People don’t appreciate enough how easy it is to pick winners right now.

The best thing about this horrible market over the last 1-2 years is that you can finally see who actually means it.

Anyone can build when the chart is green and the whole market is flying. What people take for granted is how hard it is to keep going when your token is down -90%, your community and investors turn on you, and every excuse to quit is sitting right there.

The founders still standing after a market like this passed one of the toughest filters there is. And that filter tells you almost everything you need to know about who’s worth backing.

@ThePumponomics this post hits home for me, have been using every llm for the past 6 months trying to improve my trading and its made it worse.

instead of paying attention to the markets, ive been playing with every llm and just ended up going in circles

We've been quiet recently because Mark Goodwin and I have been working to write the most comprehensive investigation into Polymarket's origins and ambitions to date.

We found that Polymarket's "official" origin story, that Shayne Coplan founded the company alone in 2020 and then built "the company in his bathroom", is a lie. Polymarket really started years earlier as another company called TokenBnk that was deeply tied to Israeli interests, specifically a crypto company founded by Benjamin Netanyahu's niece and nephew. Coplan has actively tried to obfuscate this company from his story and it's not the only thing either.

In Part 1 of this two-part series, we unravel the real history of Polymarket, directly connecting the company to Peter Thiel's efforts to resurrect controversial DARPA programs from its now defunct Information Awareness Office. Polymarket appears to have been chosen by Thiel and his associates to succeed in resurrecting DARPA's Policy Analysis Market where another Thiel-linked company, Augur, had previously failed.

Stay tuned for Part 2, where we explore the current influence of prediction markets and Polymarket, including how an insidious effort to have prediction markets replace representative democracy as a governance model is already being slowly implemented by the White House.

Read Part 1 here: https://t.co/xTmU5RzoZz

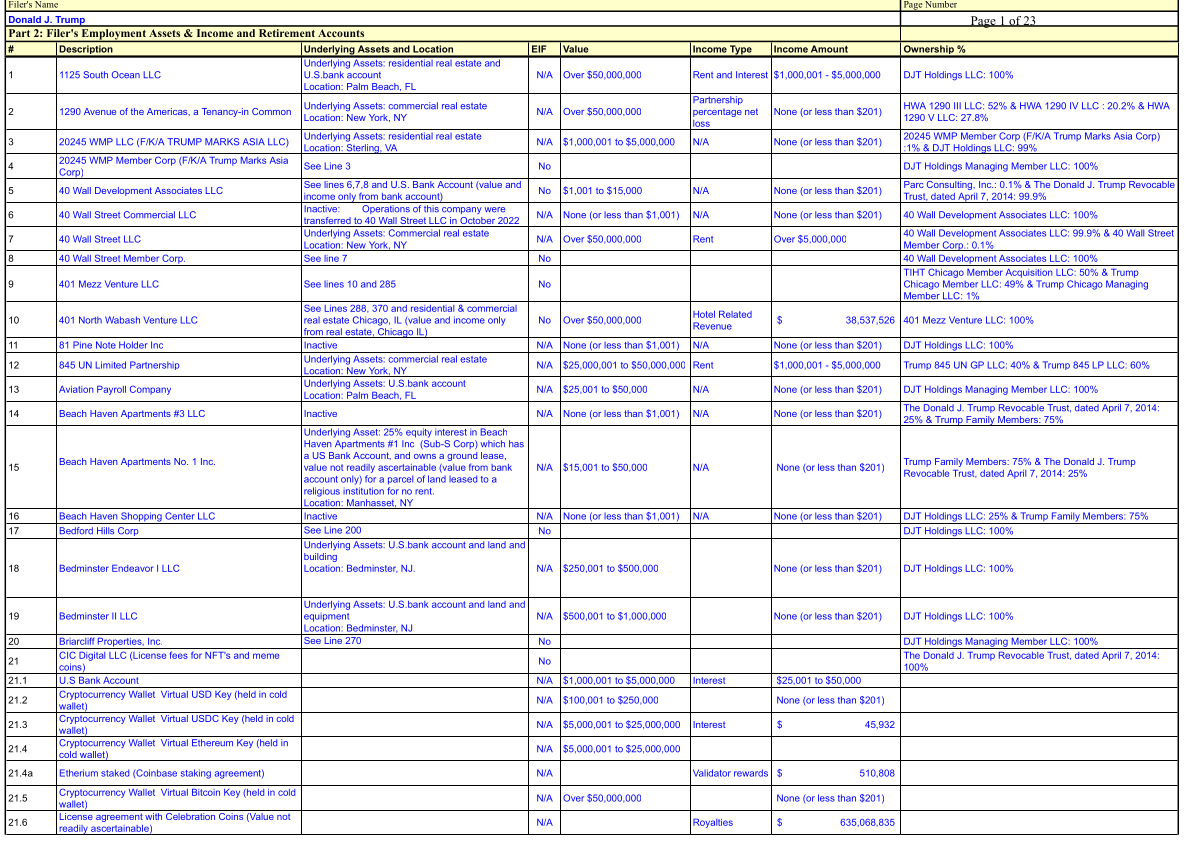

I analysed the 900+ pages of the Trump financial disclosure report.

He extracted 1.1 BILLION from crypto, divided like this:

> $635.1M → TRUMP memecoin

> $236.3M → WLFI token sales

> $196.9M → Sale of ownership interests in the USD1 stablecoin venture

> $65.6M → Sale of part of Trump's stake in World Liberty Financial

> $6.0M → Melania Trump's NFT sales and collectibles business

> $1.82M → Ethereum validator (staking) rewards

The biggest scammer of all time

The MSTR unwind probably plays out like this.

MSTR buys BTC by issuing shares and preferred (STRC). When this runs in reverse:

- Faith in MSTR as a BTC vehicle fades, mNAV drifts below 1x

- STRC trades at a widening discount as the market sees dividend coverage getting tight

- Both equity funding routes are now shut, so the ~$1.5 - 1.7bn preferred coupon comes out of cash first, then BTC sales

- BTC and MSTR de-rate further, which worsens the 'impaired vehicle' market perception

- BTC drops as the market front-runs those future sales

- If BTC sits below ~$40k long enough (roughly where coupon-funded selling starts looking material), and the 2027-28 converts can't be rolled or settled in stock because the price is too low, you get forced treasury liquidation

MSTR can survive a wick under $40k - it's a sustained BTC weakness that does the damage in theory. BUT just the possibility is enough to spark panic selling, and it's the elephant in the room for onboarding any new investment

On size:

- MSTR holds ~4.25% of total supply, closer to 5%+ once you strip lost/dead coins.

- Glassnode puts illiquid supply at ~14-15M BTC, leaving a liquid float of only a few million, so their stack is plausibly a double-digit % of that.

- 1% orderbook depth is ~$100M against ~$50B of holdings. If the market decides that MSTR is selling, that depth will decrease significantly, with lots of front-running.

The issue is, in theory this plays out as a slow grind down, but in practice it probably resolves quickly as the market prices it all in real time and frontruns it all

Mechanically it's nothing like LUNA, which had an in-built destructive downside mechanism. But for the reasons above, I think things could play out almost as brutally fast. Does it happen now? I have no idea

One silver lining though- BTC looks far more attractive once the MSTR unwind takes place and the holder base broadens. But there's a whole lot of pain to navigate first

Open source is taking share from the frontier models on the OpenRouter platform. This has ignited a mini-AI panic.

To us, it seems overblown. First, OR is not a representative sample.

But, more importantly, frontier token pricing on OpenRouter has surged this year.

@fernavid

Three confidential witnesses (CW-1,2,3) might bring down @Pumpfun

CW-1 was an early core member of the pump team and has come forward with damning internal telegram chat logs

CW-2 has handed over a “KOL contract” and indisputable evidence of Pump insiders dumping on all of us

pump’s only argument to dismiss these claims is based in 2016 case law that confidential witness allegations “should be discounted”

they did not deny any of it and i fear this is only the tip of the iceberg

pump has never treated us like part of the team; we were always the product

@KosherIslam@brucefenton If they were doing that now, I would be against it too.

Why does it take a specific religion for you to find land theft unacceptable?

@asklivermore has been all over my feed lately and I decided to look into him to see if his results match up with his claims.

so i scraped his entire X feed, pulled every stock pick he's posted, and ran the numbers against SPY over the same holding period.

what i found doesn't match what he's selling...

red flag #1: backtest doesn't match the marketing.

188 long picks over 51 days. 34.6% beat-SPY rate. worse than a coin flip. median pick 0.0% ROI.

meanwhile he's tweeting "i will make each one of my subs a millionaire" and "if you follow me, you will retire in a few years. i guarantee it."

his own data says otherwise.

red flag #2: language contradicts the website disclaimer.

site terms: "does not provide investment advice... should not be construed as a recommendation."

X feed: millionaire guarantees, numbered pick lists, retirement promises.

red flag #3: domain age doesn't match the claimed track record.

WHOIS shows https://t.co/c1uC4Inwap registered 2026-03-20. 58 days old.

homepage advertises performance "since inception (Jan 2025)."

14-month gap with zero explanation. either the inception date is fabricated or there's an undisclosed prior platform.

NEW POD: The Warsh Fed Will Look Nothing Like Before

We Cover:

🔸 Warsh's hawkish debut

🔸 The end of forward guidance

🔸 New Fed task forces

🔸 Market reaction, risk assets & more!

@josephwang@fejau_inc

Links Below ↓

This is not a robotics thesis. It is a funnel.

Slick video, charismatic marketer, “why I bet my career on robotics.” He works for $BOT. RoboStrategy, the closed-end vehicle Andrew Kang now runs and openly brands the “MicroStrategy of robotics.”

Same playbook: a committed equity facility that only works if the share price stays bid and retail keeps showing up to absorb the issuance. The content is the top of the funnel. You are the liquidity.

We traded millions of dollars of converts on the real robotics names in the late 2010s, mostly within a convertible arbitrage mandate, not fundamental stock-picking. Which is exactly why we can point at the honest alternatives here, the ones nobody is cutting a hype video for, because there is no salesman making big bucks dumping them on you.

If you want robotics exposure, the honest version is already listed in Tokyo. FANUC (6954), 20%+ operating margins through full vertical integration. Keyence (6861), asset-light, ROE most software firms would kill for. Yaskawa (6506), the servo muscle behind half the world’s arms. The Japanese Big Five ship 40%+ of global industrial robots. These are priced for competence, audited for decades, and you can size them without praying a NAV premium holds. Dull. Real. Yours at a clearing price.

And if you actually want the convexity, the asymmetric leg, it is one layer down in the actuation supply chain, not in a closed-end fund. Harmonic Drive Systems (6324), Nabtesco (6268), the strain-wave reducer makers. A humanoid needs roughly 20 harmonic drives per unit, which makes precision reducer supply the binding constraint on the entire scaling story. That is where the torque is. That is also where you get your face removed if the shipment curve disappoints. Omdia has 2025 humanoid shipments up ~480% to ~13,000 units, real growth, and a rounding error against the valuations now leaning on it.

So here is the actual choice. You can own the cash-generating incumbents directly, at a price, with no wrapper skimming you. You can own the actuation convexity directly, eyes open, and underwrite the humanoid curve yourself. Or you can buy a single ticker at a premium to its own book, structured so the manager can print on your ‘enthusiasm’, and call that a career bet.

Robotics is real. The compounding is real. The funnel is also real, and it is looking for your money.

The edge was never finding the names. The edge is knowing who is selling, and to whom.

Andrej Karpathy spent 2h showing how he actually uses AI day to day

he's a co-founder of OpenAI and led AI at Tesla, so when he shows how he works, it’s worth watching

and the whole session is just him telling the machine what he wants in simple terms, like he's briefing a coworker

watch what's actually happening the entire time:

> he describes the task in normal words

> it goes off and does the work

> he glances at the result and nudges it with one more sentence

that's the whole skill, and you've had it since you learned to talk

the only gap between that and a worker that runs on its own is handing that sentence a schedule and the tools to act

check his work, then build the version that keeps working when you stop

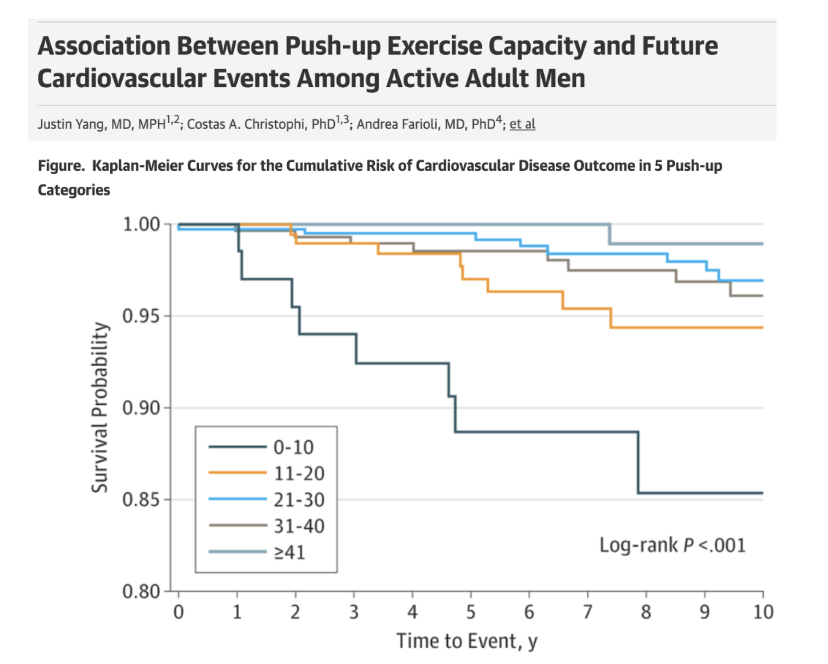

Men, take a break from whatever you're doing and see how many pushups you can do.

How many did you do?

It's a predictor of your heart disease risk.

. 20+ reps is linked to a 75% lower risk

. less than 10, you gotta get off dat ass

Data from 10 yr study of 1,104 men aged 21 to 66.

Pushups outperformed submaximal VO2max at predicting events, likely because pushups capture muscular strength and power on top of fitness, two of the strongest protective biomarkers known.

Limitations: the cohort was middle-aged male firefighters, so do not extend to women, older adults, or sedentary populations. The under 10 group was also older, heavier, and smoked more, so some signal is residual confounding by overall metabolic health.