$KTA : Review

A member of the Abu Dhabi Royal Family just created a joint venture with a blockchain project to tokenize tens of billions of dollars of Gulf commodities and modernize cross-border payments across the Middle East, Africa, and Asia.

Meet Keeta Network - a Layer-1 blockchain designed to unify global payment networks through built-in KYC/AML compliance, cross-chain settlement, and 11.2M TPS verified by Google's Spanner team.

Founded by ex-BrainBlocks and Nano veterans. Backed by former Google CEO Eric Schmidt. And as of today, partnered with ASK Group, a UAE-based investment group led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan, to build a public exchange for tokenized Gulf commodities targeting 2027.

Let's explore what just happened and why it matters. 👇

🔵 The ASK Group Partnership

This is the kind of announcement that redefines a project's trajectory overnight.

Keeta and ASK Group, led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan, have created a joint venture aiming to tokenize tens of billions of dollars of commodities and modernize cross-border payments in the GCC region and beyond.

Key details:

➛ The joint venture is working toward establishing a Keeta-powered public exchange for tokenized Gulf commodities, with an initial target of 2027, subject to regulatory approvals and the establishment of custody and operational infrastructure.

➛ Every barrel of oil, ounce of gold, and kilogram of silver will be represented as a digital token on the Keeta network, bringing 24/7 settlement, instant fractional trading, global compliance, and verifiable proof-of-reserves to one of the largest untapped markets on earth.

➛ Global commodity markets move several trillion dollars annually. The GCC's share of the world's proven oil reserves alone represents an asset base whose tokenization would constitute one of the largest migrations of real-world value onto blockchain infrastructure in history.

➛ A retail investor in Tokyo, an institutional fund in London, or a family office in Singapore will have the same direct access to a barrel of Gulf crude or an ounce of UAE-held gold as the largest commodity trading houses have historically enjoyed.

➛ The UAE is one of the highest-volume remittance origination markets on earth, with the UAE-India corridor alone moving approximately $20 billion annually. Keeta's infrastructure will modernize cross-border payments to South Asia, Africa, Southeast Asia, and beyond.

➛ ASK Group holds exclusive rights to facilitate and execute Keeta's presence across the UAE, MEA, and India.

➛ This marks the beginning of a long-term relationship. Additional asset classes and use cases in the GCC region and beyond are planned.

⚪ Why This Matters

Let's put this in context. Keeta was already positioned as a compliance-first L1 targeting the TradFi-DeFi bridge. Eric Schmidt backing. 11.2M TPS verified. Bank acquisition pending. KUSD stablecoin incoming.

Now add: a joint venture with an Abu Dhabi Royal Family-led investment group to tokenize the Gulf's commodity reserves, one of the most valuable asset bases on earth. Oil. Gold. Silver. On a blockchain that does 11.2 million transactions per second with 400ms settlement and built-in KYC/AML.

At $0.20 per token and a $113M market cap, KTA is valued at less than the annual remittance volume of a single UAE-India corridor ($20B). The commodity markets this joint venture is targeting move trillions annually. If even a fraction of 1% of Gulf commodity tokenization flows through Keeta, the current market cap looks microscopic.

⚪ Keeta at a Glance

Keeta is a Layer-1 blockchain designed to unify global payment networks. Built on a DAG-based architecture with dPoS consensus, it enables cross-chain settlement, RWA tokenization, and built-in KYC/AML compliance.

$KTA trades at $0.20 as of June 9, 2026, up 35% in the last 24 hours on the ASK Group announcement. Market cap: $113M. Circulating supply: ~513M out of 1B max.

➛ 11.2M TPS verified by Google's Spanner engineering team and Chainspect ➛ 400ms settlement times ➛ Built-in KYC/AML compliance at the protocol level ➛ DAG-based architecture with dPoS consensus ➛ Native RWA tokenization and digital identity tools ➛ Cross-chain settlement layer ➛ Bank acquisition pending regulatory approval ➛ Upcoming: KUSD stablecoin, Keeta Pay, Keeta Card, native DEX ➛ Backed by former Google CEO Eric Schmidt ($17M at $75M valuation)

🔵 Meet the Keeta Team

Keeta is led by crypto payments veterans from BrainBlocks and Nano, backed by former Google CEO Eric Schmidt, and now partnered with an Abu Dhabi Royal Family-led investment group for sovereign-scale commodity tokenization.

▶️ Core Members:

➛ Ty Schenk [ @schenkty ] - Founder & CEO | Software engineer, ex-BrainBlocks co-founder, ex-Turo, ex-Steel Perlot. Forbes 30 Under 30. Designed Keeta to make cross-border payments as simple as Venmo. Now leading a joint venture with Abu Dhabi royalty to tokenize Gulf commodities.

➛ Roy Keene - CTO | 16+ years in systems engineering. Former lead developer at Nano Foundation, former Senior Cloud Architect at AWS. Brings deep blockchain architecture and cloud infrastructure expertise. Built the 11.2M TPS engine.

➛ David Campos - Head of Operations

➛ Josh Kleiman - General Counsel

🔵 Ratings

➛ Use Case: ★★★★★ (5/5) - The ASK Group partnership elevates Keeta from "promising compliance-first L1" to "the blockchain that an Abu Dhabi Royal Family investment group chose to tokenize Gulf commodities." Oil, gold, silver on-chain with 24/7 settlement, fractional trading, and proof-of-reserves. Cross-border payments modernization for the $20B UAE-India corridor. Combined with 11.2M TPS, 400ms finality, built-in KYC/AML, Eric Schmidt backing, and the pending bank acquisition, Keeta now has the most significant real-world asset pipeline of any L1 outside of Ondo and Stellar. Upgrading from 4.5 to 5.

➛ Tokenomics: ★★★ (3/5) - Unchanged. 1B supply, 50% community allocation is decent, but 40% insider allocation (team + investors) and no burn mechanism remain concerns. The ASK Group partnership should drive significant future demand for KTA as the settlement token for tokenized commodities, but that's 2027+ timeline.

➛ Audits: ★★★★ (4/5) - CertiK audited. Stress test verified by Chainspect and Google Spanner team. Strong security positioning for an L1 targeting institutional finance and now sovereign wealth-adjacent commodity tokenization.

➛ Community: ★★★★ (4/5) - 235M testnet wallets, 42M active wallets, 13+ exchange listings, growing social presence. The ASK Group announcement drove 35% in 24 hours, showing the community responds

to real catalysts. Active Twitter Spaces and engagement from the founder.

🔵 Conclusion

One hour ago, Keeta Network went from "compliance-first L1 backed by Eric Schmidt" to "the blockchain that an Abu Dhabi Royal Family-led investment group is using to tokenize Gulf commodity reserves." That's not a partnership announcement. That's a sovereign-adjacent endorsement of Keeta as the infrastructure layer for one of the largest migrations of real-world value onto blockchain in history.

The numbers speak: trillions in annual commodity flows. $20 billion in the UAE-India remittance corridor alone. Exclusive rights across UAE, MEA, and India. Public commodity exchange targeting 2027. Oil, gold, silver as on-chain tokens with 24/7 settlement, fractional access, and proof-of-reserves. All running on a chain that does 11.2M TPS with 400ms finality and built-in compliance.

At $0.20 and $113M market cap, 35% up today, KTA is either the most undervalued infrastructure play in the RWA space or the market hasn't had time to process what just happened. Given that this announcement is one hour old, the answer is probably the latter.

The question isn't whether tokenized Gulf commodities are a big deal.

They're potentially the biggest RWA opportunity in the world. The question is whether Keeta and ASK Group can execute on the 2027 timeline.

If they do, $113M market cap for the blockchain powering trillions in commodity tokenization will look like the buy of the cycle.

I see a lot of people talking about Keeta Personal in extremes right now.

One side says it’s just a wallet update.

The other side thinks the entire global financial system changes overnight on May 22nd.

I think both takes are missing the point a bit.

Based on the previews, screenshots, Ty’s teaser, Gabe’s update, and what the team has already publicly shown, this clearly looks like a lot more than a normal crypto wallet:

• multi-currency global accounts

• native fiat balances

• SWIFT / ACH / Wire functionality

• Visa Direct payout rails

• token + fiat interoperability

• stablecoin funding and withdrawals

• cross-chain compatibility

• on-chain FX conversion

• identity tied directly into transfers

• SDK infrastructure developers can build on

• shared/member account structures

• direct banking integrations

The bigger thing I think people are overlooking is that Keeta Personal is the consumer-facing side of a much larger network/infrastructure play.

That’s where this starts getting really interesting long term.

The Anchor and SDK model means every new institution, payment rail, banking integration, or Anchor potentially expands what the ecosystem can do:

• new markets

• new currencies

• new banking rails

• new payment options

• new settlement routes

• new apps and services built on top

A simple example with Keeta Personal could be someone holding USD in their account, instantly converting it to another currency, and sending it globally through integrated rails without needing separate exchanges, apps, or traditional multi-day bank wire settlement.

Realistically, if ACH/Wire functionality, IBAN accounts, Visa Direct payouts, fiat deposits/withdrawals, and FX conversion are actually live at launch, then there almost has to already be some level of banking, payment, liquidity, or Anchor integrations operating behind the scenes.

Obviously that doesn’t mean every country and rail is fully supported on day one.

A huge part of Keeta’s long-term growth will likely come from new Anchors expanding supported rails, institutions, payment options, and overall network functionality over time.

That expansion takes time, which is why Ty building the AI Anchor deployment tool matters. It potentially allows the network to scale much faster.

I’d also expect parts of the broader ecosystem like Keeta Business, Keeta Checkout, tokenized stocks, and the T-Bill product to continue rolling out over time as the network expands.

So set expectations accordingly.

Don’t expect every part of the long-term vision to suddenly appear overnight.

But also don’t dismiss this as “just a wallet update,” because based on everything shown publicly so far, this looks like a very meaningful step forward toward what Keeta is actually trying to build.

The future looks bright.

@KeetaNetwork keeta:native

(3/8) Keeta will support Visa Direct rails for outbound payments.

This enables:

• Payouts to 190+ countries over 90+ rails

• Near-instant settlement

• Instant funding/withdraw via linked debit cards

Users no longer need to wait on legacy banking rails for funding and payouts.

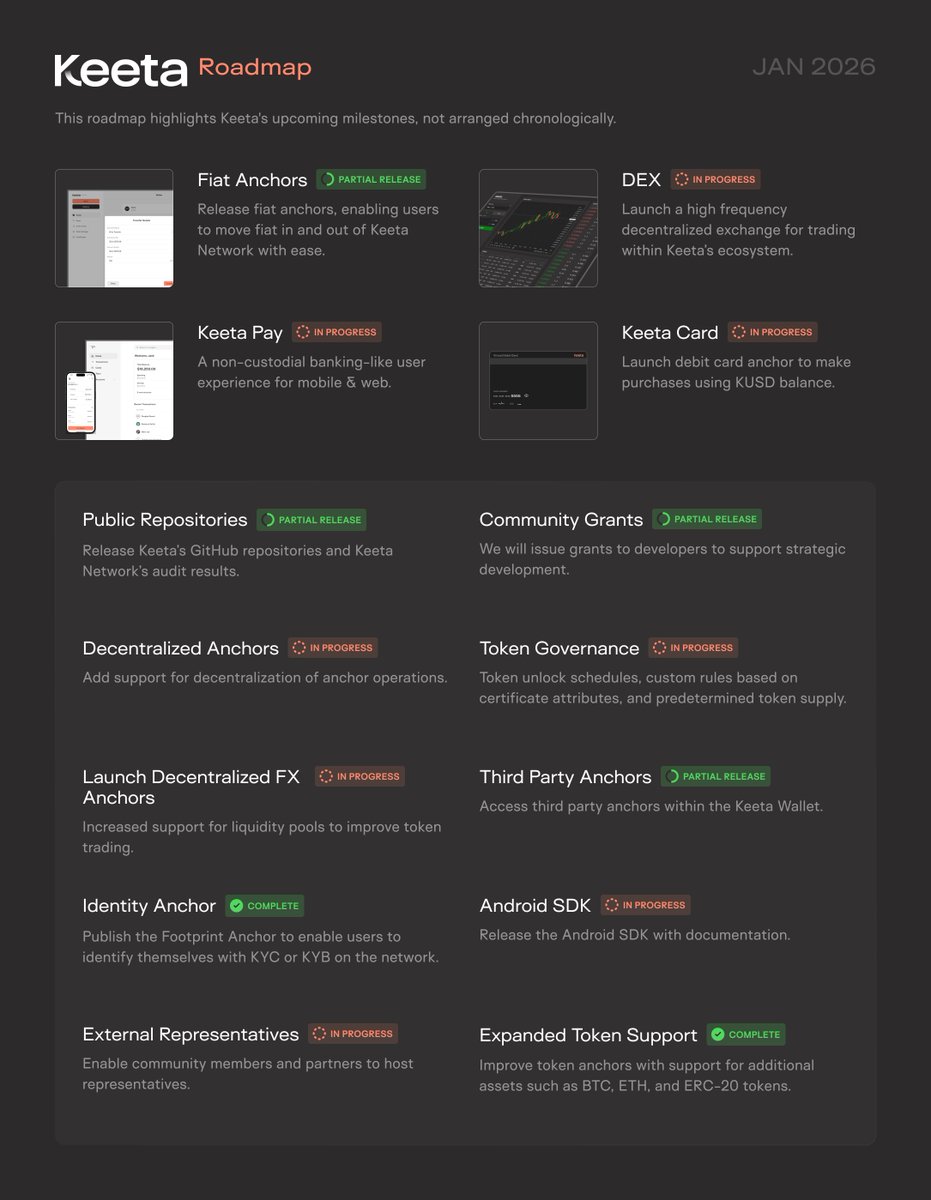

(1/8) Over the past few months, the team has been building and expanding Keeta's infrastructure across payments, FX, investments, and digital assets.

We’re now rolling out a series of major releases that significantly expand what Keeta Network can do.

See our new releases below.

Het is gelukt! Meer dan 41.000 stemmen op de petitie "vervang de vermogensaanwasbelasting door een vermogenswinstbelasting"

https://t.co/d9VzuxxJSq

Petitionaris: Freek van den Berg

Bedankt Freek! Aub aanbieden aan de @EersteKamer

Reflections on this bill from a Dutch citizen who has closely followed this process for years.

First: the old system. It was pretty simple: the government assumed that you make ~5% return on your assets per year. That return is then taxed (~35%). Assets include savings, stocks, crypto, etc. There is an exemption of ~€55.000 per person. Assets are measured on the 1st of January every year.

Imagine you hold one bitcoin worth €75,000. Subtracting the exemption leaves €20,000 taxable. The government presumes a €1,000 return (5%), resulting in €360 tax (35%).

In summary, this system is:

- Very simple to understand

- Low administrative burden

- Advantageous to investors where ROI >5%

- Disadvantageous to investors where ROI <5%

Savers fall into that latter group. Years of sub-5% interest rates led the government to overestimate savers' returns.

In 2021, the Supreme Court ruled that this was unlawful and that this needed to change. The government should calculate taxes based on the actual return on investment instead of the assumed return.

At this point, I want to make a few things clear:

- I don't mind paying taxes

- I think the Supreme Court's decision was correct

What I do mind is:

- Tax on paper gains

- Added administrative complexity for tax filings

- The Government is not listening to the advice of the Netherlands’ highest advisory body on legislation

- That the Tax Authority is pressuring the legislative process to make a quick decision

- Making obviously bad legislative decisions

And these are exactly the things that are happening.

For some reason, the Government decided against a capital gains-like system and chose an unrealized capital gains system.

This means that you pay tax on the paper profit you made during the year.

Let's say you have one Bitcoin on January 1st, valued at €70.000. On December 31st, Bitcoin is at €115.000. A return of €45.000. Taxes to pay: €15.750 (35%). No exemption in the new bill.

The problem: all your money is in Bitcoin.

But that is not a problem! That is what I want! That is why I stacked every single Satoshi I could since 2016. The same goes for stocks, gold, silver, or real estate: the goal is to have as little fiat as possible!

But in the short term, I have to pay €15.750 in taxes. In this example, it means I have to sell some of my Bitcoin (0.137 BTC, to be precise). After the tax, I'm left with 0.863 BTC (€99.245).

So on paper I'm doing fine (from €70.000 to €99.245 in a year). But my underlying assets are diminishing (1BTC to 0.863 BTC). The amount of Bitcoin, stocks, and gold in my portfolio is decreasing each year.

This creates a dilemma: I don’t want to sell. I expect bitcoin, stocks, and gold to rise over time. But I have to, because the Government demands it.

The obvious better choice was to tax when people decide to take a profit. I don't really have a problem with paying taxes on my realized profit. When I decide to sell, instead of being forced to sell when I don't want to.

I'm not the only one who thinks there are better options. The Council of State (the Netherlands’ highest advisory body on legislation):

"Don't do it. It's too complex (for both the tax authority and the citizens). Look for alternatives."

And still, the government marches on. And the House of Representatives 'reluctantly agrees'. What the fuck does that even mean?

"Yeah, we also don't like this bill, but we still are going to sign it into law."

It's batshit crazy. But it's where we are. That's what the quoted tweet is about.

Not all is lost, though:

- House of Representatives (2e kamer) still has to approve this bill (quote tweet is wrong here).

- Senate (1e kamer) still has to approve.

- The Tax Authority is unable to comply with this bill (too complex)

- Complexity makes this bill filled with loopholes

So, to sum it up: hopefully, Parliament comes to their senses and stops this monstrosity of a bill, and chooses one of the better options instead.

Keeta Network $KTA just took a major step toward becoming a real alternative to CEX's and this is just the beginning:

I used the @Stablecoin fiat on ramp to instantly on ramp some EUR, then used the new KTA/USDC and USDC/EURC pairs to swap between assets, all for a fraction of a cent fee ($0.00241) without ever leaving the web wallet.

These new pairs by @xescure effectively brings CEX level functionality directly to @KeetaNetwork. You can go from USD or EUR to KTA (and other assets) in seconds, with fraction of a cent in fees, without dealing with the usual exchange headaches: delayed deposits, frozen accounts, custody risks, or need to even create an account on an exchange.

You remain in full control of your assets at all times, with seamless, frictionless access to use and move them however you want.

👇Try it yourself (1/2)

Most financial institutions don't touch crypto because they can't.

Banks need private flows and verified accounts with full transaction attribution, which is opposite to what public blockchains offer.

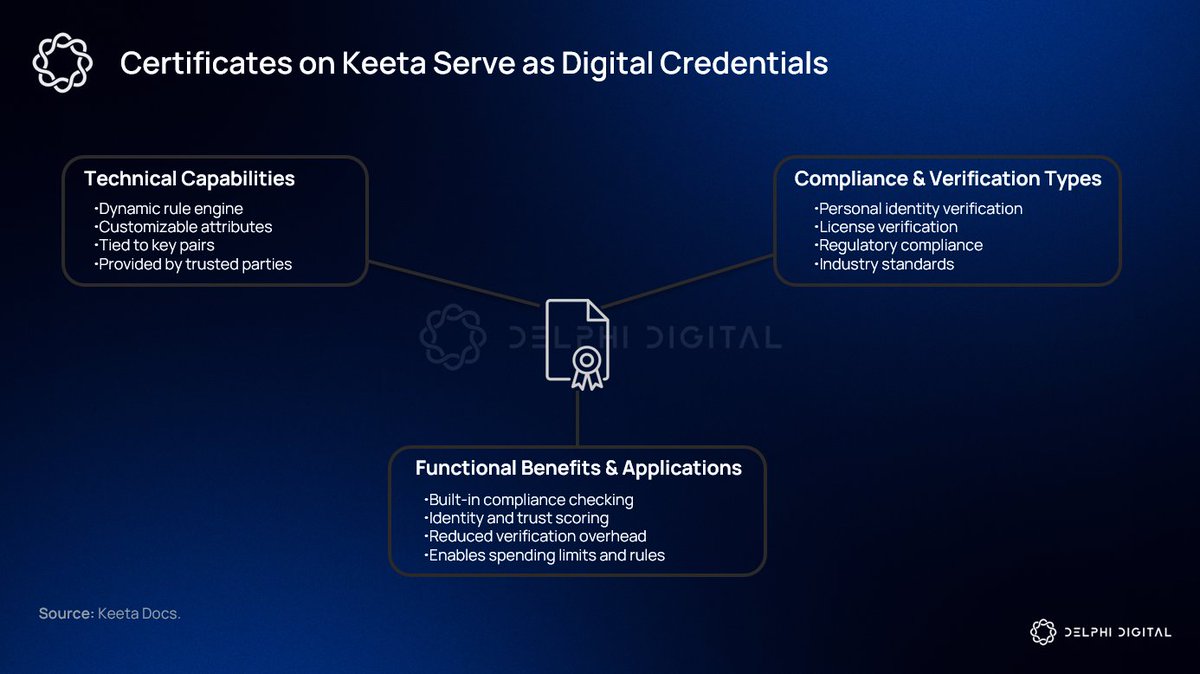

@KeetaNetwork is building for this gap. Their approach uses onchain identity certificates via the X.509 standard, the same cryptographic framework used across internet protocols). Wallets get tied to verifiable identity attestations without exposing the underlying personal data.

With selective disclosure, users can prove specific attributes (KYC status, jurisdictional permissions, business licenses) to counterparties without revealing everything else. Compliance is enforced at the protocol level while pseudonymity is preserved on the public ledger.

Keeta has also built a permission system around asset issuance that includes jurisdictional restrictions, KYC-gated transfers, and role-based permissions for custodians. These features are standard in traditional finance but still missing from most crypto infrastructure.

Keeta is building the compliant rails institutions need before they can move onchain.

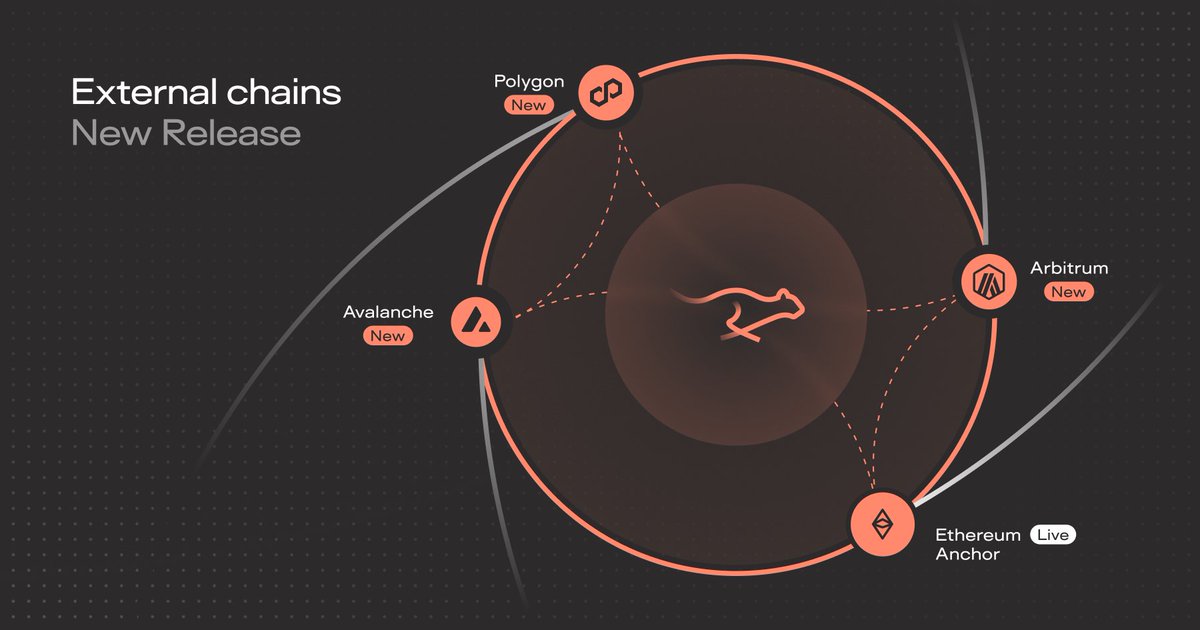

Keeta Network continues to grow.

USDC on Keeta Network can now be sent to and from Avalanche, Polygon, and Arbitrum.

USDT and PYUSD on Ethereum can now be sent to and from USDC on Keeta Network.

More routes. More liquidity. More coming soon.

$KTA

![0xchainink's tweet photo. $KTA : Review

A member of the Abu Dhabi Royal Family just created a joint venture with a blockchain project to tokenize tens of billions of dollars of Gulf commodities and modernize cross-border payments across the Middle East, Africa, and Asia.

Meet Keeta Network - a Layer-1 blockchain designed to unify global payment networks through built-in KYC/AML compliance, cross-chain settlement, and 11.2M TPS verified by Google's Spanner team.

Founded by ex-BrainBlocks and Nano veterans. Backed by former Google CEO Eric Schmidt. And as of today, partnered with ASK Group, a UAE-based investment group led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan, to build a public exchange for tokenized Gulf commodities targeting 2027.

Let's explore what just happened and why it matters. 👇

🔵 The ASK Group Partnership

This is the kind of announcement that redefines a project's trajectory overnight.

Keeta and ASK Group, led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan, have created a joint venture aiming to tokenize tens of billions of dollars of commodities and modernize cross-border payments in the GCC region and beyond.

Key details:

➛ The joint venture is working toward establishing a Keeta-powered public exchange for tokenized Gulf commodities, with an initial target of 2027, subject to regulatory approvals and the establishment of custody and operational infrastructure.

➛ Every barrel of oil, ounce of gold, and kilogram of silver will be represented as a digital token on the Keeta network, bringing 24/7 settlement, instant fractional trading, global compliance, and verifiable proof-of-reserves to one of the largest untapped markets on earth.

➛ Global commodity markets move several trillion dollars annually. The GCC's share of the world's proven oil reserves alone represents an asset base whose tokenization would constitute one of the largest migrations of real-world value onto blockchain infrastructure in history.

➛ A retail investor in Tokyo, an institutional fund in London, or a family office in Singapore will have the same direct access to a barrel of Gulf crude or an ounce of UAE-held gold as the largest commodity trading houses have historically enjoyed.

➛ The UAE is one of the highest-volume remittance origination markets on earth, with the UAE-India corridor alone moving approximately $20 billion annually. Keeta's infrastructure will modernize cross-border payments to South Asia, Africa, Southeast Asia, and beyond.

➛ ASK Group holds exclusive rights to facilitate and execute Keeta's presence across the UAE, MEA, and India.

➛ This marks the beginning of a long-term relationship. Additional asset classes and use cases in the GCC region and beyond are planned.

⚪ Why This Matters

Let's put this in context. Keeta was already positioned as a compliance-first L1 targeting the TradFi-DeFi bridge. Eric Schmidt backing. 11.2M TPS verified. Bank acquisition pending. KUSD stablecoin incoming.

Now add: a joint venture with an Abu Dhabi Royal Family-led investment group to tokenize the Gulf's commodity reserves, one of the most valuable asset bases on earth. Oil. Gold. Silver. On a blockchain that does 11.2 million transactions per second with 400ms settlement and built-in KYC/AML.

At $0.20 per token and a $113M market cap, KTA is valued at less than the annual remittance volume of a single UAE-India corridor ($20B). The commodity markets this joint venture is targeting move trillions annually. If even a fraction of 1% of Gulf commodity tokenization flows through Keeta, the current market cap looks microscopic.

⚪ Keeta at a Glance

Keeta is a Layer-1 blockchain designed to unify global payment networks. Built on a DAG-based architecture with dPoS consensus, it enables cross-chain settlement, RWA tokenization, and built-in KYC/AML compliance.

$KTA trades at $0.20 as of June 9, 2026, up 35% in the last 24 hours on the ASK Group announcement. Market cap: $113M. Circulating supply: ~513M out of 1B max.

➛ 11.2M TPS verified by Google's Spanner engineering team and Chainspect ➛ 400ms settlement times ➛ Built-in KYC/AML compliance at the protocol level ➛ DAG-based architecture with dPoS consensus ➛ Native RWA tokenization and digital identity tools ➛ Cross-chain settlement layer ➛ Bank acquisition pending regulatory approval ➛ Upcoming: KUSD stablecoin, Keeta Pay, Keeta Card, native DEX ➛ Backed by former Google CEO Eric Schmidt ($17M at $75M valuation)

🔵 Meet the Keeta Team

Keeta is led by crypto payments veterans from BrainBlocks and Nano, backed by former Google CEO Eric Schmidt, and now partnered with an Abu Dhabi Royal Family-led investment group for sovereign-scale commodity tokenization.

▶️ Core Members:

➛ Ty Schenk [ @schenkty ] - Founder & CEO | Software engineer, ex-BrainBlocks co-founder, ex-Turo, ex-Steel Perlot. Forbes 30 Under 30. Designed Keeta to make cross-border payments as simple as Venmo. Now leading a joint venture with Abu Dhabi royalty to tokenize Gulf commodities.

➛ Roy Keene - CTO | 16+ years in systems engineering. Former lead developer at Nano Foundation, former Senior Cloud Architect at AWS. Brings deep blockchain architecture and cloud infrastructure expertise. Built the 11.2M TPS engine.

➛ David Campos - Head of Operations

➛ Josh Kleiman - General Counsel

🔵 Ratings

➛ Use Case: ★★★★★ (5/5) - The ASK Group partnership elevates Keeta from "promising compliance-first L1" to "the blockchain that an Abu Dhabi Royal Family investment group chose to tokenize Gulf commodities." Oil, gold, silver on-chain with 24/7 settlement, fractional trading, and proof-of-reserves. Cross-border payments modernization for the $20B UAE-India corridor. Combined with 11.2M TPS, 400ms finality, built-in KYC/AML, Eric Schmidt backing, and the pending bank acquisition, Keeta now has the most significant real-world asset pipeline of any L1 outside of Ondo and Stellar. Upgrading from 4.5 to 5.

➛ Tokenomics: ★★★ (3/5) - Unchanged. 1B supply, 50% community allocation is decent, but 40% insider allocation (team + investors) and no burn mechanism remain concerns. The ASK Group partnership should drive significant future demand for KTA as the settlement token for tokenized commodities, but that's 2027+ timeline.

➛ Audits: ★★★★ (4/5) - CertiK audited. Stress test verified by Chainspect and Google Spanner team. Strong security positioning for an L1 targeting institutional finance and now sovereign wealth-adjacent commodity tokenization.

➛ Community: ★★★★ (4/5) - 235M testnet wallets, 42M active wallets, 13+ exchange listings, growing social presence. The ASK Group announcement drove 35% in 24 hours, showing the community responds

to real catalysts. Active Twitter Spaces and engagement from the founder.

🔵 Conclusion

One hour ago, Keeta Network went from "compliance-first L1 backed by Eric Schmidt" to "the blockchain that an Abu Dhabi Royal Family-led investment group is using to tokenize Gulf commodity reserves." That's not a partnership announcement. That's a sovereign-adjacent endorsement of Keeta as the infrastructure layer for one of the largest migrations of real-world value onto blockchain in history.

The numbers speak: trillions in annual commodity flows. $20 billion in the UAE-India remittance corridor alone. Exclusive rights across UAE, MEA, and India. Public commodity exchange targeting 2027. Oil, gold, silver as on-chain tokens with 24/7 settlement, fractional access, and proof-of-reserves. All running on a chain that does 11.2M TPS with 400ms finality and built-in compliance.

At $0.20 and $113M market cap, 35% up today, KTA is either the most undervalued infrastructure play in the RWA space or the market hasn't had time to process what just happened. Given that this announcement is one hour old, the answer is probably the latter.

The question isn't whether tokenized Gulf commodities are a big deal.

They're potentially the biggest RWA opportunity in the world. The question is whether Keeta and ASK Group can execute on the 2027 timeline.

If they do, $113M market cap for the blockchain powering trillions in commodity tokenization will look like the buy of the cycle.](https://pbs.twimg.com/media/HKX9pEtbEAAEx_P.jpg)