“I never use valuation to time the market. I use liquidity considerations and technical analysis for timing. Valuation only tells me how far the market can go once a catalyst enters the picture to change the market direction.”

— Stanley Druckenmiller

Many are asking why is SpaceX, $SPCX, NOT trading yet?

Here's exactly how the IPO process works and when the shares will be available to trade (Bookmark this):

The IPO was quoted at 9:50 AM ET and was expected to begin trading at 10:00 AM ET, but that does NOT guarantee shares will trade at that time.

Before trading begins, Nasdaq must complete a price-discovery auction where buy and sell orders are collected and matched.

At around 9:50 AM ET, "first indications" came out which are essentially a "gauge" of where the stock will open.

The first indications on $SPCX came in at $175/share, or a ~30% premium to the $135/share IPO price.

During this process:

1. Orders are entered, but no trades occur yet

2. Nasdaq continuously updates the indicative opening price

3. The opening price is adjusted until supply and demand are balanced

4. Only then does the opening auction occur and the first trade print

For major IPOs, delays are common such as Google in 2004 and Meta in 2012 which saw their first trades over 2 hours after the US market opened.

We expect the SpaceX IPO to open for trading within the next 60 minutes.

Buckle up for a historic day.

Thoughts on $ADBE

$ADBE is one of the most fascinating stocks in the market today because it highlights one of the most important lessons in investing. It continues to execute at a high level. Revenue continues to grow, margins remain exceptional, free cash flow is enormous, and millions of customers still rely on $ADBE products every day. Yet despite all of that, the stock has struggled for years hitting all time lows.

This confuses many investors, especially newer investors. They look at the financial statements and see a business that appears healthy. Then they look at the stock price and assume the market must be making a mistake. After all, if the business is improving and the stock is falling, shouldn’t that create an even better opportunity?

Sometimes the answer is yes. Some of the greatest investments in history occurred because the market became too pessimistic about a business whose future remained bright. But it is important to remember that the market is not trying to value what a company earned previously or even currently. The market is trying to value what that company might earn in the future.

This is where the story becomes interesting. $ADBE looked cheaper at $500 than it did at $600. It looked cheaper at $400 than it did at $500. It looked cheaper at $300 than it did at $400. Many investors looked at the declining valuation and concluded that the opportunity was becoming more attractive. Yet the stock continued to fall because investors were not debating the current business. They were debating what the business might look like in the future.

For decades, $ADBE built one of the strongest moats in software. Photoshop, Illustrator, etc became the standard tools used by creative professionals around the world. Entire careers were built around learning Adobe’s products. Millions of designers, marketers, photographers, and video editors integrated $ADBE into their daily workflow, creating an ecosystem that appeared almost impossible to disrupt.

Then artificial intelligence arrived and changed the conversation. For the first time, images could be generated with a prompt. Videos could be created automatically. Design work that once required years of expertise could suddenly be performed by almost anyone. The question investors began asking was not whether $ADBE remained a great company today. The question was whether $ADBE moat would be as strong five or ten years from now as it was five or ten years ago.

That distinction is incredibly important because stocks are ultimately claims on future cash flows, not current cash flows. Imagine owning a toll bridge that earns $100 million per year. If someone announces that a second bridge will be built beside yours five years from now, the value of your bridge immediately changes even though today’s profits remain exactly the same. Nothing changed in the present, but something changed in the future.

This is why investing can be so difficult. The numbers investors see today often tell a very different story than the future investors are attempting to price. A business can appear healthy while its long term competitive position weakens. At the same time, a business can appear expensive while its future becomes far more valuable than most people realize (ie $PLTR). The market spends surprisingly little time pricing the present and an enormous amount of time attempting to price a future that has not yet happened.

This is also why one of the most dangerous phrases in investing is, “The stock is down but the fundamentals are improving.” Investors have said that about newspapers as the internet emerged, department stores as ecommerce gained share, and cable television as streaming began taking over. In many cases the current business remained healthy long after the future business had already started to deteriorate.

1/2 👇

With unprecedented investor demand for the largest IPO in history (SpaceX), it's worth remembering a simple lesson:

A great company doesn't always make for a great investment at any price.

The median major IPO lost 31% in its first year & suffered a 53% drawdown along the way.

Very interesting and scary report from Morgan Stanley

The financial engineering behind hyperscaler capex

The truly unsettling part of the AI boom isn’t how much money is being spent

It’s how that money is being engineered through accounting

Hidden liabilities (> $1.8T)

Huge obligations sit off‑balance‑sheet: nearly $1T in purchase commitments, $800B+ in leases not yet started, $2T+ in RPO.

Future cash outflows that don’t show up as debt.

The coming depreciation hit

Profits look good only because spending is stuck in CIP.

Big Tech faces $520B+ in depreciation over 3 years.

ORCL’s depreciation ratio: 7% → 28%.

Supplier financing pressure

Unpaid capex is ~$110B.

ORCL’s DPO exploded from 35 → 170 days.

The whole supply chain is effectively financing the AI build‑out.

Lease accounting gray zones

Whether GPU contracts count as leases or services is subjective — and companies use that flexibility to shift billions on/off the balance sheet.

$ORCL = the most aggressive

Largest lease commitments, RPO up 300%+, capex‑to‑sales hitting 189%.

Oracle is running the highest financial leverage in the ecosystem.

BREAKING NEWS: Anthropic's latest model will NOT help you if it thinks your ML research/ML engineering is interesting, and/or will secretly degrade its IQ so that the average engineer won't notice. We are already seeing Anthropic's latest model's moderation filters our GPU inference research and programming 😭

So you can use the 5th/6th/7th best LLMs, getting 80-85% of the top guys' performance, but at an 85-95% discount in price?

You know what we call that? A commodity...

exactly what happened with LCD TVs, OLEDs, solar panels, electric cars, phones, etc

good luck with your AI IPOs!

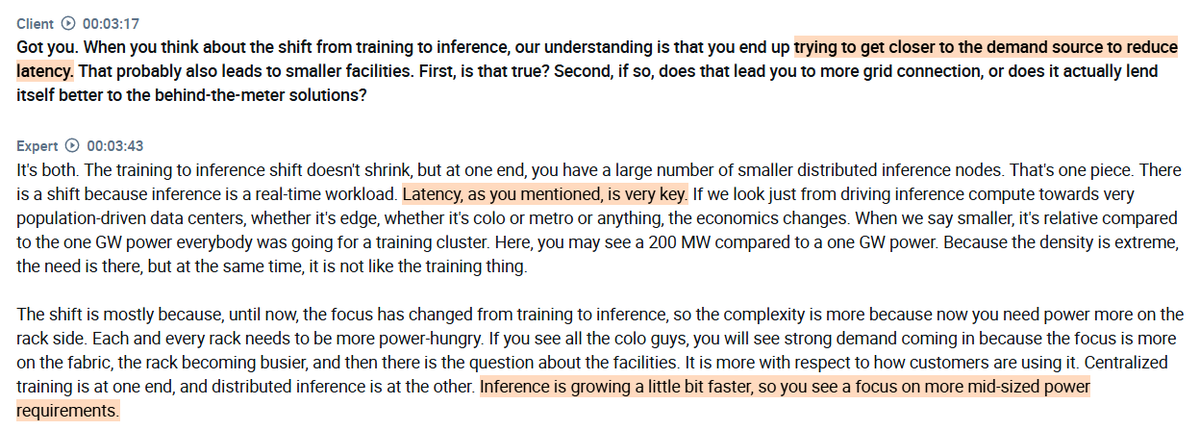

Interview with a $GOOGL employee who thinks we still have at least five more years of strong capital deployment ahead in the AI buildout:

1. The expert sees the AI data center build cycle as roughly at the halfway point, with the buildout expected to continue through 2035 before the next architectural shift. The current phase is transitioning from training-heavy investment to inference, and the expert sees at least five more years of strong capital deployment ahead. On the shape of spending, the expert expects the composition to shift rather than the total to decline, with heavy hardware investment dominating through 2027 and 2028 before giving way to a larger proportion of software and operational spend as AI becomes more of a commodity.

2. He emphasizes that the shift from training to inference pushes compute closer to population centers to reduce latency. Training clusters were chasing 1GW facilities, while inference deployments sit closer to 200MW, spread across colocation and metro sites rather than concentrated in one place.

3. The expert highlights a clear distinction between training and inference from a power design perspective. Training runs at flat, sustained load for weeks, making it predictable but requiring over-provisioned capacity, while inference is spiky and needs capacity available on demand even when mostly idle.

4. According to the expert, hyperscalers would willingly pay a 5-15% premium above the equivalent volume price to secure a shorter-duration PPA, with the logic being that retaining the option to extend, restructure, or walk away after 7 years is worth paying for compared to being locked into a 20-year commitment with no flexibility. The expert sees hyperscalers holding a stronger position in most markets, since power assets without a signed contract generate no revenue, giving hyperscalers leverage in all but the most supply-constrained regions.

5. The expert sees two forces driving the push for on-site power over waiting for grid connections. GPUs are expensive depreciating assets that generate no return when not running, and customer demand cannot wait, with any hyperscaler that fails to deploy quickly risking losing that customer to a faster competitor. In the near term, a small increase in power costs is not a deal breaker, but over a 5 to 10 year operating period that difference compounds, and the expert expects cost efficiency to become a much bigger priority by 2029.

found on @AlphaSenseInc

Citadel Securities just put institutional weight behind what the AI bulls won't say out loud.

In a new macro note titled "Tokenomics," Citadel makes the argument plainly: even the most powerful technology on earth still has to pass through the boring discipline of cost curves, capacity limits, and marginal returns.

The evidence is piling up:

– Amazon removed its token usage leaderboard

– Microsoft cancelled Claude Code subscriptions

– Multiple companies reporting unexpectedly massive token bills

Their conclusion is the part that matters.

Adoption is no longer about what AI can do in principle. It's becoming about the price and scarcity of the inputs needed to run it at scale. Compute. Power. Cooling. Memory bandwidth. Inference budgets. All real, all binding constraints.

And here's the kicker from the chart.

The Silicon Data LLM Token Expenditure Index, a benchmark for how much the market is actually spending on AI tokens, has started rolling over. Citadel reads it as a shift toward cheaper models. Companies substituting away from expensive frontier AI toward "good enough" alternatives.

That's economics 101 doing what it always does. When the price of something rises, people use less of it, or find a cheaper version.

Citadel sees a bifurcation forming. Frontier AI concentrated among a few firms with the balance sheets to absorb the cost. Everyone else quietly downgrading to simpler, cheaper models.

This is the part of every technology revolution the early narrative ignores.

The technology being real was never the question.

The question was always whether the economics could carry the valuations.

When one of the most sophisticated trading firms on earth starts writing about AI in the language of cost curves and rationing instead of limitless demand, the conversation has quietly changed.

The hype was about what AI could do.

The reckoning is about what it costs.

People will look back at the 2020s and kick themselves for missing the most obvious trades of this decade

To outperform, all you had to do is simply look at where the hyperscalers are spending their trillions of dollars in capex

Chips, data center infrastructure, and energy

My favorite 800V Power Semiconductor stocks ranked:

1. $WOLF (Wolfspeed) $2.7B market cap — The most asymmetric setup in the entire space. Wolfspeed controls the SiC substrate bottleneck, the foundational material every other SiC device maker needs. If the fab reaches target utilization, revenue could 3-5x from the current ~$713M run rate, and gross margins would inflect from negative to 40%+. At $2.7B, the market is pricing in heavy skepticism. A successful execution would make this a $10B+ company.

2. $NVTS (Navitas Semiconductor) $6B market cap — If Navitas captures even 2-3% of the AI data center power conversion TAM over the next three years, that’s a $500M+ revenue business on a fabless cost structure with 40%+ gross margins. The GaN IC technology is proven, the GeneSiC SiC portfolio adds a second vector, and the 59% revenue concentration in one AI-infrastructure distributor tells you where the growth is coming from. From a 3-year view, the revenue base could be 10x larger than today.

3. $AEHR (Aehr Test Systems) $1.5B market cap — The purest picks-and-shovels play on SiC scaling. Every SiC wafer that Wolfspeed, onsemi, STM, Infineon, or Rohm produces needs burn-in testing, and Aehr’s FOX-XP platform is the standard tool. Revenue is ~$100M and growing rapidly, but SiC production volumes are projected to 5-10x over the next five years. Aehr’s revenue is directly levered to that ramp with high incremental margins. A $100M revenue equipment company serving a market that’s about to quintuple has obvious math.

4. $VICR (Vicor Corporation) $5B market cap — Vicor’s factorized power architecture and power-on-package modules solve a physics problem that gets worse with every GPU generation: delivering 1,000+ amps at sub-1V to a processor die without unacceptable voltage droop and heat. If this architecture becomes standard in AI accelerator designs, Vicor’s content per server could be $500-1,000+. Revenue is ~$400M today. In a bull case where 2-3 major AI chip platforms adopt Vicor’s approach, this is a $2B+ revenue company at 50%+ gross margins, a $25B+ market cap.

5. $AOSL (Alpha & Omega Semiconductor) $1.5B market cap — The most overlooked name in power semi. AOSL makes power MOSFETs and PMICs for computing, server, and industrial applications. At $1.5B market cap and ~$650M revenue, it trades at ~2.3x sales, a fraction of MPWR’s 37x. The company is modestly profitable, has real products shipping into server power applications, and would benefit enormously from any broadening of AI power demand beyond the top-tier suppliers. This is the deep value pick: if the AI power theme lifts all boats, AOSL re-rates from 2x to 5x sales and the stock doubles without heroic assumptions.

Honorable mentions:

$DIOD $XFAB $ON $POWI $MPWR

Is this another dot-com bubble?

This chart shows how much money sits inside the stock market relative to all the money that exists. The Stock market is 3x bigger than all the money available in the economy.

It’s hovering near its own 2000 era peak, no wonder traditional investors are sounding the alarm about the next bubble.

So the question writes itself: are we here again?

This ratio has 2 numbers:

- Top: market cap

- Bottom: M2 (money supply)

Only watching the top misses the other half.

In 2000, the bottom was growing. M2 expanded and the ratio still tripled. That tells you the move came almost entirely from price. Money inside the market relative to money that existed had run genuinely too hot.

This time, the bottom did something different. M2 peaked in April 2022, then contracted and did not regain its high until March 2025. For three years the denominator shrank while price climbed. Part of the parabola you are looking at is arithmetic.

Every system has limits to growth. The strongest driver, the reinforcing loop, is often the same force that ends the run.

AI capex feeds earnings expectations, which feed market cap, which feed more capex. The loop spins. If the driver does not limit itself, a balancing loop arrives uninvited: less money supply, tighter liquidity. The system gets forced back to balance.

So is this dot com again?

I do not think so, yet. We happened to find a new investable technology AI which the internet itself gave birth to. Record revenue earned across the whole world. The names carrying the index actually have cash flow. M2 now reaccelerating to fresh records above 22 trillion. So from here the ratio can only keep rising.

Predicting when this ends will give you sleepless nights. Nobody times the top of a reinforcing loop. You do not need the date. You need the flows.

Understand the flows feeding the stock and watch them carefully, and you are already thinking like the top 10%.

Act on what they tell you, and you become the top 1% of market operators.

The chart tells us how far price reached last time.

The inflows tell us when the move is running out of juice.

Two members of Congress bought $MU early and now they are both in a new AI stock

Rep. Cisneros (D) bought $LITE on April 14th

Rep. Gottheimer (D) bought $LITE on May 22nd

• Cisneros sits on the Armed Services Intelligence Subcommittee. And Lumentum sells lasers directly to the U.S. military

• Gottheimer sits on House Intelligence and co-sponsored legislation targeting AI chip export controls. Lumentum's chips are subject to those exact controls

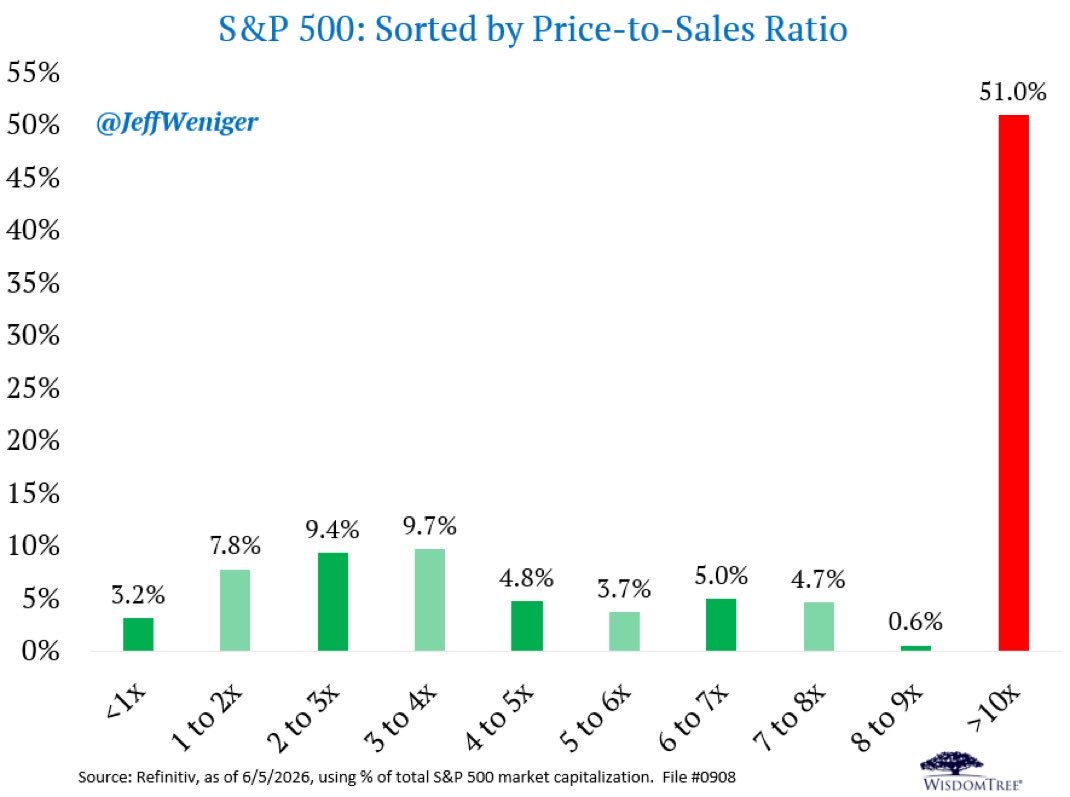

51% of the S&P 500's market cap is in stocks trading above 10x sales.

Half the index.

In 2002, after Sun Microsystems crashed 90%, CEO Scott McNealy famously said this about his own stock at 10x sales:

"At 10x revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. Zero costs. Zero R&D. Zero taxes. Zero employees. What were you thinking?"

He was explaining why investors had been insane to pay it.

Today, half the S&P 500 trades there.

Different decade. Same math.

A perspective on how stretched current valuations are:

$AVGO traded at a median sales multiple of just 5x before 2023. Today, it trades near 25x.

Wall Street expects $AVGO to reach $250 billion in sales by 2029.

But even if that happens, a re-rating back to 5x sales would still imply roughly 30% downside from today’s level.

That is the real risk: AI capex does not need to collapse. It only needs to stop accelerating.

Even if hyperscaler capex stays flat at an elevated level, the market can still stop paying peak-cycle multiples for AI infrastructure names.

It is not a matter of if, but when.

Excellent piece from Alexander Chartres titled "Iliads & Odysseys."

The TL;DR is to own:

> Real assets

> Defense

> Cybersecurity

> Semiconductor niches

> Automation and robotics

> Applied AI

> Precious metals

> Energy Commodities

Love this list and completely agree.

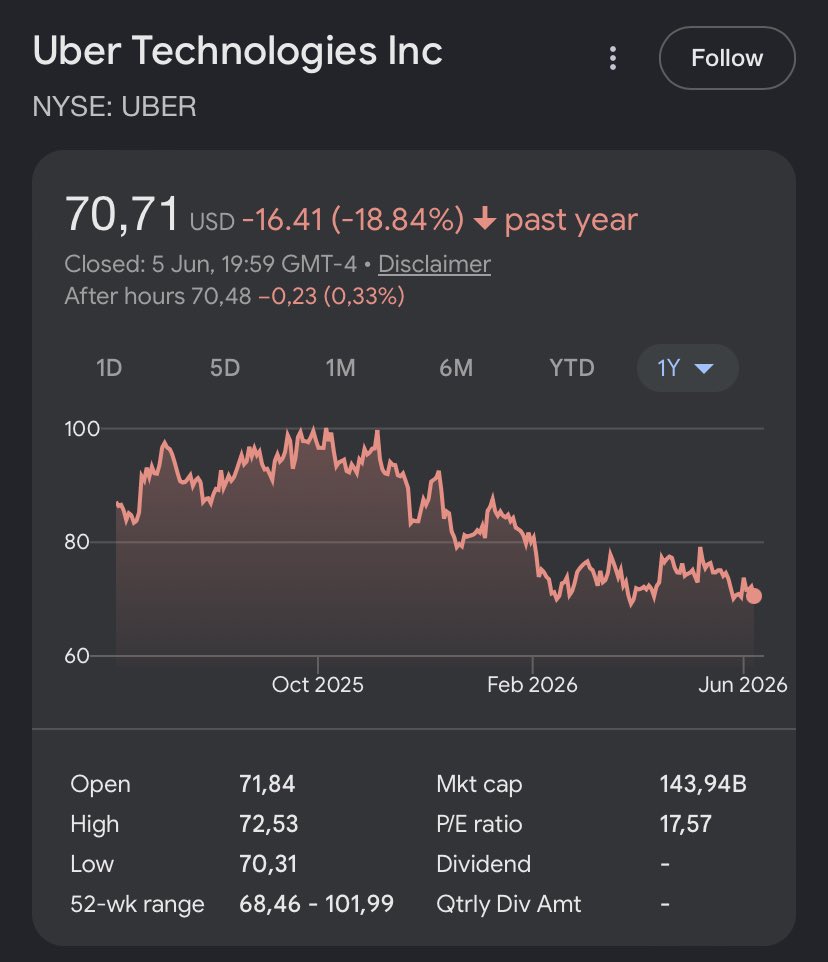

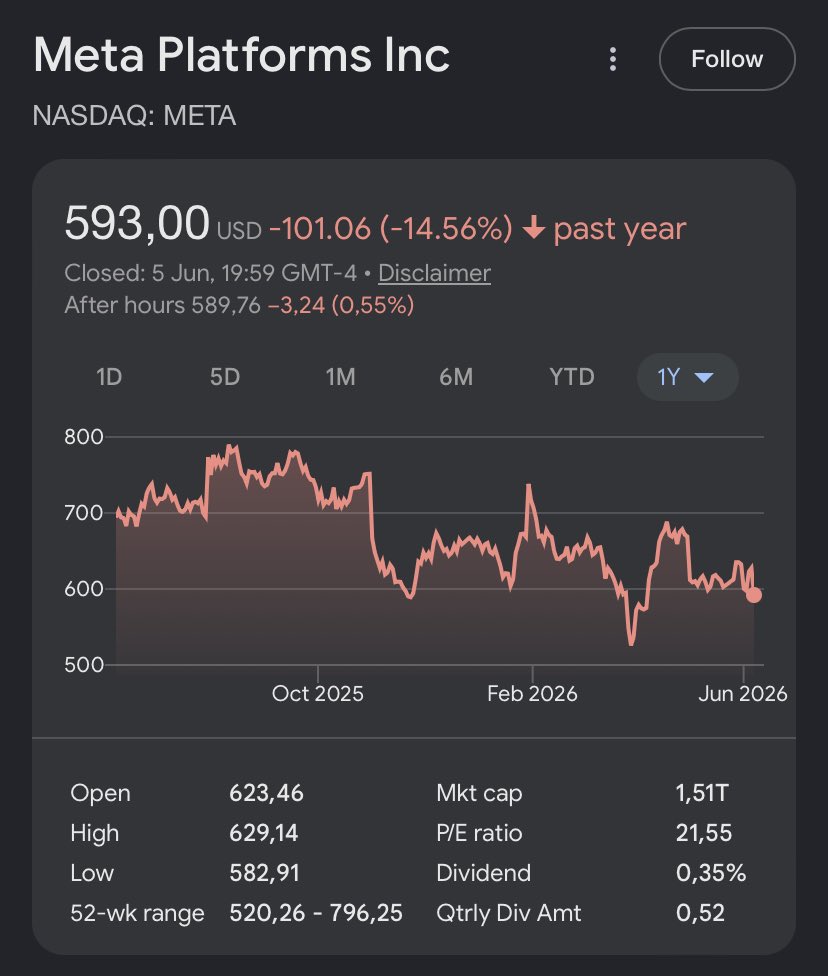

Bill Ackman is right.

- $META at 18x forward earnings

- $UBER at 16x forward earnings

Two of the strongest companies in the world, trading at no brainer levels.

Yet, people prefer owning unprofitable stocks at 100x sales because they are related to AI.

Never ends well.