My stock market checklist

learn to follow this checklist whenever you buy or sell a stock

1. Business model/ AAA management/TCE

2. Annual /Quarterly Sales growth

3. Annual/ Quarterly Bottom line growth (PAT growth/ operating Profit)

4. Margin expansion/ Operating leverage

5. Management guidance/Tone of concall

6. Capex and expansion

7. Valuations - PE Rerating possible?

8. Sector tailwinds/TAM

9. Macros

10. New product or Product mix change - leading to increased margins but no sacrifice in growth

11. Strong Order book

12. Sector-specific metrics (e.g., retail - SSG, hospital - ARPOB, hotel - REVPAR)

13. Operating Cash flows & EV/EBIDTA at least 60%)

14 Focus of Govt policies/Budget direction

15. Market direction

16, Supply and Demand/ Liquidity

17 special situation I. e Demerger/Acquisition/new geography/ new product/ new management/ Rush among institutional investor for new IPO/ entry of PE investor

18. is secular sector or cyclical or shallow cyclical?

19. Avoid when sector is at peak level/Peak Margin/Avoid when sector specific IPO is coming at peak

#SenoresPharma#SENORES

A pharma company with 42% EPS CAGR trades at just 17.9× FY28E. Is the market pricing a two-year earnings spike about to peak — or completely missing what this business actually is? Here is the full picture on Senores Pharmaceuticals. 🧵

What it does

Most generic pharma companies make a drug and sell it once. Senores operates two distinct businesses out of the same factory — and that distinction is why the margins look nothing like a typical generics company.

Business 1 — Own ANDA portfolio. Senores spends 2–3 years earning USFDA approval for complex drugs — controlled substances, oncology injectables, high-barrier specialty molecules. It owns the approved dossier. It manufactures every unit at its own plants in India and Atlanta. But instead of building a US sales force, it licenses distribution rights to large partners like Dr. Reddy's. Dr. Reddy's pays Senores three times: an upfront licensing fee for the right to sell, a per-batch supply price for every unit manufactured, and a back-end profit share from US sales. Dr. Reddy's earns only from selling. Senores earns from all three — with none of the sales overhead.

Business 2 — CMO/CDMO manufacturing. Here a third party already owns the drug approval and simply pays Senores to manufacture it at their facility. Senores earns only the manufacturing margin — one revenue layer, not three. Lower margin than the ANDA business but steady, volume-driven, and it sweats the same factory assets that the ANDA business already paid for.

The combination drives 29–33% EBITDA margins — high-margin ANDA licensing stacked on top of a contract manufacturing base that keeps the plants fully utilised between own-product batches.

The moat

Not a patent. It is time, compliance, and geography — three things money alone cannot shortcut.

Each USFDA drug approval takes 2–3 years and is tied to a specific facility. Senores has 51 approved. A competitor starts from zero.

The DEA licence in Atlanta is rarer still. Manufacturing controlled substances on US soil requires high-security infrastructure and compliance audits most Indian pharma companies have never attempted. It opens direct US government supply contracts that are simply unavailable to everyone else.

For select approvals, the USFDA grants a 180-day exclusivity window — Senores is the only generic supplier before competitors can legally enter. 28 more filings in progress means this is a repeating cycle, not a one-time event.

Once Dr. Reddy's integrates a Senores-supplied product, switching requires finding another USFDA-cleared manufacturer for the same molecule, passing fresh facility audits, and running full-scale batches — all while risking US pharmacy stock-outs. Nobody does that over a price difference.

The FY28 numbers

FY26A: Sales ₹679 Cr · EBITDA ₹199 Cr (29.4%) · PAT ₹121 Cr · EPS ₹30.85 · ROIC 23.5%

FY28E: Sales ₹1,235 Cr · EBITDA ₹414 Cr (33.5%) · PAT ₹287 Cr · EPS ₹62.08 · ROIC 28.1%

Two structural drivers power this — operating leverage on a fully staffed cost base (every incremental ₹100 revenue drops ₹34 to EBITDA) and a 51-approval launch calendar already on paper. One transient item: IPO proceeds permanently wiped ₹23 Cr of finance costs — that step-change is now in the base and does not repeat. FY27 and FY28 need no new catalyst. At 17.9× FY28E the market is pricing a 42% EPS CAGR as if it flatlines the moment FY28 closes.

What could re-rate this significantly — and why

① 28 new filings confirm the launch engine keeps running.

The market's single biggest concern is that FY26–28 was a one-time wave of exclusivity windows rather than a sustainable machine. Confirmation that a fresh wave is incoming transforms the narrative from cyclical earnings spike to structural compounder with a rolling launch calendar.

② US government mandates onshore controlled-substance supply.

Government institutional contracts are annuity revenue — fixed volumes, predictable pricing, multi-year tenure, no sales effort required. This type of revenue is structurally different from product-by-product licensing deals and commands a higher earnings quality premium from the market

③ CDMO segment gets valued separately.

The contract manufacturing business is guided at ₹210–250 Cr in FY27 alone — already large enough to stand on its own.

- Because their revenue is contracted, visibility is high, and capital requirements are low.

④ Emerging markets inflects commercially.

Senores has 285 registered products and 636 under registration across Latin America, Africa, and Asia. - Currently sub-scale in revenue contribution.

Diversifying from US concentrated regulatory play.

The closing thought

Is the market pricing a two-year earnings spike that peaks at FY28 — or has it simply not looked closely enough at what a 28-molecule filing pipeline, a DEA licence nobody else in Indian pharma holds, and a CDMO base growing on the same assets can quietly compound into over the next five years? 🤔

[Not investment advice, DYOR]

Jefferies On Industrials

Defence and power standout on capex visibility

Believe Power equipment and defence remain the best way to play the sector

Top picks- Siemens Energy, Hitachi, HAL, BEL, KEI, and L&T

FY26 order flow rose 9% YoY for the coverage universe, led by L&T and BEL.

"There are certain years in company's journey where performance improves, and there are certain years where foundation for next decade is built.

For Shilpa Medicare, FY26 has been one such year."

— Keshav Bhutada, CEO

Q4 FY26 , Concall .

Shilpa Medicare Q4 FY26: Building the foundation for the next decade 👉

Shilpa is no longer a single vertical.

It is building a pharma platform spanning:

✅ APIs

✅ Complex Formulations

✅ CDMO

✅ Biologics

✅ ADCs

✅ Recombinant Human Albumin

Q4 Concall updates 🧵

#VINYAS

Vinyas Innovative Technologies: Quick Thesis 🧵

Revenue engine: Mysuru plant capacity doubling to ₹1,200 Cr ceiling (live Apr 2027) · Israeli defense JV ramping Box-Build avionics & tactical comms under Make in India · US subsidiary chasing direct export contracts in Europe & North America · ₹1,309 Cr order backlog provides 18–24 month runway with 30–35% CAGR guidance

Margin story: EBITDA expanding 12.5% → 17% as defense Box-Build mix (30–35% gross margins) displaces standard board stuffing (7–10%). Employee cost falling from 9% → 8% of sales. COGS declining as component-heavy assembly gives way to full system integration. Interest cover strengthening 4.4x → 7.9x as equity pool cuts debt reliance.

Moat: The only Indian EMS player with Nadcap AC7120 accreditation — the certification that opens doors to global aerospace and defense OEMs. Entry barriers are 18–36 month audit cycles that volume-scale competitors cannot shortcut. Demand lock-in is strong; switching triggers multi-year re-certification. IP is weak (OEM-owned) but the process know-how and cleanroom layout is the real edge. CAP 5 years, stable to widening as Box-Build JV deepens client integration.

Management: Founder-operator Narendra Narayanan with 20+ years in HMLV defense EMS — not a financial aggregator. Delivered 25–30% revenue growth as guided, every year post-listing. Promoter stake diluted to 29.4% deliberately to fund the ₹150 Cr expansion — zero pledging. Board is balanced with independent oversight on all key committees.

Numbers: Sales ₹518 Cr (FY26A) → ₹685 Cr (FY27E) → ₹900 Cr (FY28E) · PAT ₹31 Cr → ₹56 Cr → ₹88 Cr · EPS ₹24.51 → ₹44.07 → ₹70.21 · CFO turns positive FY27

Not SEBI registered. Not investment advice. DYOR.

India just dropped a defence BOMBSHELL.

₹17,000 CRORE in military drone orders.

Only INDIAN companies qualify.

Deliveries in 18 months.

This isn't just procurement.

This is the birth of an Indian drone superpower.

🧵 Deep dive. Everything you need to know.

ADVAIT Energy, Concall updates Q4FY26

1/ Record Order Bk 👉Multi-Year Visibility

FY26 Order bk 1,304 Cr, up 159% YoY, with 64% from Power Transmission and 36% from New Renewable Energy.

Mgmt expects FY27 growth guidance of 40%+ to be conservative.🔥

Sacheerome Q4FY26 Concall updates

New Capacity Addition

The company planned to scale capacity from 7,60,000 kg to 27,60,000 kg - almost a 4x jump, was originally expected to be commissioned in March 2026.

However, there is a delay and the new capacity is now expected to be commissioned in August 2026.

FY26 revenue was 150 cr.

Management guided for

👉🏼₹200 Cr sales in FY27,

👉🏼₹250 Cr in FY28, and

👉🏼₹300 Cr in FY29, which they themselves acknowledged multiple times is quite conservative.

Since new capacity comes online only in August 2026, H1FY27 (Apr 26- Sep 26) results may not be particularly strong, with meaningful growth expected to reflect from H2FY27 onwards.

Considering the current P/E of 24, management's strong track record, and good institutional investors in the company, I plan to hold.

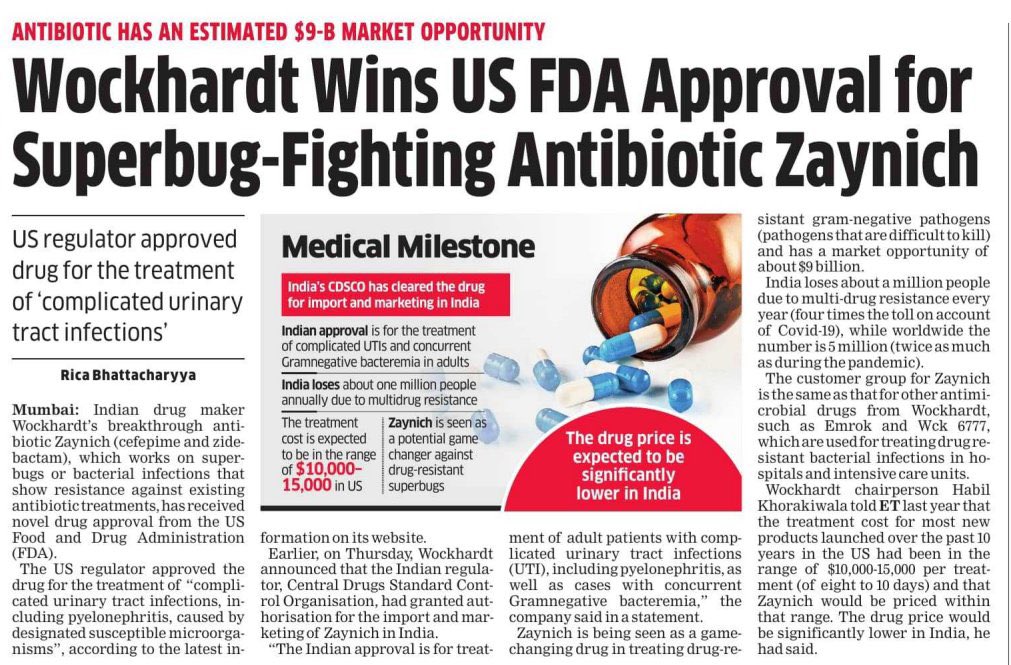

FEW POINTS FOR WOCKHARDT :

Game‑Changing Development: Zaynich Antibiotic :

Breakthrough molecule: Zaynich (a.k.a. WCK‑5222) targets drug‑resistant infections with a susceptibility breakpoint of 64 mg/L—the highest recorded in the last century .

Massive market potential: It addresses 10 gram‑negative pathogens, tapping into a ~₹2.11 lakh crore global AMR (antimicrobial resistance) opportunity. Wockhardt aims for up to 75% market share.

U.S. FDA NDA filing expected in Q2 FY25, with marketing anticipated by 2026–27. Indian approval is likely by early 2026 .

With no comparable competing drugs projected for the next 15 years, Zaynich offers exceptional competitive insulation

![ramesh_vd's tweet photo. #SenoresPharma #SENORES

A pharma company with 42% EPS CAGR trades at just 17.9× FY28E. Is the market pricing a two-year earnings spike about to peak — or completely missing what this business actually is? Here is the full picture on Senores Pharmaceuticals. 🧵

What it does

Most generic pharma companies make a drug and sell it once. Senores operates two distinct businesses out of the same factory — and that distinction is why the margins look nothing like a typical generics company.

Business 1 — Own ANDA portfolio. Senores spends 2–3 years earning USFDA approval for complex drugs — controlled substances, oncology injectables, high-barrier specialty molecules. It owns the approved dossier. It manufactures every unit at its own plants in India and Atlanta. But instead of building a US sales force, it licenses distribution rights to large partners like Dr. Reddy's. Dr. Reddy's pays Senores three times: an upfront licensing fee for the right to sell, a per-batch supply price for every unit manufactured, and a back-end profit share from US sales. Dr. Reddy's earns only from selling. Senores earns from all three — with none of the sales overhead.

Business 2 — CMO/CDMO manufacturing. Here a third party already owns the drug approval and simply pays Senores to manufacture it at their facility. Senores earns only the manufacturing margin — one revenue layer, not three. Lower margin than the ANDA business but steady, volume-driven, and it sweats the same factory assets that the ANDA business already paid for.

The combination drives 29–33% EBITDA margins — high-margin ANDA licensing stacked on top of a contract manufacturing base that keeps the plants fully utilised between own-product batches.

The moat

Not a patent. It is time, compliance, and geography — three things money alone cannot shortcut.

Each USFDA drug approval takes 2–3 years and is tied to a specific facility. Senores has 51 approved. A competitor starts from zero.

The DEA licence in Atlanta is rarer still. Manufacturing controlled substances on US soil requires high-security infrastructure and compliance audits most Indian pharma companies have never attempted. It opens direct US government supply contracts that are simply unavailable to everyone else.

For select approvals, the USFDA grants a 180-day exclusivity window — Senores is the only generic supplier before competitors can legally enter. 28 more filings in progress means this is a repeating cycle, not a one-time event.

Once Dr. Reddy's integrates a Senores-supplied product, switching requires finding another USFDA-cleared manufacturer for the same molecule, passing fresh facility audits, and running full-scale batches — all while risking US pharmacy stock-outs. Nobody does that over a price difference.

The FY28 numbers

FY26A: Sales ₹679 Cr · EBITDA ₹199 Cr (29.4%) · PAT ₹121 Cr · EPS ₹30.85 · ROIC 23.5%

FY28E: Sales ₹1,235 Cr · EBITDA ₹414 Cr (33.5%) · PAT ₹287 Cr · EPS ₹62.08 · ROIC 28.1%

Two structural drivers power this — operating leverage on a fully staffed cost base (every incremental ₹100 revenue drops ₹34 to EBITDA) and a 51-approval launch calendar already on paper. One transient item: IPO proceeds permanently wiped ₹23 Cr of finance costs — that step-change is now in the base and does not repeat. FY27 and FY28 need no new catalyst. At 17.9× FY28E the market is pricing a 42% EPS CAGR as if it flatlines the moment FY28 closes.

What could re-rate this significantly — and why

① 28 new filings confirm the launch engine keeps running.

The market's single biggest concern is that FY26–28 was a one-time wave of exclusivity windows rather than a sustainable machine. Confirmation that a fresh wave is incoming transforms the narrative from cyclical earnings spike to structural compounder with a rolling launch calendar.

② US government mandates onshore controlled-substance supply.

Government institutional contracts are annuity revenue — fixed volumes, predictable pricing, multi-year tenure, no sales effort required. This type of revenue is structurally different from product-by-product licensing deals and commands a higher earnings quality premium from the market

③ CDMO segment gets valued separately.

The contract manufacturing business is guided at ₹210–250 Cr in FY27 alone — already large enough to stand on its own.

- Because their revenue is contracted, visibility is high, and capital requirements are low.

④ Emerging markets inflects commercially.

Senores has 285 registered products and 636 under registration across Latin America, Africa, and Asia. - Currently sub-scale in revenue contribution.

Diversifying from US concentrated regulatory play.

The closing thought

Is the market pricing a two-year earnings spike that peaks at FY28 — or has it simply not looked closely enough at what a 28-molecule filing pipeline, a DEA licence nobody else in Indian pharma holds, and a CDMO base growing on the same assets can quietly compound into over the next five years? 🤔

[Not investment advice, DYOR]](https://pbs.twimg.com/media/HKb3Q1ka8AAfIHc.png)