.