momentum has positive skew.

most trades are small paper cuts, you enter, it fizzles, you get stopped, small loss. that happens constantly.

then occasionally one trade catches a real trend and pays for all of them several times over.

the cleanest analogy is venture capital. the VC makes 20 bets, 15 go nowhere, 1 returns 100x and makes the fund.

the expectancy doesn't live in your win rate. it lives entirely in the size of the rare winner.

this is why the strategy feels bad most of the time. small losses drip in while you wait. it only feels good occasionally. people quit right before the move that would've made them whole.

the discipline: take every valid signal because you don't know which one is The One. cut losers fast so a paper cut never becomes a wound. and let winners run far past where it feels comfortable, because the whole edge is in not chopping the tail short.

Most traders think slippage is the gap between their stop price and their fill. It's not. Slippage is the cost to cross the spread — buyer to seller.

@multistratmark goes through it.

Commodity Trend Following is a strategy backed by over 140 years of data. During the worst 8 years for the traditional 60/40 portfolio, this strategy managed to generate profits.

So, what does it entail?

1. Long commodities when prices increase.

2. Short commodities when prices decrease.

Commodities include assets like oil, copper, corn, and gas. A key aspect of this strategy is that it focuses solely on price movements, rather than the reasons behind those movements. It takes long positions when commodities trend upwards for several months and shorts when they trend downwards. This approach is effective because commodities tend to trend more strongly than stocks.

Unlike most investors who adopt a long-only stance, and many commodity ETFs that also focus solely on long positions, commodity trend following can short. This means:

- When oil prices crash, the strategy shorts oil.

- When gold prices reverse, it can also short oil.

This strategy is about waiting for significant price movements rather than merely betting on upward trends. It represents a divergent bet rather than a convergent one.

Over 145 years, this strategy has demonstrated positive returns through:

1. Two World Wars

2. The Great Depression

3. The stagflation of the 1970s

4. The 2008 financial crisis

5. The sell-off in 2022

What are your thoughts on this strategy? Are you implementing a similar approach to help your portfolio zig when the market zags?

New 0DTE traders think a stop-loss caps their risk at a clean number. It doesn't. The stop has its own volatility — slippage varies, and on a fast move a $5 stop fills at $7 or $15 or $25. You're trading spread-width certainty for variable cost. Understand that before you size up. With @multistratmark

A 7% dividend is not a 7% return.

In a high bracket, taxed as ordinary income, you might keep 4%.

Structured as return of capital inside an ETF wrapper? Most of the tax bill defers for years — and what's left often lands at long-term rates.

Same asset. Same cash flow. Very different after-tax outcome.

Two mechanics most investors ignore:

1. ETF wrappers. In-kind redemptions let funds rebalance appreciated positions without triggering gains. Your tax bill pauses until YOU choose to sell.

2. Return-of-capital distributions. Some option-income ETFs distribute mostly ROC — monthly cash flow, basis step-down instead of a current tax bill, eventual LTCG treatment.

Two tools anyone can use:

→ Box-spread ETFs: roughly T-bill yield with §1256 treatment (60/40) and deferral until sale — versus a HYSA taxed at ordinary rates every year.

→ 130/30 long/short direct indexing: ~100% net index exposure while continuously harvesting realized losses to offset gains elsewhere.

Every taxable investment has to answer two questions: does it make money pre-tax, and does it survive post-tax?

Most investors stop at the first.

At MBH Capital Management, we build our 0DTE and multi-strategy books around after-tax outcomes — because after-tax returns are the only returns that matter.

@t0mbfx Something no one wants to talk about is how long it actually takes to become profitable, then once you start a fund then you start right back over.

@Madhur2379 This is definitely a tough market for O DTE, extremely hard for people who are trying to learn how to trade in zero day for the first time. Most of the strategies that were effective last year are no longer effective.

0 DTE isn't dead; I simply outgrew one engine.

Fund I is a 3(c)(1) and is capped at 100 LPs by regulation, not by edge. This led to the creation of Fund II, which maintains the same 0DTE under the hood but with a smaller weight. It is layered with:

- Tax-aware equity beta

- Managed futures and global macro

- Relative value and equity market neutral strategies

- External specialists for niches like convertible arbitrage

Each pod operates independently, with one risk manager allocating resources across them as market regimes shift.

If your highest ROI comes from trading, continue on that path. If your focus is on your business, career, or craft, remember that outsourcing risk management is not a sign of weakness; it reflects resourcefulness. Ultimately, people either have more resources or more resourcefulness.

On June 2, 1925, Wally Pipp had a headache.

He sat out one game. Lou Gehrig took his spot and didn't give it back for 2,130 straight games.

"Getting Pipp'd" entered the lexicon: replaced by someone better while you weren't looking.

Markets work the exact same way.

The strategy that printed last year? Someone is reverse-engineering it right now.

The edge you're sitting on? Half-life is shorter than you think.

The day you stop measuring your own performance is the day the market starts measuring it for you. Usually expensively.

Stay paranoid. Stay sharp. Show up.

The bench is full of people who'd kill for your seat.

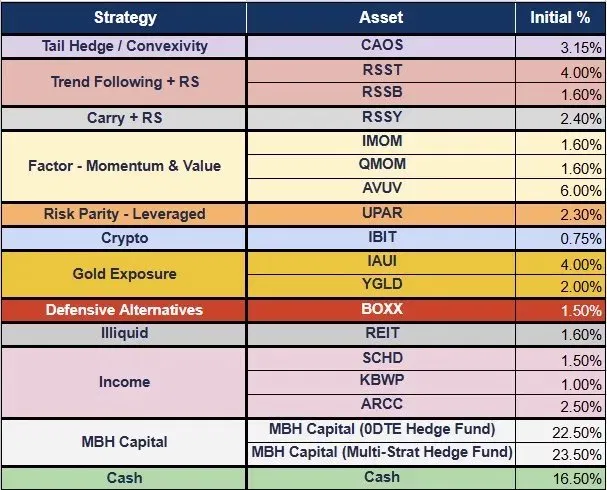

MBH Capital Management returned +2.12% net in April.

MBH Capital is built for income as the outcome — providing investors with consistent returns that seek zero beta and pure alpha relative to traditional equity and fixed income markets. Our fully systematic, algorithmic approach is designed to offer a liquid alternative within a diversified portfolio.

➡️ Join our Distribution List: https://t.co/EbkZys6ysl

➡️View Our Daily Returns Since Inception Here https://t.co/ZY2pJyQM5m

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Strategy involves substantial risk including potential loss of principal. Returns shown are net of all fees and expenses; correlation calculated over [1/2023-5/1/2026].

Offered exclusively to verified accredited investors under Rule 506(c) of Regulation D.

"Fair value and change are therefore two sides of the same coin; the more ways in which a security can lose value from a future market move, the less it should rationally be worth today, and hence the mantra: more risk, more return."

- Emanuel Derman, My Life as a Quant.

![multistratmark's tweet photo. MBH Capital Management returned +2.12% net in April.

MBH Capital is built for income as the outcome — providing investors with consistent returns that seek zero beta and pure alpha relative to traditional equity and fixed income markets. Our fully systematic, algorithmic approach is designed to offer a liquid alternative within a diversified portfolio.

➡️ Join our Distribution List: https://t.co/EbkZys6ysl

➡️View Our Daily Returns Since Inception Here https://t.co/ZY2pJyQM5m

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Strategy involves substantial risk including potential loss of principal. Returns shown are net of all fees and expenses; correlation calculated over [1/2023-5/1/2026].

Offered exclusively to verified accredited investors under Rule 506(c) of Regulation D.](https://pbs.twimg.com/media/HHlRL3DXoAItuG-.jpg)