$RW.V worth a look. High-growth vertical SaaS: +33% ARR in ’25, NRR +119%, FY25 profitable, net cash, 43% insider ownership. Trades at ~1.6x my est. ’26 ARR. Non-ARR service rev decline masks ARR growth. Priced for AI disruption; I think AI enhances/expands the offering. Illiquid

Got a quick update out on $EVC. I have been pounding the table on this one for over a year now. Stock is up 80% after hours and is likely still undervalued here.

When you are vocal about an investment, others often follow your lead.

It is a mark of true integrity to update the community when your thesis changes, especially when you provide the facts to back it up. This is what gentlemen do.

Disclosure: I am long $SLYG

As I said since day 1: one thing is what you say, another is what you aim. Aim is proven by actions.

If you are a gentelmen, knowing the ppl for years, and you move apart for X reason, you shut up. This only knowingly damaged the ppl you’ve been with for years: mgt and friends.

@sergimp16 I do honestly not understand your hate and attacks against former $SLYG investors that sold and very well reasoned their reasons why they did so...

I think it's completely unnecessary and unfounded.

@Kreuzmann13 Could you a little bit elaborate on the "understanding the change and acknowledging what is happening there"?

Otherwise, are you not afraid of the weak and weakening JPY? Exchange rate JPY/USD for last 1Y is about -7% and for 5Y about -32%.

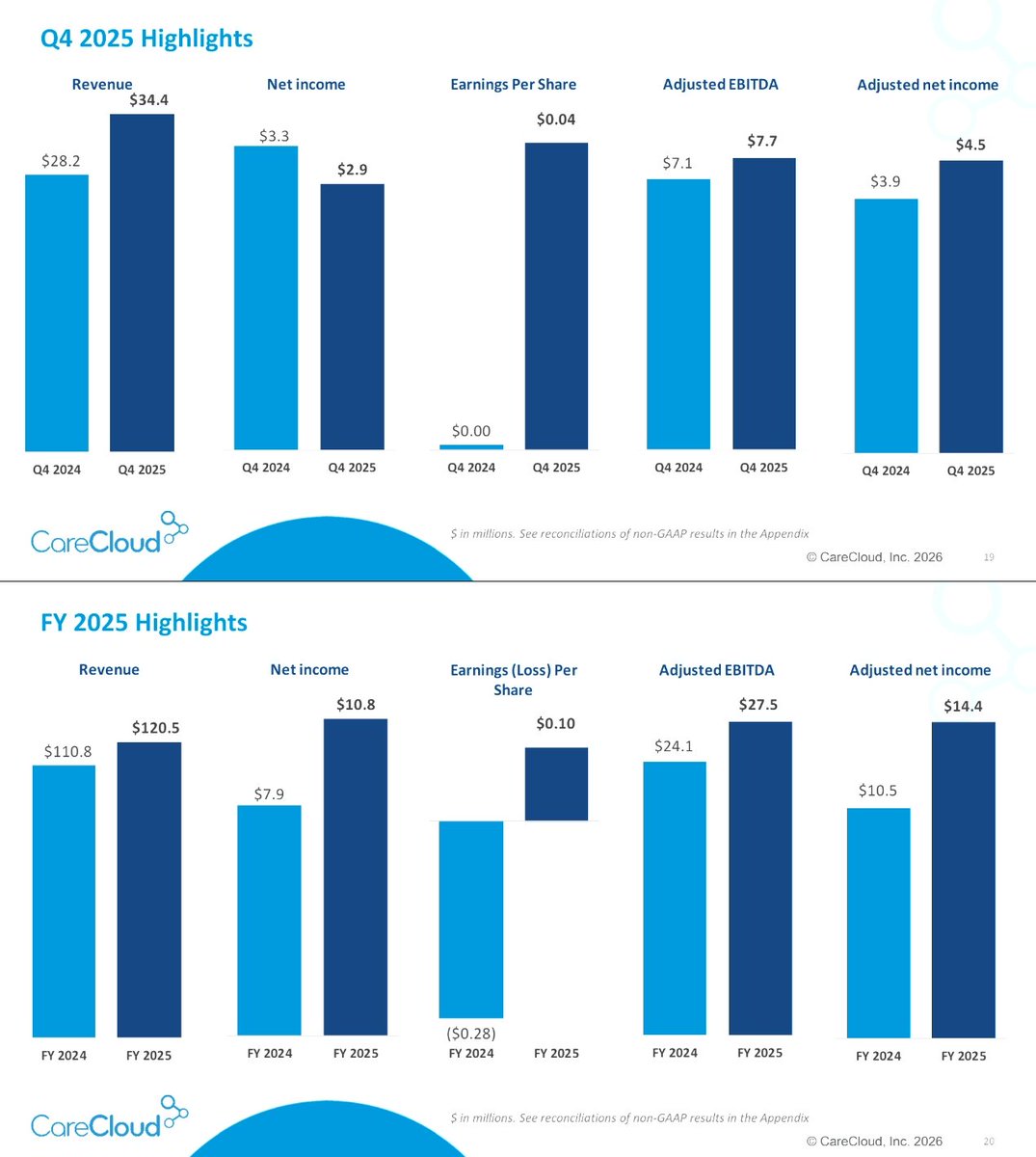

$CCLD: great results, solid growth, and they’re projecting another year of high single-digit to low double-digit growth for 2026. Importantly, that doesn’t include any unannounced acquisitions—it’s based solely on the current business.

They also noted they’ll remain active on the M&A front, and buying at ~1x revenue or lower, as they’ve done, should provide a meaningful lift. AI products are starting to become a key theme going into next year, and margins should continue to improve.

There’s a lot of room to come in above current guidance—I think it’s very conservative. Cash generation is strong, valuation is around ~5x FCF, and it should be a big beneficiary of AI, not a loser like the market is pricing in.

Great company, still underappreciated by the market.