Here are my proposals for improving $STRC:

On the technical end:

- Offer optional depeg insurance to buyers in exchange for a portion of the yield. On the flip side, offer a degen version of STRC with higher depeg sensitivity but much higher yield. Degens can thus provide a portion of the liquidity during sell events.

- To a limited extent, defend the $100 price by deploying balance sheet assets and issuing stock to provide additional liquidity during sell events. Host a dedicated STRC-USD, STRC-BTC and STRC-MSTR trading desk.

- Maintain a high USD reserve at around 20-30% of net BTC held. Rebalance when the BTC price moves up or down. (This ensures you generally buy low and sell high.)

While these measures don’t guarantee that STRC always keeps its peg, they make it a much more robust product.

On the marketing end:

- Pitch STRC as a novel high-yield stablecoin-like product backed by Bitcoin.

- Be transparent about tail risks and provide clear warranty conditions and risk mitigation strategies (i.e., via additional insurance coverage).

- To Bitcoiners and MSTR holders, clarify how the company intends to deploy its balance sheet to defend the $100 peg in the short term while maintaining the long-term vision of accumulating Bitcoin and providing amplified performance to common stockholders.

- Showcase how STRC is battle-tested against various scenarios, including BTC and MSTR price crashes and a massive sell-off in STRC.

Other suggestions:

- Hire the best technical talent from the crypto industry to build next-generation DeFi products on top of STRC. Tokenize STRC and MSTR and list them on decentralized exchanges.

- Internationalize STRC and MSTR.

- Collaborate with Tether to get STRC to back USDT.

BREAKING: Bitcoin is now expected to fall below $50,000 this year.

The odds of Bitcoin falling below $50,000 in 2026 have surged to 64%.

There is also now a 46% chance of Bitcoin falling below $45,000.

Of course, the question arises as to who will buy such a funky product that appeals to neither degens nor institutional investors. This can be partly mitigated by better marketing. Beyond that, secondary insurance markets can be established that protect investors against depeg risk. Part of the high yield offered by STRC can pay for the premium. With this, both institutional investors and degens can independently participate in the product. In fact, degens can secure the leveraged yield they seek by selling depeg insurance to risk-averse investors.

Hot take: STRC depeg is a feature, not a bug.

A temporary depeg is the only way to ensure users don’t abuse the carry trade arbitrage. It acts like a release valve to flush out leveraged positions. Price and volatility will restore over time as new buyers enter to take advantage of the higher effective yield. This ensures the long-term health of the product, as the risk of depeg discourages degen behavior.

Saylor’s biggest misstep was falsely advertising STRC as basically risk-free. But I get that it’s hard to sell a product that works as intended **most** of the time. No car salesman mentions the maintenance cost of the car they’re selling.

There is absolutely zero alpha on Polymarket when it comes to price action. The probabilities you see there can basically be deduced from a random walk model.

There is a way Strategy could generate yield per share even if their mNAV goes below 1. In this case, they have to sell Bitcoin and buy back the shares with the proceeds. They can do this until mNAV returns to 1.

Selling Bitcoin when it’s advantageous is a very rational thing to do. That’s the whole point of buying Bitcoin in the first place.

What’s really BS is claiming you will never sell. From that aspect, Saylor is more rational now than in the past, which is an improvement and not a flip-flop.

For 5 years Michael Saylor told the world he would never sell Bitcoin.

Last night that changed.

On Strategy’s Q1 2026 earnings call, Saylor admitted his company will probably start selling.

This is the complete opposite of what he has been preaching since 2020.

Strategy holds 818,334 Bitcoin at an average cost of $75,537 per coin.

That’s $61.8 billion deployed into Bitcoin since August 2020.

Nearly 6 years of relentless buying.

Bitcoin is now around $81,000.

Their entire stack is up around 7% in almost 6 years.

That’s roughly 1% per year.

The S&P 500 returns about 10% per year on average.

Bitcoin itself is up 700%+ over the same period.

Strategy bought Bitcoin the entire way up and still barely broke even.

This is what happens when you buy aggressively at every price with no discipline.

You drag your average cost higher and higher until you have no margin of safety left.

And now they have a real problem:

Strategy issued a preferred stock called STRC that pays an 11.5% annual dividend.

That’s $1.5 billion in dividend obligations they have to fund every year, no matter what Bitcoin does.

So when Bitcoin dropped from $87K to $68K in Q1, Strategy posted a $12.5 billion net loss.

The largest in the company’s history.

Now Saylor has to sell the very thing he built his entire brand on never selling, just to pay dividends on a financial product his own company created.

When we start buying BTC again, we will share it here.

Turn on post notifications so you don’t miss our alerts, this is VERY important.

A lot of people will wish they followed us sooner.

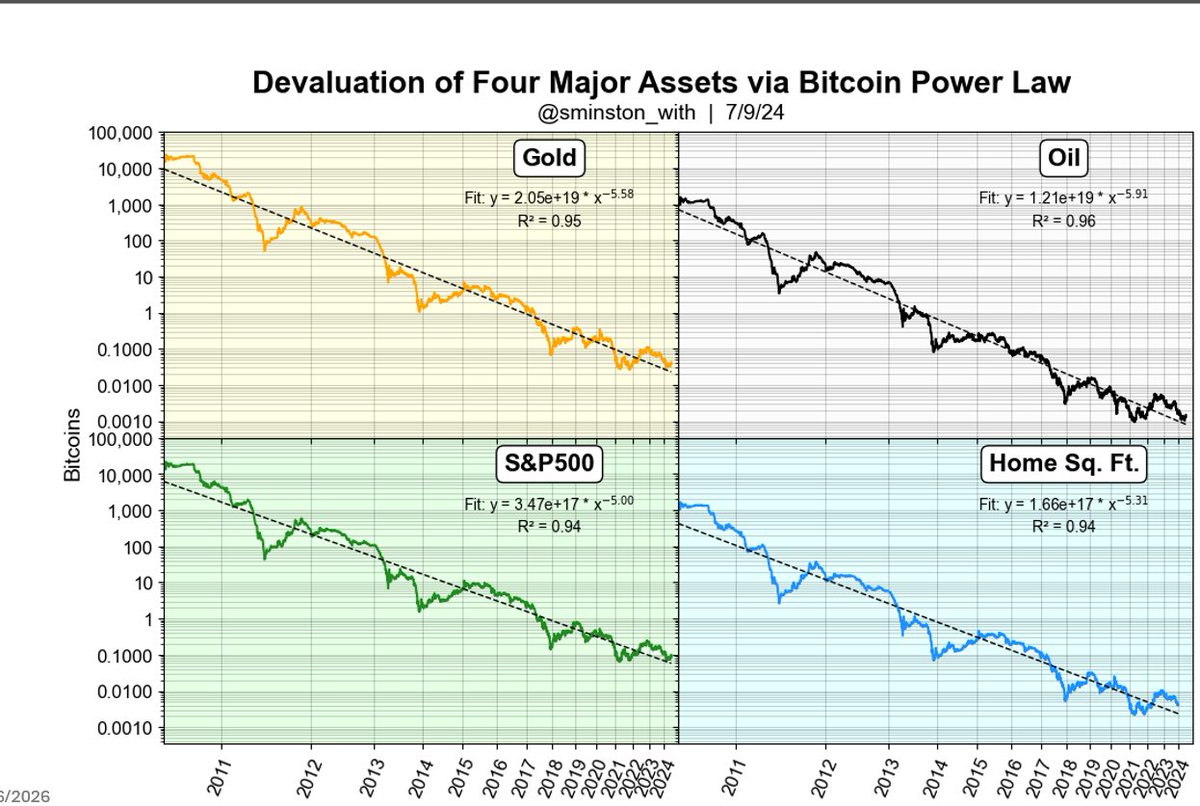

Indeed, as Giovanni puts it, the denomination does not really matter for visualizing Bitcoin’s price power law, since no other asset or commodity has scaled 8 orders of magnitude in just 17 years.

However, most people forget that Bitcoin’s primary market is in fact energy. Thus, the most natural unit for denominating Bitcoin’s price is joules. If you are a purist, you can construct your price model in joules per BTC and you will essentially recover the t⁶ power law. The main drawback of this approach is that you need to track global average miner efficiency (kW per TH/s), which is not straightforward (see CBECI). But it is possible in principle to price Bitcoin without reference to any currency. This is the unique feature of PoW-based mining that Satoshi pioneered.

That being said, USD is the most pragmatic choice for modeling price, since it is by far the largest, most open, and most liquid market for exchanging Bitcoin. USD is also crudely tied to the price of energy, making it an imperfect but sufficiently good substitute for joules.

Even when we price Bitcoin in gold, for instance, we are essentially comparing the dollar price of Bitcoin against the dollar price of gold. Whether we like it or not, USD—being the most traded, most liquid asset to ever exist—makes it the unit of account for modeling price. There is no second best at the moment.

Whenever I thought I covered all the topics in the book somebody says something that reminds me I need to add a section to address this issue.

At a point I will make a post to ask people to express their concerns, doubts, open questions about the power law.

Whenever I think I have covered all the topics for the book, someone raises a question that reminds me I need to add another section. At some point I will probably make a post asking people to share their concerns, doubts, or open questions about the power law so I can address them systematically.

One of the most common concerns is the following:

“The Bitcoin power law also appears when price is measured against other assets or currencies. Doesn’t that make the model trivial?”

This actually highlights an important point.

The power law works when Bitcoin is measured in most currencies around the world.

The reason is simple: the power law describes the process by which Bitcoin emerges from the fiat monetary system, so expressing it in dollars is natural. The dollar is the dominant unit of account of the current system Bitcoin is interacting with.

But the power law also works when Bitcoin is compared with gold, real estate, oil, or many other assets.

Why? Because the Bitcoin power law spans eight orders of magnitude in price. Over the same period, most other assets have changed relative to each other only by factors of a few. Compared to Bitcoin’s scaling, these relative changes are essentially negligible. In that sense they behave almost like constants.

This is precisely why Bitcoin can become the best performing asset over long time scales. The scaling law governing Bitcoin’s growth is so strong that it dominates the comparatively small fluctuations between other assets.

Looking forward, if the power law continues for another twenty years, Bitcoin would grow by roughly two additional orders of magnitude. Very few assets in history have changed their relative value by that much over similar time frames.

So the conclusion is not that the power law is trivial. It is the opposite:

Bitcoin’s scaling dominates the system so strongly that the choice of comparison asset becomes largely irrelevant.

This is one of the most common concerns. We address it many times but I do need a put a section on this in the book for sure.

1) The power law works with most currencies in the world.

2) It is the story of how we leave the fiat monetary system so of course needs to be expressed in dollars.

It is the main story.

3) It works with gold, real estate, oil, any other asset you can imagine.

The reason is that the power law is scaling over 8 orders of magnitude and these assets at most changed relative to each other by factors of few so their relative change is meaningless to Bitcoin. It is all constant in a certain sense.

4) This is exactly how Bitcoin can be the best asset in the world. It beats over time all the others.

This applies in particular over the past but even in the next 20 years we are expecting other 2 order of magnitude and almost no asset will change that much.

So in summary it doesn't matter what asset you use as a comparison they are all power laws.

With the economy resilient, inflation sticky above target, and geopolitical tensions driving energy prices higher, I see limited room for the Fed to cut rates in 2026. That's fine by me. I'd rather Bitcoin grow in a high-rate world than get spoon-fed the baby formula of cheap credit.

#Bitcoin

There is a simple explanation for why #Bitcoin behaves more like a technology stock than gold: its market cap. At roughly $1.38T, its market cap is on par with top US tech stocks, while gold’s is around $30T.

It’s reasonable to expect assets with similar market caps to carry similar risk profiles. A higher market cap indicates greater liquidity and market penetration, and thus lower risk.

Of course, Bitcoin is unique in having a much higher beta than tech stocks. But that also comes with proportionally higher growth potential.

Holding #Bitcoin in a hardware wallet is the most amazing feeling ever. It’s truly the first invention of real property rights made possible purely through math and sheer human ingenuity!

Financialized paper Bitcoin can deal massive damage in the short term. But to think it can destroy or neuter Bitcoin is foolish.

Manipulating markets always comes at a cost to the manipulator. In the long term, the real economics of supply and demand always take over.

With Bitcoin, the supply is set in stone. Nobody can change it. And there will always be growing demand for a decentralized, sovereign bearer asset that can be cheaply transferred at volume to anywhere on earth with near-instant settlement.

#Bitcoin

One of my intuitions about Bitcoin’s price mechanics is that of a stretched rubber band:

- Rubber is an incompressible material, meaning its volume remains constant under deformation. This reflects Bitcoin’s finite supply.

- An increase in length results in an equivalent reduction in thickness. This is akin to the distribution of available coins from existing users to new holders.

- The energy stored in the rubber band is proportional to the square of the extension. This is akin to Metcalfe’s law, which states that price (equivalent to energy) is proportional to the square of the number of users.

#Bitcoin

@thesecondrei1 The security will drop (more or less) to the level it was at that price.

Of course you have to take halving and increase in mining efficiency into consideration.

How a price crash can actually benefit some miners – Bitcoin's hidden antifragility

Consider a simplified Bitcoin network with only two miners. Bitcoin price is $100k, block subsidy is 100 BTC per day.

Assumptions:

- Miner 1: 90% of total hashrate, production cost $90k per BTC

- Miner 2: 10% of total hashrate, production cost $85k per BTC

At $100k per BTC:

- Miner 1 profit: (100 – 90) × 0.9 × 100 = $900k per day

- Miner 2 profit: (100 – 85) × 0.1 × 100 = $150k per day

If price crashes to $88k per BTC:

- Miner 1 stops mining (no longer profitable)

- Miner 2 stays profitable and captures the full 100 BTC subsidy: (88 – 85) × 1 × 100 = $300k per day

Despite the price crash, Miner 2 becomes more profitable.

Furthermore, although network hashrate drops 90%, overall efficiency increases. When price and hashrate eventually recover, the network is more resilient than before.

The same dynamic applies to a network with millions of miners.

This is the beauty of Bitcoin’s antifragility!

#Bitcoin