Stablecoins made settlement global, 24/7, and programmable.

But payments are a full-stack problem. The next frontier is making settlement usable at scale -- trusted, liquid, compliant, reconciled, and accessible for businesses, users, and agents.

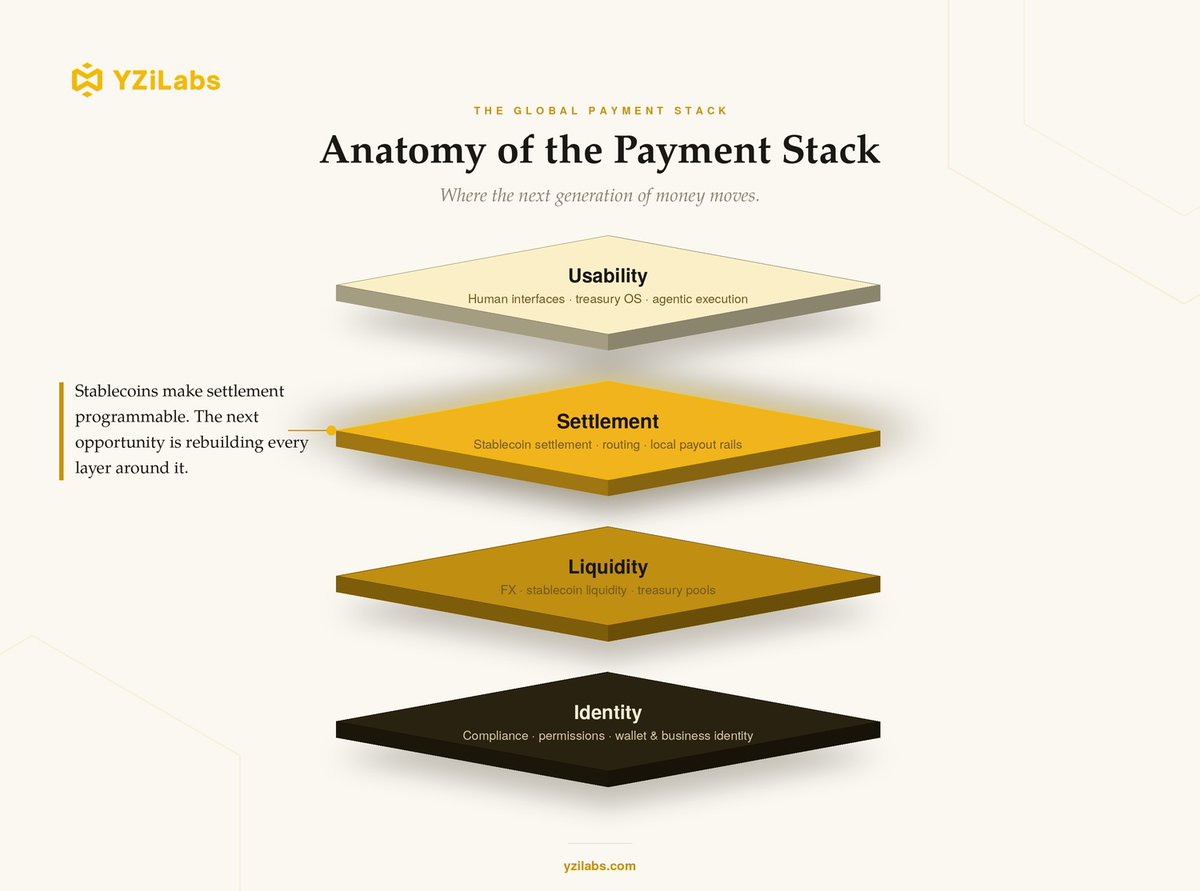

At YZi Labs, we are looking for founders rebuilding the key payment layers: Identity, Liquidity, Settlement, and Usability.

More soon as we unpack our thesis.

Saturday morning. A family in London sends $5,000 to Lagos.

The stablecoin arrives in 3 seconds.

The fiat needed to fund it? Stuck until Monday. Because banks don't work on weekends.

Fintechs processing these payments have to front the capital themselves. At scale, that's tens of millions locked up every weekend.

This is the gap that needs to be fixed, the settlement gap between instant crypto rails and legacy banking infrastructure.

This is what @NaraUSD is built to solve.

Yield has to come from somewhere.

At @NaraUSD, ours comes from real assets: short-duration, asset-backed, and structurally uncorrelated to crypto markets.

Today we're introducing our first strategy partner @FasanaraCapital and asset partner @MidasRWA 🧵

This is what we mean when we say NaraUSD+ yield is backed by real economic activity.

Not token emissions. Not recycled liquidity. Trade receivables from real businesses with real repayment paths.

Full breakdown of the strategy and the numbers 👉

https://t.co/uXDNkFZxlj

Follow @NaraUSD ⏳

$194 trillion flows across borders every year.

Projected to hit $320 trillion by 2032.

DeFi's total TVL? Around $100 billion on a good day.

The opportunity isn't inside crypto. It's the trillions that hasn't touched it yet.

That's the market @NaraUSD is built for.

Source: @jpmorgan, 2026 Cross-Border Payments Trends.

The ugly consequences of duration mismatches are surfacing in private credit, both in TradFi and DeFi.

A product is only as liquid as its underlying assets.

If you're locking up capital in long-term debt while promising short-term liquidity, you're playing a dangerous game.

That’s why we’re focused on ultra short-term payment and bank settlement financing. At @narausd our aim is to build the most resilient RWA yield product in DeFi.

Public launch soon.

- Stablecoin lending on @aave: ~3%

- Basis trade on @ethena: 3.5%

- Payment financing: Target ~10% APR

The first two depend on trading activity, leverage, and crypto market conditions.

Payment financing doesn't. It's backed by real businesses moving real money, and the yield reflects the size of the opportunity, not the size of the risk.

That's where @NaraUSD plays.

DeFi lending is circular. It recycles crypto to leverage more crypto.

PayFi is linear. It finances real-world payment flows, invoices, remittances, and cross-border trade.

One compresses the second the market cools. The other doesn't care how crypto prices are doing.

That's the difference.

@NaraUSD is PayFi — yield backed by real payment flows, not the crypto market cycle.

1/3 Before crypto, I helped build a neobank in Southeast Asia. I watched businesses lose 3–5% on every cross-border transaction.

Wait days for settlements.

Get priced out of basic financial infrastructure.

Stablecoins fix the rails. But the gap between digital dollars and the real world?

Still broken. Today, we're fixing that. 👉

The best yield opportunity in stablecoins is not in DeFi.

It's hiding in the 1 to 5 day gap between when commerce happens and when banks settle.

We built Nara to capture it.