A wrongful “WRITTEN-OFF” reporting by @IDFCFIRSTBank remained on my credit profile for years despite no intentional default from my side.

Before this issue, I had successfully repaid multiple loans through IDFC-linked lending with a clean repayment history.

After the wrongful reporting period:

• Loan applications became difficult

• Mainstream lenders rejected applications

• I was pushed toward NBFC loans charging 25%–35% interest

• My financial credibility suffered for years

Only after repeated escalations, disputes, RBI complaints, calls, emails and public pressure were the bureau records finally corrected.

I have documentary proof including:

✔️ Bureau correction confirmation

✔️ Loan rejection letters

✔️ High-interest loan records

✔️ Complaint history & call recordings

Credit reporting errors can financially corner a person for years.

Seeking a fair and accountable resolution before proceeding further legally.

@RBI@CIBIL_Official@FinMinIndia@jagograhakjago@consaff@moneycontrolcom@CNBCTV18News@ETNOWlive

One important detail in this entire credit reporting issue:

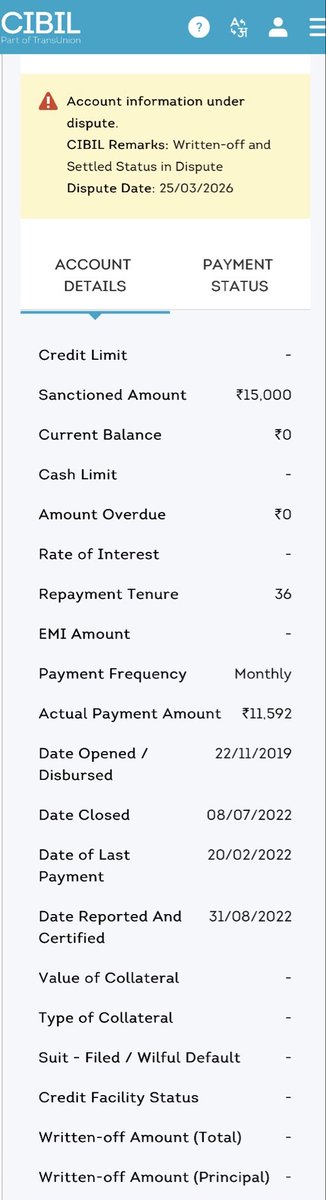

Even after the “written-off” status was eventually removed, the matter was still not fully resolved.

The account continued to remain under dispute status.

In the end, I personally had to contact CIBIL again, explain the situation, and follow up myself to get the remaining issue resolved.

Consumers should not have to become experts in credit bureau processes to correct reporting issues.

@CIBIL_Official@IDFCFIRSTBank@RBI

#CIBIL #CreditScore #ConsumerRights #Banking

A dispute raised with CIBIL regarding my account linked to @IDFCFIRSTBank was initially closed after the bank confirmed the reporting was “correct”.

Later, the same reporting was corrected.

Even after the correction, I still had to personally follow up with CIBIL again to resolve the remaining dispute status issue myself.

This process took multiple escalations and months of effort over a single credit reporting issue.

@CIBIL_Official@RBI

#CIBIL #CreditScore #ConsumerRights

My CIBIL dispute against @IDFCFIRSTBank was initially closed after the bank confirmed the reporting was “correct”.

Later, the same reporting was corrected.

Even after that, the dispute status still remained active until I personally contacted CIBIL again and got it resolved myself.

This entire process took multiple escalations, repeated follow-ups, and months of effort over a single credit reporting issue.

@CIBIL_Official@RBI

#CIBIL #CreditScore #ConsumerRights #Banking

I first raised a dispute with CIBIL regarding the reporting linked to my account by @IDFCFIRSTBank.

CIBIL closed the dispute after the bank confirmed the reporting was “correct”.

I then raised RBI complaints and continued follow-ups for weeks.

Later, the “written-off” status was removed — but the issue still wasn’t fully resolved because the account remained under dispute status.

In the end, I personally had to contact CIBIL again and explain the issue myself to finally get the remaining correction completed.

This entire process showed how difficult it can be for consumers to correct inaccurate credit reporting even after partial corrections are made.

@RBI@CIBIL_Official

#CIBIL #CreditScore #ConsumerRights #BankingSector

I first raised a dispute with CIBIL regarding the reporting linked to my account by @IDFCFIRSTBank.

CIBIL closed the dispute after the bank confirmed the reporting was “correct”.

I then raised RBI complaints and continued follow-ups for weeks.

Later, the “written-off” status was removed — but the issue still wasn’t fully resolved because the account remained under dispute status.

In the end, I personally had to contact CIBIL again and explain the issue myself to finally get the remaining correction completed.

This entire process showed how difficult it can be for consumers to correct inaccurate credit reporting even after partial corrections are made.

@RBI@CIBIL_Official

#CIBIL #CreditScore #ConsumerRights #Banking

In March 2026, my dispute with CIBIL was closed after @IDFCFIRSTBank confirmed that the reporting linked to my account was “correct”.

After RBI escalation and continued follow-ups, the same reporting was later corrected.

This is exactly why inaccurate credit reporting can become so damaging for consumers.

A single bureau entry affected:

• loan approvals

• borrowing costs

• financial credibility

for years.

@RBI@CIBIL_Official

#CIBIL #CreditScore #ConsumerRights #Banking

In March 2026, I raised a dispute with CIBIL regarding wrongful reporting by @IDFCFIRSTBank.

CIBIL closed the dispute after the bank confirmed:

“the credit information reported by them is correct” and “no changes” were required.

Only AFTER RBI complaints and repeated escalation did the bank later correct the bureau data.

Even after correction, the issue remained unresolved in dispute status until I personally coordinated again with CIBIL.

This raises a serious question:

If the reporting was originally “correct,” why was it later corrected?

Consumers should not have to:

• fight multiple escalations

• involve RBI

• repeatedly contact CIBIL

just to fix incorrect credit reporting.

@RBI@CIBIL_Official@IDFCFIRSTBank

#CIBIL #CreditScore #Banking #ConsumerRights #RBI #IDFCFIRSTBank

A wrongful “WRITTEN-OFF” reporting by @IDFCFIRSTBank remained on my credit profile for years despite no intentional default from my side.

Before this issue, I had successfully repaid multiple loans through IDFC-linked lending with a clean repayment history.

After the wrongful reporting period:

• Loan applications became difficult

• Mainstream lenders rejected applications

• I was pushed toward NBFC loans charging 25%–35% interest

• My financial credibility suffered for years

Only after repeated escalations, disputes, RBI complaints, calls, emails and public pressure were the bureau records finally corrected.

I have documentary proof including:

✔️ Bureau correction confirmation

✔️ Loan rejection letters

✔️ High-interest loan records

✔️ Complaint history & call recordings

Credit reporting errors can financially corner a person for years.

Seeking a fair and accountable resolution before proceeding further legally.

@RBI@CIBIL_Official@FinMinIndia@jagograhakjago@consaff@moneycontrolcom@CNBCTV18News@ETNOWlive

Dear Kia India,

I have already shared all booking and vehicle details via DM regarding forced insurance bundling by Pressana Automobiles, Erode, but have not yet received any update.

Vehicle already allotted in my name:

VIN: MZBEA813LTN051866

Booking date: 30.03.2026

Vehicle arrived at yard: 14.05.2026

Inspection completed: 15.05.2026

Despite this, dealership informed me that the vehicle may be delivered to another customer if I do not purchase insurance through them.

I am fully willing to provide valid insurance from my own insurer before registration and delivery.

Requesting urgent intervention from Kia India for fair resolution.

@kiacareindia #KiaIndia #KiaSeltos #ConsumerRights

Booked a Kia Seltos D1.5 6MT HTE on 30.03.2026 after clearly informing the dealer that I would arrange insurance independently.

After waiting nearly 2 months, the car was allotted in my name:

VIN: MZBEA813LTN051866

Vehicle arrived at dealer yard on 14.05.2026 and I completed inspection on 15.05.2026.

Now the dealership is insisting dealer insurance is “mandatory” and has stated that if I do not purchase insurance through them, the car may be delivered to another customer despite allocation and inspection already completed.

I am fully willing to provide valid insurance from my own insurer before registration and delivery.

This is our family’s 3rd Kia vehicle, and I have never faced such pressure tactics before.

I request Kia India to kindly intervene and ensure fair customer treatment without forced insurance bundling.

#KiaIndia #KiaSeltos #ConsumerRights

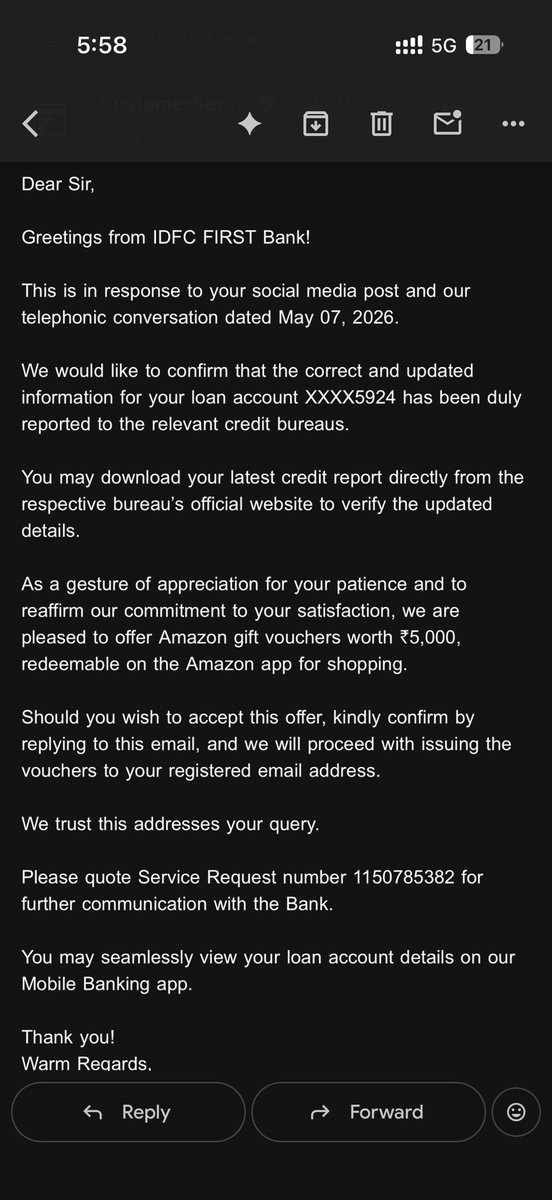

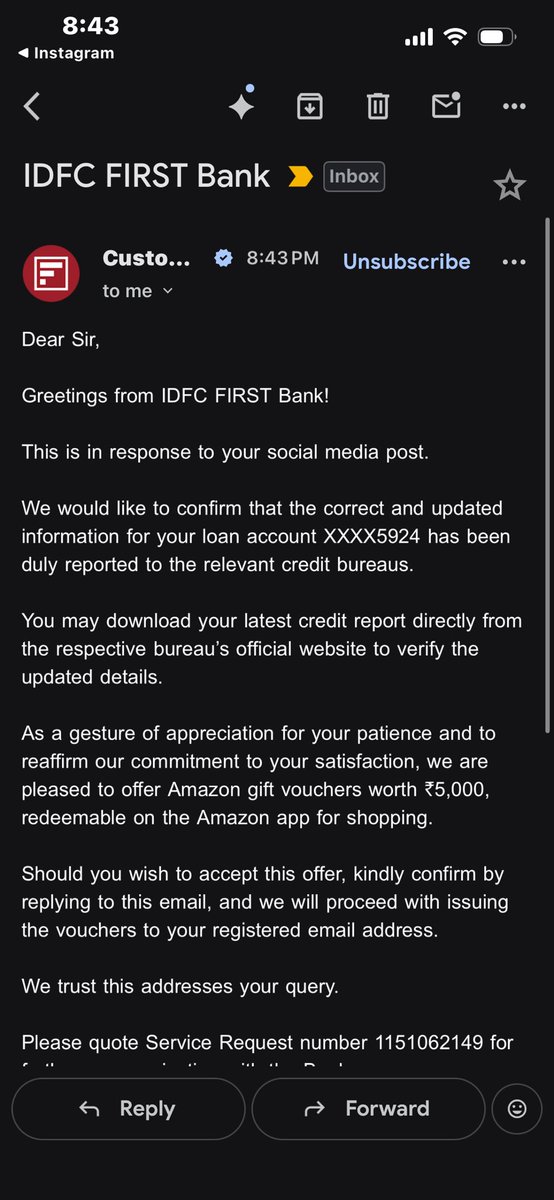

It has now been several days since @IDFCFIRSTBank acknowledged the incorrect credit bureau reporting linked to my account and confirmed the correction.

The bank repeatedly offered only ₹5,000 vouchers despite the long-term financial impact caused by the wrongful reporting.

After multiple identical template responses, there has now been no meaningful update regarding:

• compensation for financial loss

• rejected loan applications

• high-interest borrowing forced through NBFC/private lenders

• damage caused to my creditworthiness over multiple years

I am preserving all emails, SR numbers, and supporting documents for formal escalation.

@RBI@CIBIL_Official

#ConsumerRights #CIBIL #CreditScore #Banking #FinancialDamage #IDFCFIRSTBank

Over the past several days, @IDFCFIRSTBank has repeatedly sent identical template responses acknowledging that the incorrect bureau reporting linked to my account has now been corrected.

The bank has also repeatedly offered ₹5,000 vouchers as a goodwill gesture.

However, despite multiple acknowledgments, there has still been no meaningful response regarding:

• the years of impact on my credit profile

• rejected loan applications

• reduced access to mainstream credit

• higher borrowing costs through NBFC/private lenders

At this stage, I am compiling all communications and proceeding through formal escalation channels.

@RBI@CIBIL_Official

#CIBIL #CreditScore #ConsumerRights #Banking #FinancialDamage #LoanIssues #IDFCFIRSTBank

Another identical template response has been received from @IDFCFIRSTBank.

The bank continues to:

• acknowledge the bureau correction

• repeat the same ₹5,000 goodwill offer

• avoid addressing the long-term financial impact caused during the years the incorrect reporting remained active

The issue is not merely about correcting a CIBIL entry today.

The concern is the financial loss, loan rejections, reduced credit access, and high-interest borrowing I faced during the affected period.

All communications and responses are being documented as I proceed through formal escalation channels.

@RBI@CIBIL_Official

#CIBIL #CreditScore #ConsumerRights #Banking #FinancialDamage #LoanIssues #IDFCFIRSTBank

Another response received today from @IDFCFIRSTBank.

The bank continues to confirm that the incorrect bureau reporting linked to my account has now been corrected and is repeatedly offering ₹5,000 vouchers as a goodwill gesture.

However, the actual financial impact caused over the years still remains unaddressed.

Because of this reporting issue:

• Loan approvals became difficult

• My credit profile suffered

• I was forced toward high-interest borrowing options

• I ended up paying significantly higher interest rates through NBFC/private lending

I am requesting a fair and proportionate resolution based on the long-term financial impact caused.

@RBI@CIBIL_Official

#CIBIL #CreditScore #ConsumerRights #Banking #LoanIssues #FinancialDamage #IDFCFIRSTBank

Another response has now been received from @IDFCFIRSTBank.

The bank continues to:

• Confirm that the incorrect bureau reporting linked to my account has now been corrected

• Repeatedly offer ₹5,000 vouchers as a goodwill gesture

However, the core issue remains unresolved.

The wrongful reporting remained on my credit profile for years and had real financial consequences:

• Loan rejections

• Reduced borrowing eligibility

• Dependence on high-interest NBFC/private loans

• Significantly higher borrowing costs over multiple years

This matter is no longer only about correcting a bureau entry.

It is about accountability for the financial impact caused during the period the incorrect reporting remained active.

I will now be proceeding through formal escalation channels.

@RBI@CIBIL_Official@IDFCFIRSTBank

#CIBIL #CreditScore #ConsumerRights #Banking #FinancialDamage #LoanIssues #RBI #IDFCFIRSTBank

UPDATE:

@IDFCFIRSTBank has now officially confirmed via email that the credit bureau information linked to my account was corrected.

The bank has also offered ₹5,000 as a “gesture of appreciation”.

But the financial impact over the years was far greater than ₹5,000.

After the wrongful reporting on my credit profile:

• Loan applications were rejected

• I lost access to mainstream lending

• I was pushed toward high-interest NBFC/private loans

• I ended up borrowing at rates as high as 25%–35%+

This issue affected my financial credibility and borrowing costs for years.

I am still requesting fair accountability and compensation proportional to the actual financial damage caused.

@RBI@CIBIL_Official@IDFCFIRSTBank

#CIBIL #CreditScore #ConsumerRights #Banking #LoanRejection #NBFC #FinancialDamage #RBI #IDFCFIRSTBank

Weekend update on this issue:

@IDFCFIRSTBank has now officially confirmed through email that the incorrect bureau reporting linked to my account has been corrected.

The bank has also offered ₹5,000 vouchers as a goodwill gesture.

However, the impact of this issue went far beyond a temporary inconvenience.

For years after the wrongful “WRITTEN-OFF” reporting:

• Loan applications were rejected

• My credit profile was severely affected

• I had to depend on NBFC/private lenders

• I ended up borrowing at interest rates as high as 25%–35%+

I had already maintained prior successful repayment history before this issue occurred.

This is not only about correcting a CIBIL entry later.

It is about the financial damage caused during the period the incorrect reporting remained active.

Requesting proper accountability and fair resolution.

@RBI@CIBIL_Official@IDFCFIRSTBank

#CIBIL #CreditScore #ConsumerRights #Banking #LoanIssues #FinancialDamage #NBFC #RBI #IDFCFIRSTBank

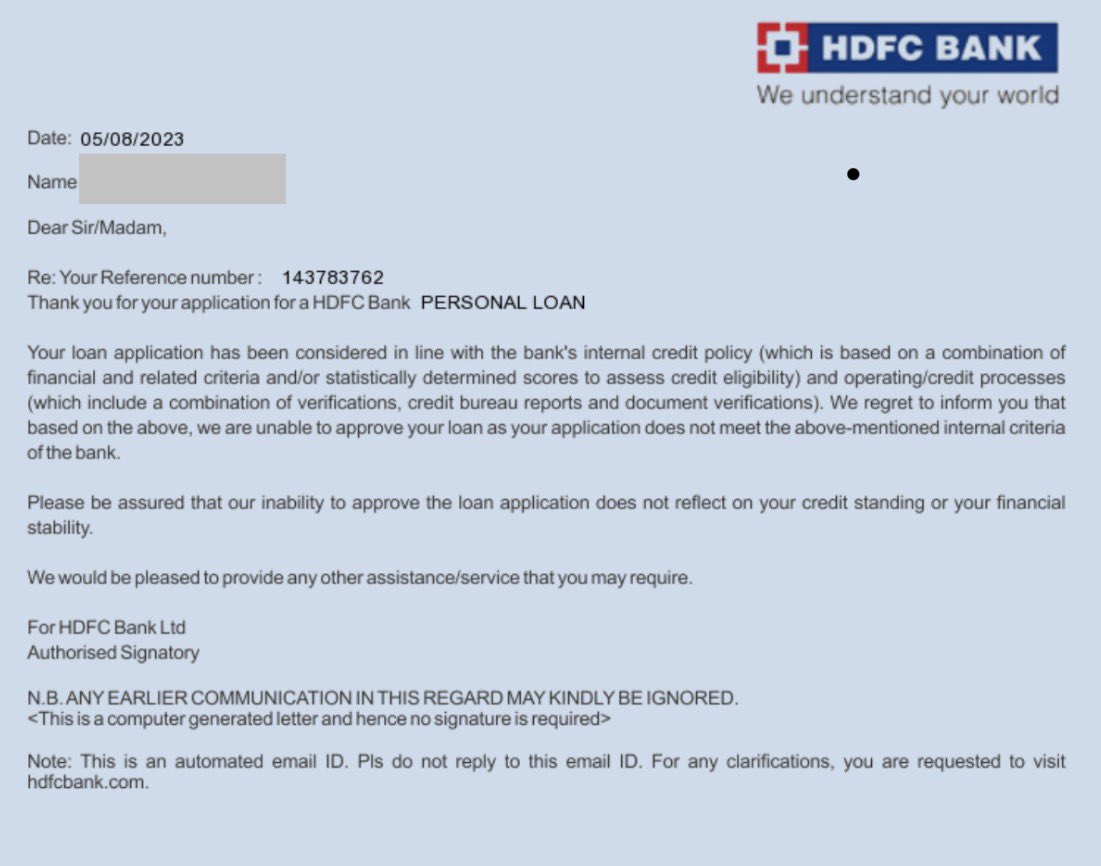

The most frustrating part is this:

Before the wrongful reporting, I had successfully handled multiple loans and maintained repayment discipline.

After the “WRITTEN-OFF” entry appeared on my credit profile:

• Mainstream lenders started rejecting applications

• I had to depend on NBFC/private financing

• Interest rates went as high as 25%–35%+

• Borrowing became significantly more expensive

This was not just a CIBIL issue on paper.

It had real financial consequences over multiple years.

@IDFCFIRSTBank@RBI@CIBIL_Official

#CreditScore #CIBIL #Banking #ConsumerRights #NBFC #PersonalFinance #LoanRejection #FinancialDamage #RBI #IDFCFIRSTBank