October 9 - November 9

- P&L: +$93,183.91

- Max Drawdown: 5.88%

I rarely catch huge moves (3%+). Most of my edge comes from stacking frequent 0.5-2% gains with a 95%+ win rate.

The bulk of the gains came on Oct 9-10, catching one of the largest moves in a while. I barely traded for the next 10 days (travel + fewer clear setups), then wrapped up the month with the final third of gains, at a 100% win rate.

There is a conclusion many of us avoided before asset management firms (e.g., BlackRock), sovereign wealth funds (e.g., Abu Dhabi, Luxembourg), and nation-states (e.g., El Salvador, *kind of* the U.S., etc.) started accumulating $BTC. We all suspected institutional involvement would transform $BTC into something resembling digital gold. The conclusion we avoided now seems confirmed across the past couple of bull markets: $BTC doesn't perform the same function as gold.

$BTC remains compelling as a long-duration asymmetric bet. The 4-year halving cycle keeps printing higher highs and higher lows, which offers a structured accumulation framework that rewards patience through brutal 50-70% drawdowns. For long-term holders, this thesis still works.

However, regarding the "digital gold" narrative... This is where we need intellectual honesty. Gold performs its safe-haven function precisely when we need it: rising during geopolitical shocks, monetary crises, and equity selloffs.

$BTC definitely fails this test. During recent market turmoil, Bitcoin has shown 0.6-0.8 correlation with $QQQ and risk assets broadly. When $SPX drops 3%, $BTC typically drops 5-8%. When $VIX spikes, $BTC bleeds with tech stocks, not alongside gold.

$BTC may be digital scarcity, but it's not digital gold; at least not yet. It mostly trades as a levered tech bet, not a safe haven. The 4-year cycle thesis can coexist with this reality, but pretending $BTC protects portfolios during risk-off events contradicts observable market behavior.

We should invest based on what assets do (on a large enough sample of events), not what we wish they were. For now, invest in the 4-year cycle; just don't count on $BTC to protect you in crises because, so far, it never has.

At Bitcoin MENA, @cz_binance’s chat about the gold bar stunt with me omitted the fact that tokenized gold is just as easy to verify as Bitcoin. The critical difference is that with tokenized gold you verify ownership of something, but with Bitcoin you verify ownership of nothing.

And then you have CT constantly posting "everybody predicted the top, so we're about to hit new ATHs" and/or "everyone is saying it's a bubble, so it's not a bubble."

Bullish investor sentiment is surging:

44.3% of individual investors expressed a bullish stock market outlook over the next 6 months in the latest AAII survey, the highest since October 8th.

The peak over the last 12 months was 45.9%.

Over the last 3 weeks, this percentage has risen by +12.7 points.

During the same period, the share of retail investors expressing bearish sentiment has declined -18.3 points, to 30.8%, the lowest since January 23rd.

As a result, the gap between bullish and bearish readings jumped to 13.5 points, the 2nd-highest this year.

Everyone wants a piece of this market.

Congrats on the gains!! I closed that new long after 1h btw when it was in good profits, as I was waiting for another proper fill of the CME gap, which means I missed on some additional gains today since it kept going up!

But it looks like my order for yet another long above the gap just filled now. I have more long orders at $88.9-89.3K; hopefully they get filled too. I'll do my best not to close those before Wednesday.

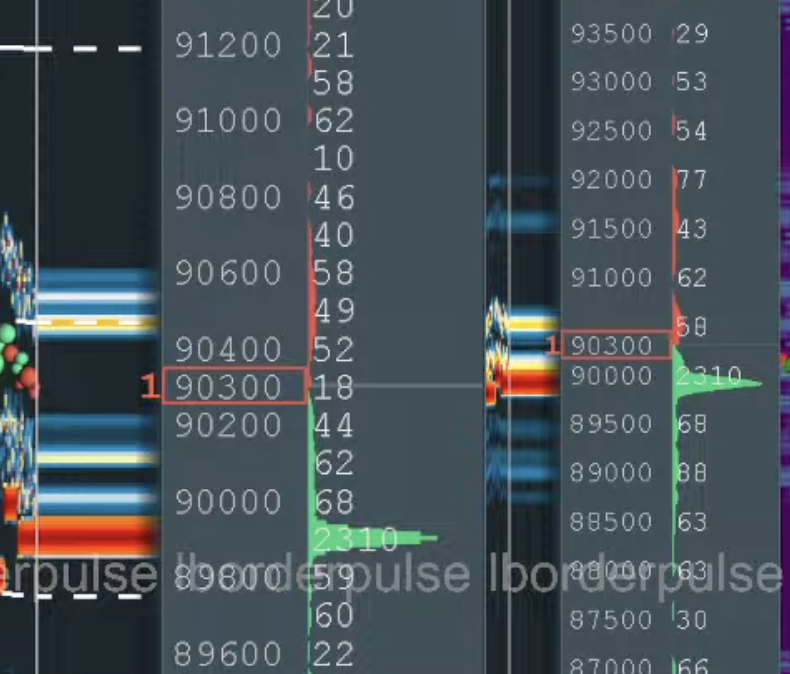

The same entity has been appearing in the order books with more than 2,000 $BTC for the past couple of months. Before October 10, they typically deployed less than half of that amount to spoof the OB. Now, whenever they switch from showing 2,000+ $BTC on the buy side to 2,000+ $BTC on the sell side (and vice versa), other algorithms react almost instantly.

I just noticed the wick to $88.3K that happened on Coinbase in the past hour. $BTC might fill that wick in most exchanges before going up for a few days.

Also, the S&P just filled the last gap to the upside (6,890) today, there is nothing else above and no catalysts for risk assets after FOMC. Don't count on liquidity having any significant impact on these markets for a few months.

I just noticed the wick to $88.3K that happened on Coinbase in the past hour. $BTC might fill that wick in most exchanges before going up for a few days.

Also, the S&P just filled the last gap to the upside (6,890) today, there is nothing else above and no catalysts for risk assets after FOMC. Don't count on liquidity having any significant impact on these markets for a few months.

Do we finally understand that the $MSTR preferred dividends reduce Bitcoin per share when funded with common stock sales and/or BTC sales or are we still living in a fantasy land?

@ShardiB2 Couldn't muster enough strength to close the gaps above, even when it was really close. That should be taken into account for the (very) short-term.

@amitisinvesting 1. What Trump wants leads to the same situation that Japan is dealing with right now. Costly mistake.

2. Regarding QE: https://t.co/ZgvyNWKTuJ

Quantitative easing and routine asset purchases aren’t the same, and this article emphasizes that by mentioning:

- "in no way represent a change in the underlying stance of monetary policy"

- "not a new effort to stimulate the economy"

- "long-planned phase of the Fed’s approach to matching the levels of cash-like assets"

- "modest level of Fed bond purchases"

QE is large-scale stimulus; it only shows up when interest rates are already near zero. Right now, to stimulate the economy, the Fed can still lower the interest rates for a while (most likely years), before QE is even on the table. Last time we had QE, it was in response to COVID, and rates were at 0, as is often the case for such reactions from the Fed.

Since this isn’t QE and doesn’t signal a shift toward crisis-level easing, I still support the idea that 2026 won’t get some surprise liquidity surge and that $BTC follows the usual 4-year cycle and bottoms by end of 2026 (unless macro conditions truly break, in which case, I'll likely return to posting macro takes).

I was chatting with Claude about the situation with Japan’s yields, and I asked it to put together a full recap, with an intro explaining how bonds and yields relate.

I hadn't read about this stuff in years, and the intro turned out to be a great primer for anyone who wants to interpret the situation we are in for the next few months.

Here it is:

"A bond is a loan packaged as a tradable security. When a government or corporation issues a bond, it is borrowing money from investors. The bond specifies a face value, which is the amount that will be repaid at maturity, a coupon rate, which is the annual interest payment expressed as a percentage of face value, and a maturity date, which is when the principal must be repaid.

For example, a ten-year U.S. Treasury bond with a face value of one thousand dollars and a five percent coupon pays fifty dollars in interest each year for ten years, then returns the one thousand dollar principal at the end. Investors who need safe, predictable income often buy bonds, while those seeking higher returns and willing to accept more risk prefer stocks.

Bond prices and yields move in opposite directions, which is one of the most important relationships in finance. The yield is the annual return an investor earns on a bond based on its current market price. If you buy a bond at face value with a five percent coupon, your yield is five percent. But if the bond's price falls to nine hundred dollars, your yield rises above five percent because you are earning the same fifty dollar annual coupon on a smaller initial investment. Conversely, if the bond's price rises to one thousand one hundred dollars, your yield falls below five percent.

This inverse relationship explains why bond prices fall when interest rates rise. If the Fed raises rates and newly issued bonds offer higher coupons, existing bonds with lower coupons become less attractive, so their prices must fall to offer competitive yields. Similarly, when the Fed cuts rates, existing bonds with higher coupons become more valuable, so their prices rise."

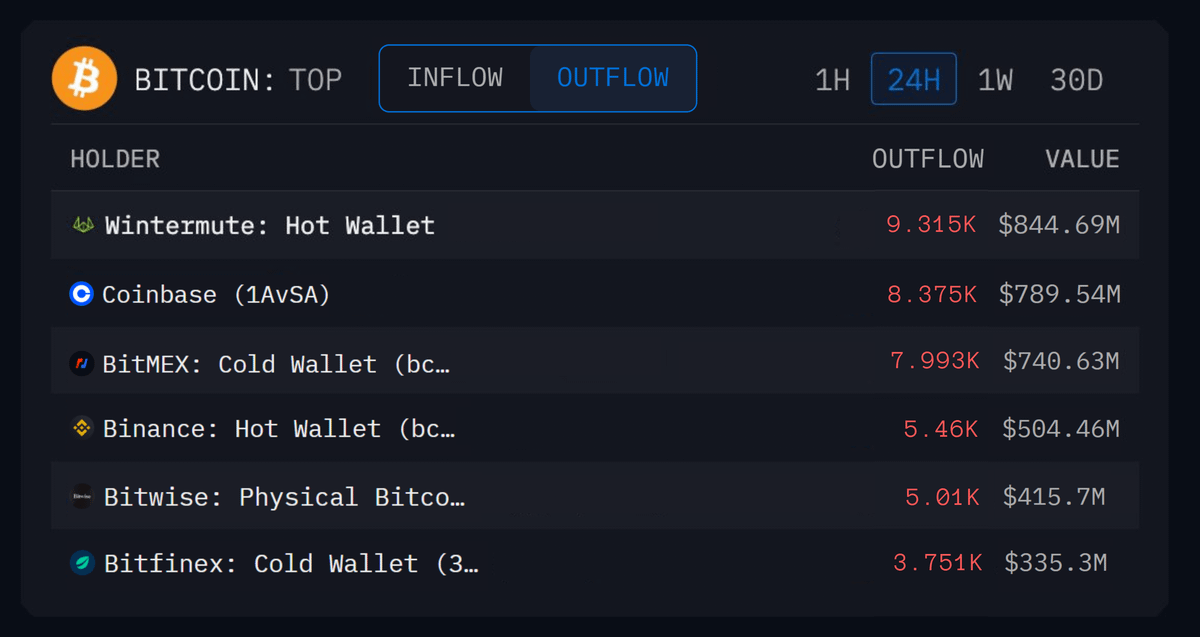

1. This post is double-counting a lot of the outflow. The $BTC flowing out of @wintermute_t 's hot wallet is mostly composed of $BTC that flew out from @coinbase and @binance, for example, to @wintermute_t.

2. I can think of 4-5 routine reasons for exchange-related $BTC outflows that don’t imply coordinated or conspiratorial selling.

3. New week / new month systematic rebalancing (one of those routine reasons) is linked to algo-driven de-risking, especially in the current macro environment with rising Japanese yields and tightening liquidity across markets.