1/ Just dropped: What's new in the **26/27 tax year** – exciting **NEW Platinum Modeller** + 1:1 Teams meetings with experts!

Now we well into the new tax year – our core modellers (Bronze/Silver/Gold) are undergoing final testing for release in 1st Quarter 26/27, plus major upgrades:

- NEW Gold Concierge: historic scheme pays analysis

- Enhanced 'TRS view' at YOUR chosen retirement ages (with historic & existing scheme pays)

- **NEW Platinum Concierge & charts** – project your pensionable pay (all 4 nations), and test impact of promotions, salary sacrifice

- 5 exciting new charts (see the video and tweets below) helping you navigate partial retirement / R&R and tax through to seeing if strategy meets your cash flow & net pay targets +/- state pension

Also a rundown on some depressing news on public sector pensions here, including what Reform have got planned for public sector pensions 👇

https://t.co/LrZ8OUYe8K

Register interest for 26/27 modellers (be first in line!): https://t.co/xwAun9BU40

#KnowYOURnumbers Pls RT / share

@goldstone_tony It’s simply unreasonable to expect a salaried NHS employee to waste their time on this. If NHSBSA provide the data we can declare it. Otherwise life is too short.

17/17 If you agree change is needed, please share. Try not to stress about Annual Allowance—free help is available including our free growth tool. #NHSPension

https://t.co/Mt66LYfml8 #PensionTax

Hoping for real improvements in 2026! RT! #ItsTooComplicated

1/ Longtime followers may remember this update from 4.5 years ago. Id met the then head of @nhs_pensions and the senior leadership team. They made lots of promises to improve things around Annual Allowance that BADLY needed improvement....

Pls read, share and RT

@goldstone_tony Hi Tony, I can see via my 05 pay & service extract that the pensionable pay has likely been adjusted and would account for the appropriate allocation. Would the modeller then ideally use the 05 amounts instead of payslips for accuracy (& save money)? Thx

IMPORTANT: Many of you will soon be opening brown envelopes and seeing some pretty large numbers for 24/25, which can be scary. Others will be modelling them if you haven’t received a statement yet because the scheme failed to send it within the legal timeframe (you can model growth for free here: https://t.co/xwAun9BU40).

But it’s important to remember a few things.

You have a charge because your pension has increased significantly. I know it feels unfair—as it’s correcting years of prior erosion—but that’s one of the many problems with the Annual Allowance.

Please don’t lose sleep over the Annual Allowance. It might not be as bad as you think (so model it, and remember carry forward, for many there will be significant carry forward in 23/24 especially for hospital doctors due to #negativePIAs which many people have been lobbying for many years!). Some people will have the ability and choose to pay; others may opt for Scheme Pays, through choice or necessity.

I previewed my Scheme Pays analysis a few months ago in a YouTube, and hopefully it will be available shortly as an add-on to my free or premium modellers (sneak preview below). Scheme Pays has a lot of moving parts—because the interest depends not only on rates but also on when you plan to retire from each scheme. There isn’t a single “Scheme Pays impact”; it’s dynamic and varies based on several factors including several things that may change including when you want to retire, and also your health. None of 👇 is advice, its just to help you understand your numbers. Some people way wish to get formal financial advice i.e. from an IFA around this decision.

Also remember to consider whether you can do anything THIS tax year we are in which may also see big growth numbers for many—can you avoid tapering, or should you ignore it and carry on? Scheme Pays may not be as bad as feared (and has improved versus a few years ago for technical reasons), so you need to #KnowYourNumbers and #ModelYourPension to make an #informedchoice.

Last but not least, remember that despite its many problems—including catastrophically poor administration and the Annual Allowance being poorly suited to schemes like the NHS—it’s still a good scheme. Leaving the scheme is almost never the right decision.

Here’s a sneak peek of what’s hopefully coming soon as an #AddOn 👇, so model your numbers today and sleep better knowing your position. Remember there is no downloadable model this year - the only way you can get it is by registering at https://t.co/xwAun9BU40 !

Please share/RT with people who are struggling.

16/16 IMHO Mr. Crossley & Quliter should apologize and retract the previously supplied figures; and the Times should retract the article in full. Pure propaganda with little grounding in truth nor reality.

Poor modelling & poor jounralism. RT if you agree

Many doctors are struggling with pensions annual allowance figures due to a lack of pension savings statements from the NHS. Many will be hit by tax traps in 25/26 and are wondering if they can do anything ? You need to know your numbers. If that’s you 👇

1/ 🚨 BREAKING: The September CPI has just been announced at 3.8%! 📈 This key September CPI figure (Aug 2025: same at 3.8%; Sept 2024: 1.7%) directly influences public sector pensions, taxes, and more. Details below… #Pensions#CPI

https://t.co/JpFasHj65C

Grateful @TheIFS@IsaacDelestre answering my question (upvoted to most popular) on their view on ridiculous tax cliff edges such as £100k & AA taper

Answer from the IFS - "we hate them"

And a clear message to @RachelReevesMP they would like her to address them

RT if u agree!

V. topical story below @SkyNews on £100k tax trap which is hugely destructive for NHS productivity as discussed with @TorstenBell previously & @TheIFS last week

Ive been working on NHS modeller for a while. Sneak preview👇

Pre-register if interested https://t.co/R9E2afEUB0

RT!

"Surfing competition abandoned after sewage is dumped off Cornwall."

What a headline for the nation the 2025 English Inter-club Surfing Championships, abandoned due to sewage dumping. 🫨

https://t.co/WmABVW4RCr

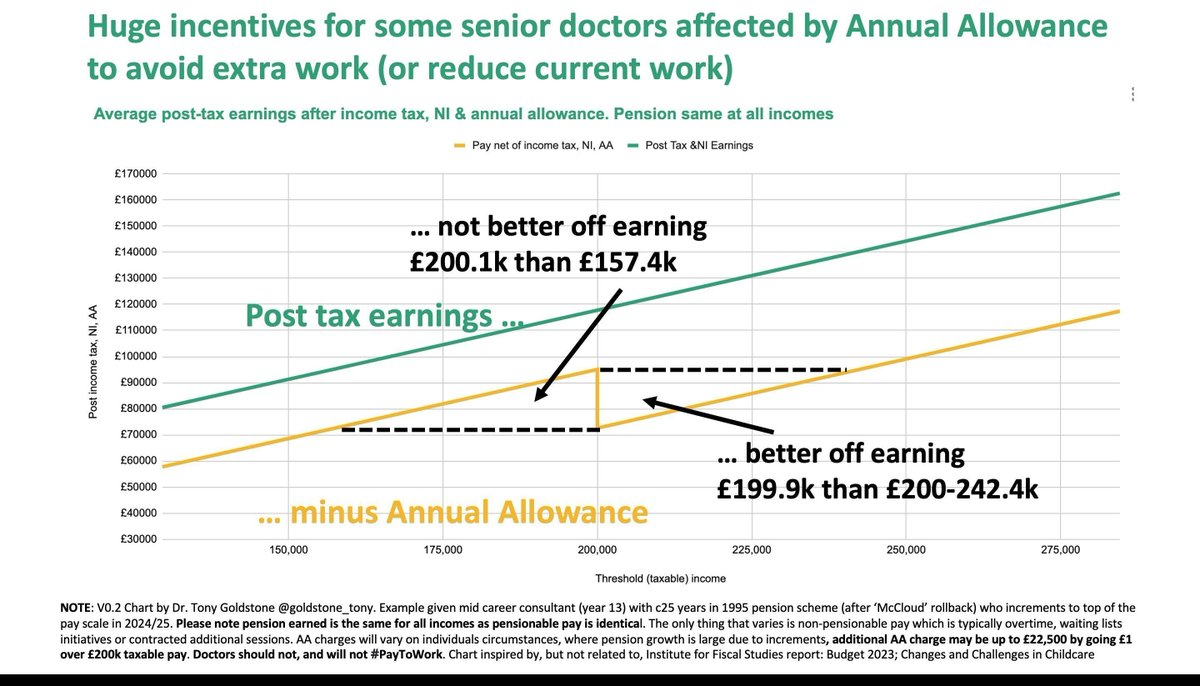

⚠️Lots of threads/posts on tapering, threshold, adjusted etc. Now we have March payslips can I tell you how I would approach it

1️⃣ Get your March 25 payslip. Note your YEAR TO DATE TAXABLE Pay. *IGNORE* gross pay and for now IGNORE pensionable pay. Dont use gross income and deduct pension contributions - the "taxable pay" already has them deducted so dont deduct it again.

2️⃣Do *NOT* add back in salary sacrifice for things likes cars and childcare. You are required to add in "relevant salary sacrifice arrangements made after 8 July 2015" - the key word here is relevant defined as "the individual gives up the right to receive general earnings or specific employment income in return for the making of relevant pension provision," - so DONT add cars etc back in.

3️⃣So you now have your NHS taxable income for the year. Now you need to add any other taxable income - think other PAYE, private practice, property, BIK, dividends, interest etc. Basically anything else that is subject to income tax. Less employment related Income Tax Reliefs claimed via tax return i.e. GMC, BMA, MDU etc

4️⃣Do NOT take off gift aid for normal charitable donations which is another common mistake Ive seen experts make. Note you can do this for the ridiculous £100k cliff calculation, but not threshold/adjusted

5️⃣So your NHS taxable income plus all other taxable income, less any other NON NHS pension contributions i.e. a SIPP, is THRESHOLD INCOME.

If this is below £200k you are not tapered and have the full £60k allowance and any carry forward (use the HMRC carry forward calculator to work out if you have carry forward - you will have needed both your RPSS to the 22/23 tax year and 23/24 PSS to work this out, latter obviously also delayed in England & Wales - you can estimate 23/24 using the tool below).

6️⃣If threshold income above £200k you need to work out ADJUSTED INCOME. You wont find out your PIAs for 24/25 until October 2025 but can estimate them using the link to the free tool and video below. If you are in 2008 its a bit more involved, and I wouldnt advise the NHS Employers modeller for this as for 2008 it ignores reckonable pay so is wildly innacurate. Adjusted income is THRESHOLD plus deemed PIA pension growth accross both schemes plus any other pension growth or SIPP contributions etc. The free tool below will help you calculate this.

7️⃣The free tool below will help you estimate your threshold and adjusted income, so see if you can expect a liability for 24/25 (due Jan 26, scheme pays Jul 26)

WHY IS THIS SO IMPORTANT in 24/25

Because of the 23/24 pay award paid in 24/25 and DDRB 24/25 many people will have VERY LARGE PIAs - Im year 14 (just) and my PIA is over £150k. That means if you go over THRESHOLD income, when you add in the PIA, tapering can be BRUTAL and reduce your allowance from £60k down to £10k - that might increase your AA tax charge by £22,500 (45% x £50k reduction).

So if your THRESHOLD income is CLOSE to £200k you can still DURING THE TAX YEAR ONLY i.e. the next 9 days or so make a SIPP payment to reduce it below threshold income to avoid tapering. Say your THRESHOLD income (step 5 above) is £210k you could make a £11k GROSS SIPP payment which would reduce your threshold income to £199k which could reduce your AA liability by £22.5k making the SIPP free.

See the worked examples in the video below

Free tool and video to work all this out is below

Free Tool: https://t.co/rVC2FzNF84

Self help video: https://t.co/UB9dqIyke5

Ok March '25 payslips landed so now you can more accurately work out threshold income. And also estimate pension growth if tapered now 24/25 pensionable pay known.

There will be some BRUTAL PIAs this year (24/25). Make sure you #knowyournumbers & understand this graph👇

Still 10 days or so to reduce your threshold income if you are just above. Free tools and video below. Dont delay! Pls share with colleagues not on social

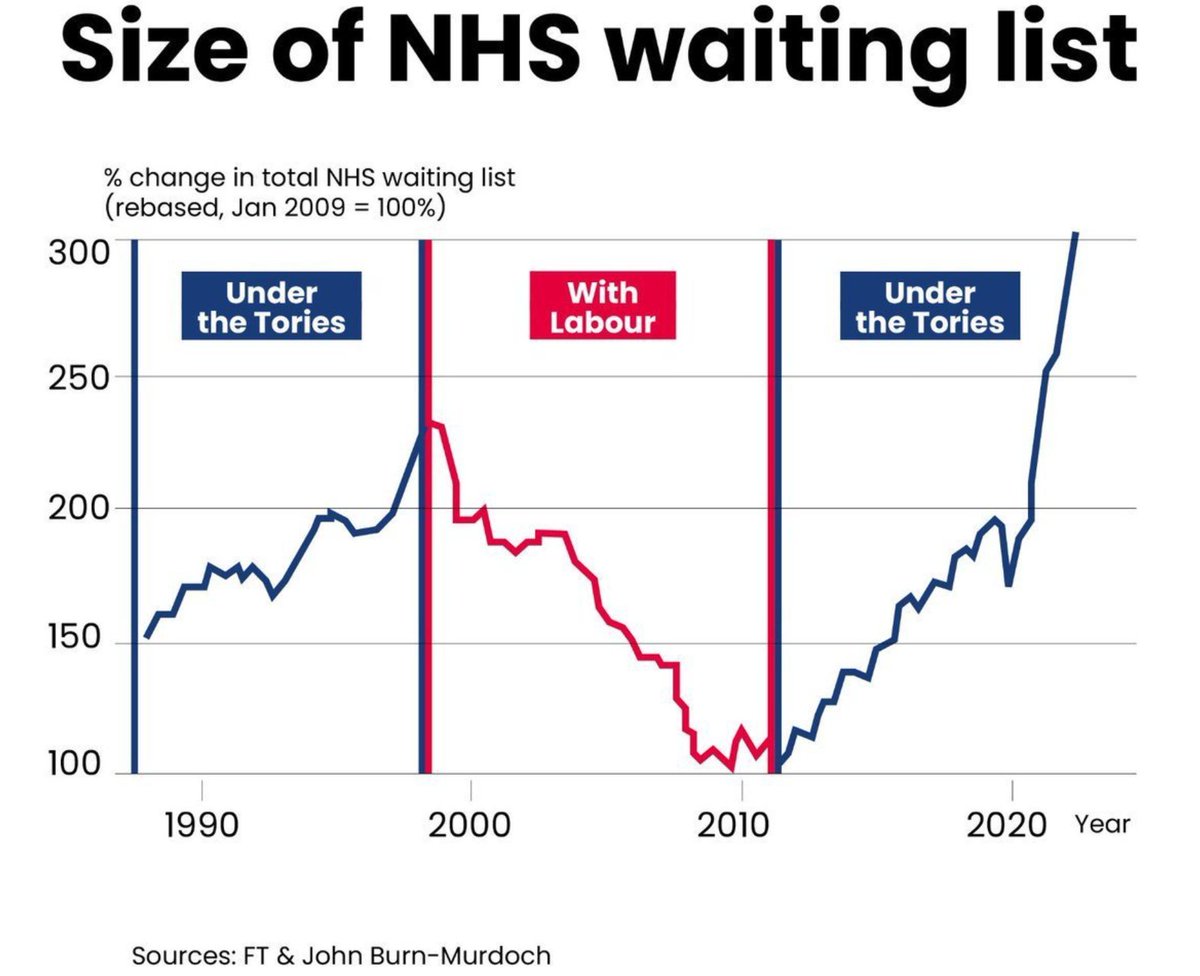

Our pensions survey has revealed that pension tax rules are potentially reducing NHS waiting list capacity by almost 10%. No one should be #payingtowork, the Government must scrap the annual allowance taper - https://t.co/KFeQVirrqG

1/3 BREAKING: See results from our #pensiontax survey 👇

-1/5 reduced regular o/tdue to #Taper

-1/4 reduce "ad hoc" o/t

- Loss of 5,400 consultants worthof capacity @wesstreeting - 9.3% of consultant workforce

Thats a huge amount of capacity that could improve #WaitingLists👇