$Wrap @WrapTechInc@Defconservices_

“The Interview Most Investors Probably Missed.”

On May 5, 2026, WRAP Technologies CEO Scot Cohen appeared on the OnlyCops podcast for a fifty-seven minute conversation that most investors likely never saw. It was not an earnings call, not an investor conference, and not a carefully staged Wall Street presentation. It was a long-form discussion with a former police officer talking candidly about use of force, training, liability, officer safety, and the growing gap between what departments expect officers to do and the tools they actually give them to do it.

Which is precisely why the interview mattered.

Because beneath the promotional tone and sympathetic setting, the conversation revealed something much larger than a product pitch. Scot Cohen was not really talking about BolaWrap as a standalone restraint device. He was describing what increasingly looks like an attempt to reposition WRAP itself around a broader concept: Non-Lethal Response as an operational architecture.

The most important sentence in the interview may have been the easiest to miss:

“the new launch of the company through this non-lethal response in the next thirty or so days.”

Not the launch of a product.

The launch of the company.

That distinction matters because it explains much of what WRAP has been quietly building over the last year. Training infrastructure. LMS integration. VR deployment. Drone-enabled response concepts. Policy-compatible workflows. Partnerships built around operational integration rather than simply hardware distribution. The company increasingly appears to understand that the challenge was never just proving that BolaWrap mechanically works. The challenge was building a framework around it that departments could actually operationalize at scale.

Today is May 26, roughly three weeks after the interview aired, and enough has happened since then to confirm that the repositioning Cohen described is real.

Since the interview, WRAP has accelerated the public rollout of its “Non-Lethal Response” framing across releases and partnerships. The company has expanded its drone-first-response messaging, continued integrating training into the center of the narrative, and publicly described its vision as extending “far beyond a single device.” It has increasingly characterized itself not as a standalone hardware vendor, but as an integrated Non-Lethal Response ecosystem.

That shift was already visible in pieces before the interview. The STORM Training Group relationship. WrapReality VR deployments. Healthcare expansion. LMS infrastructure. The growing emphasis on doctrine and workflows rather than simply selling devices. But the OnlyCops interview was the clearest articulation yet that WRAP no longer wants investors to think of it primarily as “the BolaWrap company.”

It wants to define a category.

And the category it is attempting to define sits inside a very real tension now emerging across law enforcement and public safety. Departments continue tightening policy around force while simultaneously demanding fewer injuries, fewer lawsuits, fewer controversial encounters, and more measurable policy compliance. Yet officers still need workable options before situations escalate into lethal force or violent hands-on encounters.

That operational gap drove much of the interview.

The former officer hosting the discussion repeatedly described what many departments already understand privately: pain-compliance tools increasingly carry litigation exposure, medical scrutiny, administrative burden, and policy complications. Meanwhile, hands-on force remains dangerous for both officers and subjects, particularly in an era of staffing shortages, declining recruitment, and inconsistent training standards.

WRAP’s thesis is that restraint-based intervention may increasingly fit the space in between.

Not lethal force.

Not traditional pain compliance.

Something else.

What Cohen repeatedly described was a layered response architecture built around light, sound, restraint, training, and policy integration. Even the drone discussion reflected that same framework. Cohen confirmed a UK-based drone-first-response order and identified Vector as a training-focused operational partner whose drone curriculum is being integrated directly into WRAP’s LMS infrastructure. Importantly, border-security applications were referenced explicitly during the discussion, signaling that WRAP increasingly views drone-enabled non-lethal response as a federal and perimeter-security opportunity, not merely a municipal patrol tool.

That matters because it expands the company’s strategic ambition well beyond the traditional belt-device market. The story being told now is not simply about patrol officers carrying BolaWrap. It is about distributed non-lethal response infrastructure spanning patrol, corrections, healthcare, private security, perimeter environments, drone deployment, and eventually federal operational settings.

Whether WRAP can successfully execute that transition remains an entirely separate question.

The company still faces major obstacles: entrenched procurement ecosystems, incumbent vendor relationships, slow policy adoption cycles, training friction, capital constraints, and the sheer institutional difficulty of changing public-safety doctrine. Some of the interview’s most interesting claims also remain unverified publicly, including Cohen’s assertion that roughly one hundred departments are now deploying BolaWrap more frequently than TASERs, pepper spray, or batons in certain operational contexts.

And importantly, the “thirty-day” clock Cohen publicly created is still running. While many elements of the repositioning have clearly surfaced since May 5, the full “launch of the company” he described still appears incomplete as of today. There has not yet been a definitive unveiling of a fully integrated Non-Lethal Response operating framework, investor presentation, or formal relaunch event tying all of these components together.

But the strategic direction itself is now difficult to miss.

WRAP no longer appears to be trying to reposition a product.

It appears to be trying to reposition the entire conversation around force.

Disclosure: I am long WRAP common. This is not investment advice.

https://t.co/fZ6bQZPgmE

DID $DGXX JUST SOFT ANNOUNCE MAJOR DEAL? Multi-billion dollar mystery.

Before you label me as a delusional bull poster, hear me out.

This is my own theory/speculation based on available information, but I think there is a high chance that DigiPower X has entered into a major agreement/partnership with 100B+ MC company.

Lets lay down some facts:

➡️CEO Michel Amar likes to underpromise and over deliver. He has taken a very careful approach to expansion of the company and every move has been well calculated.

➡️ $DGXX has 85 million cash and crypto in their balance sheet, up from 29 million on September 30.

➡️A recent press release indicates that the estimated 2026 T3 HPC MW will be 300% higher than estimated in October 2025.

➡️2027 T3 HPC MW will be staggering 700% higher than estimated in October 2025.

➡️The North Carolina site will become online 2028.

➡️They were in advanced talks with +100B MC company.

Lets then ask some questions:

Why would Michel Amar suddenly promise us a 700% higher MW number for T3 in 2027 and 300% higher for 2026?

Why announce North Carolina availability now?

Why not lay this information out in the earnings release next week? Why now?

Where did the 56 million extra cash come from?

And the billion dollar question:

Where will DigiPower X get 1.5 billion dollars to build all the promised T3 infrastructure?

The answer is simple: Either a major deal or partnership.

DigiPower X filed 6-K on October 15 with SEC for a special meeting taking place on December 11 2025. We have not yet got a proxy for this meeting, so we do not know what will be voted on at this meeting, but considering the timing of yesterday's press release, I do believe it will come between today and the 13th of November ER.

I think this proxy will contain information about a significant partnership or deal which will require shareholder vote.

CEO Michel Amar laying down his bullish roadmap just before earnings does not make any sense otherwise. He had to do it so we know what we will get if we vote yes.

Let's break down the press release:

First company states:

“This robust liquidity positions Digi Power X to accelerate the rollout of its 2026 AI infrastructure development plan, which includes the planned deployment of high-efficiency Tier III AI data centers and expansion of the Company's critical power capacity across multiple U.S. sites.”

DigiPower X provided an update to their strategic roadmap of AI rollout and there are some HUGE updates.

DigiPower anticipates the following rollout of Tier 3 AI/HPC computing power to come online next year.

Q1 2026: 5 MW

Q2 2026: 15 MW

Q3 2026: 30 MW

Q4 2026: 55 MW

If we take a look at the October 2025 investor presentation, the Total Anticipated Megawat Portfolio for next 24 months was 220MW and only 10% allocated to HPC. This means that DigiPower X is accelerating rollout by almost 300% and will do it all in next year.

The other notable update was the CURRENTLY available power in DigiPower X infrastructure.

Alabama site: 55 MW (up from 22MW October 2025)

New York sites: 141.7 MW (up from 79MW October 2025)

Total available power TODAY: 196.7 MW (up from 100MW October 2025)

This means that they have managed to almost double their MWs in the past couple months. This is huge news and this is only possible if the North Tonawanda power plant completed load study is now operating at 120MW.

DigiPower X also finally shared the estimated availability of Hildebran, NC datacenter. The 200MW datacenter is anticipated to be available by 2028. I like to see that they have now given us some estimations instead of just mentioning that it is “In development”. Things are moving in the right direction.

Lastly, we got forward looking statement to year 2027:

“Looking ahead to 2027, the Company is targeting a total operational capacity of 195 MW, including 140 MW of critical AI compute infrastructure. That planned expansion underscores Digi Power X's commitment to becoming a leading provider of high-density, AI-optimized Tier III data center capacity in North America.”

140MW of critical AI compute infrastructure is almost 700% more than the 22MW in October 2025.

Rolling 140MW critical AI infrastructure will cost over a one and half billion dollars CAPEX and is not feasible for such a small company without partnership or forward paying deal.

We know DigiPower has partnered with Ramboll Group A/S, the Danish engineering and consulting firm which brings credibility to DigiPower.

Ramboll also partnered recently with TeraWulf $WULF to transform TeraWulf's Lake Mariner campus in New York—a former coal-fired power plant site—into a near-zero-carbon AI and high-performance computing (HPC) data center.

As I said, this is just my theory and speculation, but for me it just does not make sense to announce such a major ramp in terms of MW just before earnings, unless there will be something which requires shareholders to know this before proxy vote.

Please let me know in comments if you think I am completely off with this speculation.

Disclaimer: This is not financial advise. Writer is very long AF on $DGXX and has a bullish bias.

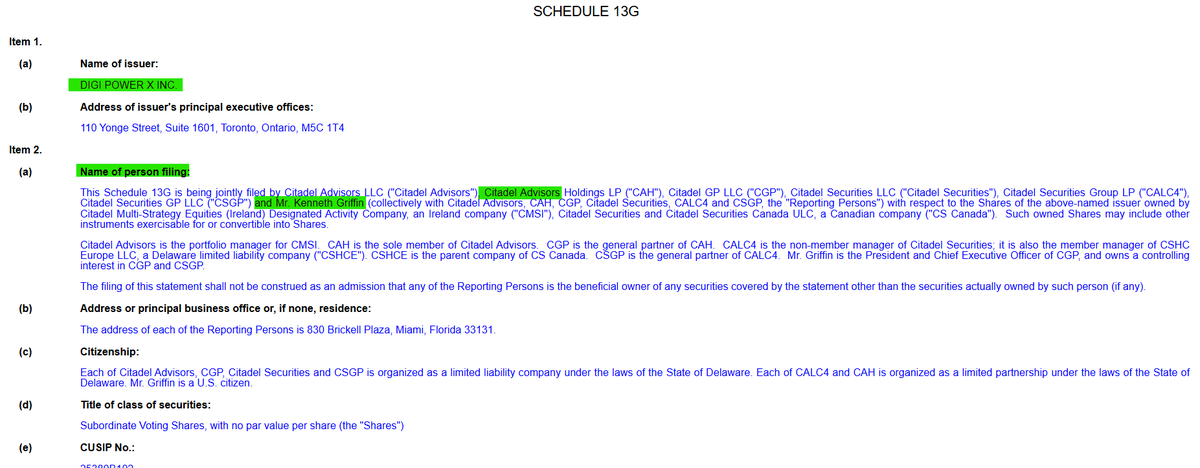

First Peter Lynch... and now Citadel (including Ken Griffin personally) just took a stake in DigiPower X $DGXX.

If you listen to my Wall Street Unplugged podcast - you should be in this AI name below $1.50.

It's now trading over $4... with two legendary investors backing it.

$WRAP From Wrap website, States ramping deployments: "Recent changes in the Law Enforcement Liability Landscape have expanded BolaWrap™ 150 use and widespread adoption"

US Gold Corp $USAU just released its updated pre-feasibility (PFS) study on its permitted CK Gold Project in Wyoming.

It shows USAU is sitting on a near $1B ASSET!

Using a gold price of just $2,100 and copper price of $4.10... the NPV is $459M, 42% HIGHER than the previous study.

Yet, if we use today's prices (gold- $3,000 / Copper - $4.50)... the NPV surges to over $950 million.

USAU's current market cap is just: $100M.

Keep in mind... this does not include any of the aggregate (which is in high demand, and easily minable given the project lies in one of the most mine-friendly jurisdictions in the US).

Based on my estimates, the aggregate alone is worth close to the full market cap of the company.

In other words, you are getting the permitted CK Gold Project, it's signature asset with a "net" NPV (so minus the cost to mine the project) of over $620M - FOR FREE.

This is just one of the few junior mining companies that will has incredible upside potential as the price of gold heads higher.

I will be sharing several others (names and mgmt teams I've followed for 10+ years) over the next few days.

https://t.co/BPpuo50xV6

Great to see Wisconsin lawmakers pushing for more nuclear energy. Clean, reliable, and efficient—nuclear is key to a strong energy future. Time for more states to follow suit! ⚡ #NuclearEnergy#Wisconsin#EnergyFuture” https://t.co/Iq7QFvXtYF

I don't care what you think of Rodgers, that is absolutely heartbreaking. Left the Packers with class, handed the keys over to Love, seemed so excited for his next chapter and then it ends in 4 plays. I'm sick