@shamikiscooking@DFinMirror No lower circuit on Monday. Weak results were already anticipated due to low IPO activity during the last quarter. So the results are not shocking. Already priced in.

Gem Aromatics #HarResultKuchKehtaHai#GOOD

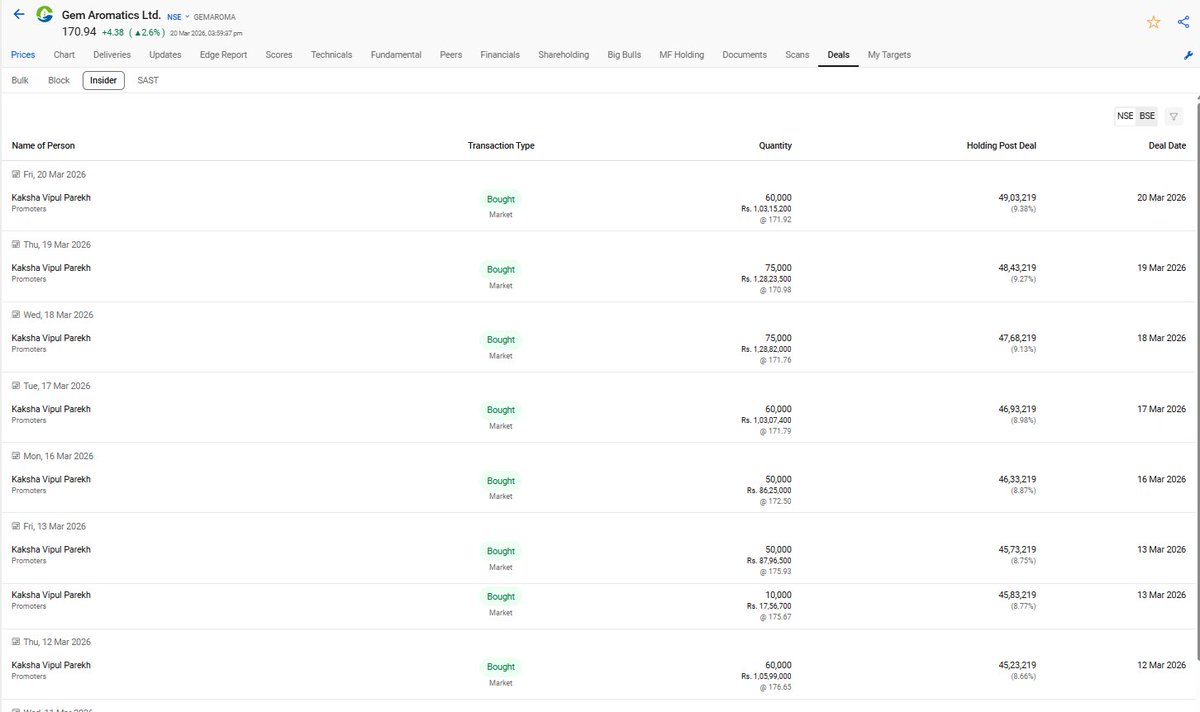

The headline 96% drop in profit hides a significant sequential turnaround that the market appears to have missed. After recording a ₹5 Cr loss in the previous quarter, the company returned to a ₹1 Cr profit as the new Dahej facility began its first full quarter of operations. This facility triples the group capacity to over 17,000 tons and marks the beginning of a structural shift away from volatile mint trading toward high-value cooling agents and phenol derivatives. Operating margins jumped from 8.9% to 14.2% in just three months, a sharp expansion that confirms the new product mix is significantly more profitable than the legacy business.

The balance sheet has also been cleaned up, with total borrowings falling from ₹225 Cr to ₹149 Cr following the full utilization of IPO proceeds for debt repayment. This reduction in leverage is critical as it provides the working capital headroom needed to fund the inventory build-up required for the Dahej ramp-up. Promoter confidence is perhaps the most compelling signal in this result. The Managing Director and CFO purchased over ₹10 Cr worth of shares from the open market in March 2026, just as the quarter was concluding. This represents a massive vote of confidence in the ₹160-200 price range, suggesting that management views the current valuation as a significant discount to the replacement value of the new assets.

The plant is currently at 18% utilization, with a clear path to the 45% cash break-even mark by late FY2027. Looking ahead, the next major catalyst is the commencement of phenol derivative trials in Q1 FY2027. These products, including Anisole and MEHQ, are designed to target global flavor and fragrance houses that are actively seeking alternatives to Chinese suppliers under the 'US plus one' strategy. If the company successfully executes its planned 3x asset turn on the new facility, the ambitious ₹1,100 Cr revenue goal for FY2028 remains highly achievable. The return to positive earnings this quarter likely marks the end of the gestation-related losses.

Full breakdown → https://t.co/bhs6kdMxUs

Public NSE/BSE filings · Not Investment Advice

#GEMAROMA #Q4FY26 #StockMarket #Earnings

Personal update: I've joined Anthropic. I think the next few years at the frontier of LLMs will be especially formative. I am very excited to join the team here and get back to R&D. I remain deeply passionate about education and plan to resume my work on it in time.

Asked someone from the industry whether foreign investors are still interested in allocating to India. The TLDR:

Interest has pretty much died out. India is seen as geopolitically exposed, especially to an oil shock. There are no real AI plays. Valuations are rich. And the rupee situation doesn't help.

On top of that, investors who were sitting on gains have taken money off the table and are now looking at markets like Japan, Taiwan, Korea, Europe etc instead.

He also pointed out that our LTCG/STCG structure and the increase in STT have made India less attractive compared to other markets that are seeing inflows.

If we need to attract FPIs back, and we do, fixing this feels like pretty low-hanging fruit.

With sustained FII outflows from Indian markets, it may be prudent for the government to revisit capital gains taxes (STCG, LTCG) and consider removing STT to improve global competitiveness @nsitharaman@PMOIndia

DAM Capital Advisors at ₹126 looks interesting.

• ~40–50% ROE

• Debt-free

• Investment bank leveraged to India’s IPO boom

• High operating leverage �� profits can jump in strong capital market cycles

Small market cap + cyclical earnings = potential rerating candidate.

@amazonIN Very poor experience. Ordered a Hitachi 1.5 Ton AC on 23 Feb, delivery promised 24 Feb. As of 28 Feb, no delivery and the order has vanished from order history. Payment already done. Need immediate clarification. #AmazonHelp

📺 Amagi turns up the volume on profits in Q3 FY26 🚀

The cloud-based media SaaS platform reported a 292% YoY jump in net profit for the quarter ended December 31, 2025. 👇

💰 Net Profit: ₹30.94 crore (vs ₹7.89 crore)

📈 Revenue: ₹403.81 crore (+22% YoY)

💼 Employee costs rose to ₹204.13 crore

For the first 9 months of FY26:

📌 Revenue at ₹1,108.64 crore

📌 Net profit of ₹37.41 crore (vs ₹58.11 crore loss last year)

MD & CEO Baskar Subramanian said scaling revenue translated into strong operating leverage and profitability expansion.

More details ⬇️

https://t.co/3rrD9milfr

#media #brand #marketing