Most traders don't fail for lack of a signal. They fail

because their expectations were never realistic to begin with.

A durable systematic edge in crypto is unglamorous: a Sharpe ratio near 1, a drawdown you can actually sit through, and annual returns that would sound boring at dinner. Good years exist; they are paid for by flat years and losing stretches.

Consider the arithmetic. A strong 20% year returns $400 on a $2,000 account and $4,000 on $20,000. Only near $200,000 does it begin to resemble an income. Leverage does not close that gap; it converts a modest edge into a fast liquidation.

The priorities that actually determine outcomes, in order, are survival, costs, and returns. A single ruin event resets compounding to zero, and zero compounds to zero.

Want to learn more? Read the full breakdown here:

https://t.co/PlYofQGFQD

The hardest part of optimization is knowing when to stop.

There is a point in every optimization where the backtest keeps improving and the strategy keeps getting worse.

Past that point, you are no longer finding an edge.

You are sanding the strategy down to fit one exact shape of the past, a shape the future has no reason to repeat.

Optimization should make a strategy more durable.

Done without discipline, it does the opposite. It makes the strategy more confident and more fragile at the same time.

This is the part we are building Edgecraft around: you run the backtest, then validate it with k-fold across the history plus much, much more; and have honest train and test splits that keep the out-of-sample genuinely out of sample. So you can see the moment your tuning stopped adding edge and started adding fragility.

Don't be the trader that sees this and thinks he will print money:

SOL/BTC has been one of the cleaner regime reads this cycle, but that cloud is still stacked heavily against it on the daily. These sharp spikes from compressed ranges after long downtrends are interesting because if the cloud starts thinning ahead, the transition back can move fast. Is this still a watch for you, or are you already leaning into the rotation?

Most people optimize for one number.

That one number is usually what breaks them.

Optimize for return, and drawdown can quietly grow until it would have ended you.

Optimize for win rate, and you breed strategies that win often and lose huge.

Optimize for Sharpe, and you can end up with a beautiful ratio built on nine trades.

Every metric, maximized alone, sacrifices the others.

A real objective is not a number.

It is a balance:

enough return, contained drawdown, enough trades to trust the result, and stability across assets and conditions.

Who can tell me what the issues are with this strategy? Be careful to not get tricked by that sexy-looking profit number.

A single “best” parameter is usually a warning, not a win.

When you optimize, you get the best value.

Best lookback. Best stop. Best threshold.

But the question that matters is not how good that point is.

It is what happens right next to it.

If the strategy is excellent at one exact value and falls apart one step in either direction, you did not find an edge.

You found a spike.

Robust strategies live on plateaus, not peaks.

A wide region where the strategy stays good even when the parameter is slightly off is worth far more than a sharp peak that only works at one number you will never hit again live.

The market will never hand you the exact value you optimized to.

So stop hunting for the peak.

Start looking for the plateau.

Join the waiting list to get early access and learn more on how to not fall into this trap: https://t.co/a6C3n3gu7F

Coiling under a declining MA stack is different from a neutral squeeze: the MAs aren't just overhead; they're compressing from the top too. Direction feels asymmetric given the context. Have you looked at how BTC 4H squeezes actually resolve when the price is below all major MAs? Easy to run the historical hit rate to see whether the bias is as bearish as the setup looks.

The tricky part is that perps lead spot on genuine breakouts too: the signal looks the same going in, and you only know which it was after price resolves. Curious whether you've pinned down a quantitative threshold for when the divergence becomes a fade signal or whether it stays a structural discretionary read. That's pretty easy to codify and backtest across prior BTC cycles to see if there's a reliable edge or whether it needs more context to hold up.

Hash Rate - Ep. 177: Bitsec SN60 Beats Mythos(!)

🧙 Guest: @yubrew of @bitsecai

A Bittensor $TAO Subnet Just Beat Anthropic's MYTHOS at Cybersecurity

00:00 Introduction to Bitsec

03:01 Jailbreaking Fable: Mythos Unleashed

12:02 The Competitive Landscape

17:49 The Future of Bitsec

30:03 John Yu's Journey into Cybersecurity

40:46 Subnet Token

44:53 Sales Strategy

49:40 Final Thoughts and Future Directions

Optimization is where good strategies quietly die.

Not because optimizing is wrong.

But because it feels like progress while doing the opposite.

You change a parameter. The metric improves.

You change another. It improves again.

Every step feels like skill.

But improvement measured on the same history you are fitting to is not improvement.

It is memorization wearing the costume of skill.

Validation told you the strategy might be real.

Optimization is where you can quietly make it fake again by tuning it so perfectly to the past that nothing is left for the future unless you understand what you are doing. Edgecraft can show you the right way.

The cleaner the curve gets, the more you should ask:

Am I improving the strategy?

Or just teaching it to recite history?

Why we had to build our own trading strategy engine.

When we started building Edgecraft, we did not set out to build a trading engine. We set out to trade with confidence. The engine was a missing puzzle piece that revealed itself only once we reached for it and found nothing on the shelf that fit.

Here is the thing: every existing solution does one or two things well. We needed all of them at once. And the moment you do, you are in build-it-yourself territory.

It had to be market-like. A simulation is only as honest as its assumptions. We wanted execution close to real conditions: fills, fees, slippage, funding, the things that quietly decide whether a strategy is profitable or just looks profitable on a chart.

It had to be fast. A strategy is not validated by one backtest. It is validated by thousands, across regimes and parameter sets. Slow feedback kills iteration.

It had to be flexible. We needed to spin up variants without the execution model quietly breaking underneath us. This is where most solutions thin out.

It had to optimize the parameter space. Not just run a strategy, but search the landscape around it, to see where it is robust and where it sits on a fragile knife-edge.

It had to let us explore the data. We wanted to interrogate the results, to look at mountains of trade data and understand what it was telling us.

It had to run live, and run live reliably. No crashes, clean recovery, real monitoring, full visibility into what the system is doing at every moment. This is the part almost nobody talks about.

And it had to do all of this for perpetual crypto markets. Perps with cross and isolated margin are not spot assets. Not forex, not stocks, not CFDs. The margin mechanics, the funding, the liquidation model have to be simulated as what they are.

For almost every item, a solution exists somewhere. But each solves a slice. The seams are where strategies go to die: where your fast backtester and your live executor quietly disagree about what a fill means, and you do not find out until real money is on the line.

So we built our own. One engine, market-realistic, fast, flexible, optimizable, observable, built for perps from the ground up, with the same model from backtest to live. The thing you validated is the thing that trades.

A trading idea is not a strategy until the equation works.

Win rate alone tells you nothing.

A 70% win rate can lose money.

A 40% win rate can make money.

Costs can turn a good-looking backtest into a negative expectancy strategy.

The only question that matters is whether the relationship between win rate, average win, average loss, and costs creates positive expected value.

Edgecraft helps you explore that faster.

Start with your own idea.

Use the Edgecraft agent to generate strategy architectures.

Test variations.

Compare the trader’s equation across them.

Keep what has potential.

Kill what does not.

That is how trading ideas become evidence-based strategy portfolios. Join the waiting list for early access: https://t.co/a6C3n3gu7F

If you want to read more about the trader's equation: https://t.co/Y18WFOVoAA

A strategy starts to become interesting when it survives being wrong.

Wrong costs.

Wrong slippage.

Wrong assumptions.

Wrong parameters.

Wrong asset.

Wrong market regime.

Wrong timing.

That is the point of strategy validation.

Not to prove that the backtest was good.

But to understand how fragile the edge is.

Does performance disappear if parameters move slightly?

Does it only work on one asset?

Does it rely on one exceptional period?

Do most returns come from a few trades?

Does drawdown expand dramatically under slightly worse assumptions?

Does the strategy still make sense when the market changes?

Capital should not go to the prettiest backtest.

It should go to strategies that survive questioning.

This is why we are building Edgecraft: to give traders ready-to-use tools for validating strategies properly, without needing to become engineers, coders, or statisticians just to understand whether an idea deserves risk.

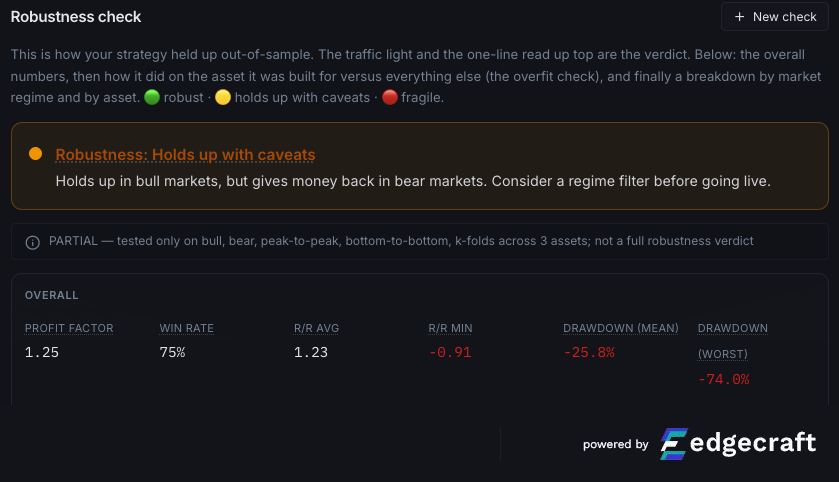

This strategy was optimized for BCHUSDT over a period of almost 4 years, which wasn’t balanced perfectly, meaning it had a bullish bias. The OOS validation came 100% in a bear market.

The numbers stay solid if the preparation is also robust.

Join the waitlist for early access to this strategy and the platform that gives you access to everything you need for trading with confidence: https://t.co/a6C3n3gu7F

Sentiment is a good macro indicator to use to switch from running short strategies to long and vice versa. I find it difficult to trade on this signal alone. Too noisy on its extremes to have good management of trade. Do you actually trade on it, or are you using it in a similar fashion?

Sometimes the biggest improvement to a strategy does not come from changing the core idea.

It comes from understanding when the idea should or should not be active.

A strategy might look average overall.

But then you discover it behaves very differently depending on price action:

during strong trends,

after volatility expansion,

near range breaks,

after failed breakouts,

during compression,

after large impulse moves,

or when momentum starts fading.

The core signal may be useful.

But only under certain conditions.

That is where a lot of traders stop too early.

They backtest the strategy, look at the headline metrics, and decide whether it is “good” or “bad.”

But sometimes the real question is:

“What is the strategy missing?”

Maybe it needs a regime filter.

Maybe exposure should change dynamically.

Maybe entries should be skipped after certain price structures.

Maybe position sizing should respond to volatility.

Maybe exits should adapt when momentum weakens.

These overlooked angles can drastically move the needle, and at Edgecraft, this is exactly the kind of work our agent is built to investigate. The possibilities are only limited by your creativity.

Strategy validation is not only about finding reasons a strategy might fail; it is also about discovering what the strategy is trying to tell you.

Sign up to get early access and start understanding what you use to trade: https://t.co/a6C3n3gu7F

A strategy can pass an out-of-sample test and still not deserve capital.

That sounds uncomfortable, but it is true.

OOS is useful because it tests the strategy on data it was not directly optimized on.

But OOS is not magic.

The period might still come from the same regime. The same asset. The same volatility environment. The same liquidity conditions. The same market behavior that made the in-sample test look good.

So yes, passing OOS is better than only passing in-sample.

But it does not prove the edge is robust.

A strategy can pass OOS because the idea is strong.

Or because the future briefly looked enough like the past.

That is why the question is not just:

“Did it work out-of-sample?”

The better question is:

“What kind of out-of-sample did it survive?”

At Edgecraft, this is one of the things we care deeply about: helping traders move beyond a single backtest result and understand how their strategy behaves across different assets, assumptions, and market conditions.

Because validation should not stop at “it worked on unseen data.”

That is only one gate.

Not the finish line.

To get access to this strategy or to create your own, join the waitlist: https://t.co/a6C3n3gu7F

Fully agree, and so few traders are aware of these things or take them into account correctly when they backtest or optimize. This is why we include all the headwinds a strategy will hit in live conditions by default in the backtesting process, optimization, and validation. Traders need a system that will point out exactly what the delta is between the costs they took into account and what the reality is during live trading so they can re-test and work on improvements at the earliest sign of false assumptions.

The most important question in strategy development is not

“Does this backtest make money?”

It is:

“Does this strategy deserve capital?”

Those are very different questions.

A backtest can be profitable because the idea is real.

But it can also be profitable because of overfitting, bad assumptions, ignored costs, optimistic execution, one lucky regime, or a few oversized trades.

Before a strategy deserves capital, it needs to survive more than a historical simulation.

It needs to survive scrutiny.

That is the problem we are building Edgecraft around.

Not just helping traders run backtests, but helping them validate strategies properly with ready-to-use tools for stress testing, robustness checks, execution assumptions, and deeper strategy analysis.

Because a good-looking backtest is not enough.

The real question is whether the strategy deserves risk.

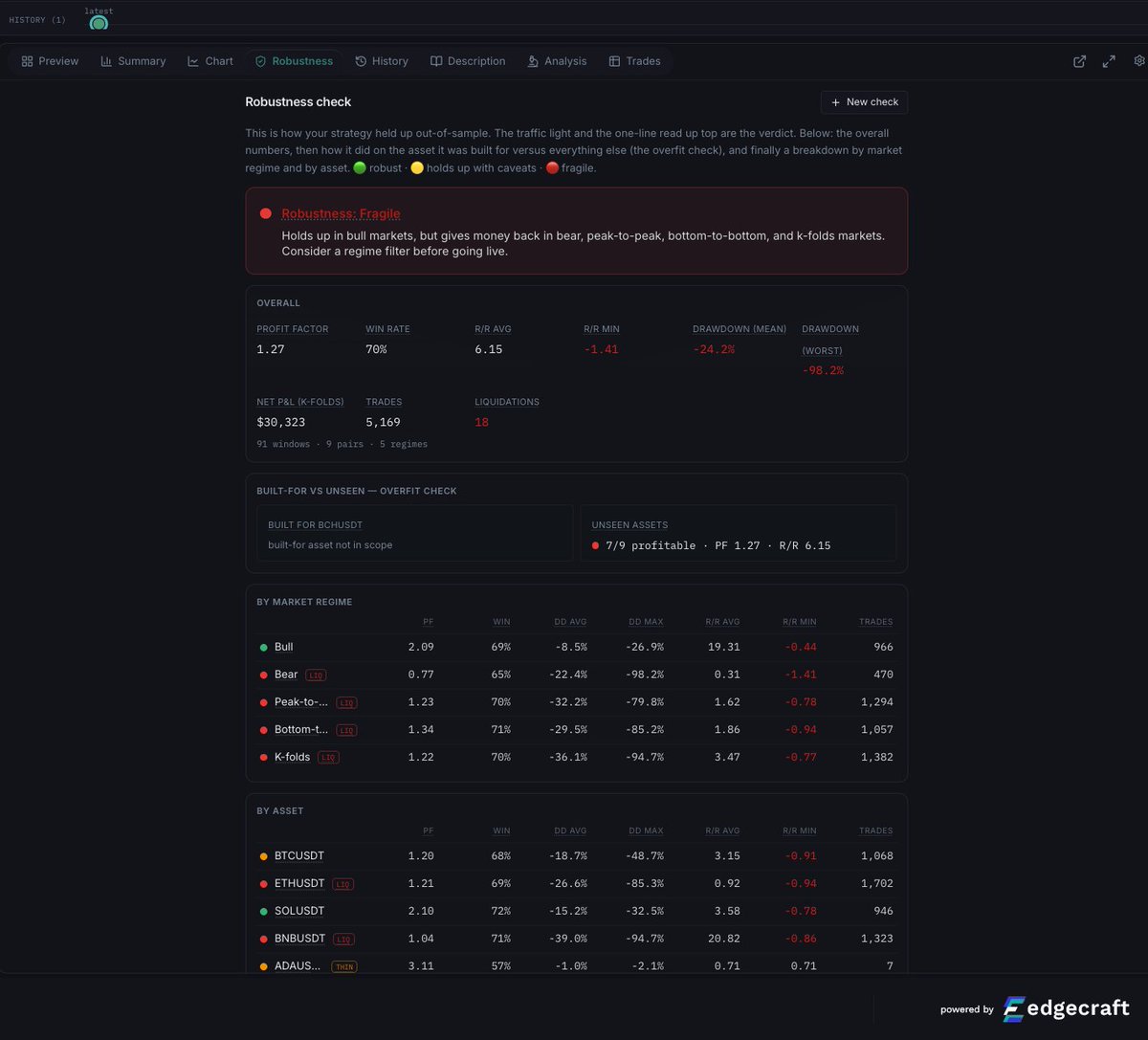

A strategy worked on and backtested over 5 years on BCH that looks solid and ready to be used live in fact has many issues and is not ready. The most obvious being that it doesn’t win for an entire year in 2022.

To get access to this strategy or to create your own join the waitlist: https://t.co/a6C3n3gu7F