Nexspecto does not reject the old logic of community finance.

It upgrades its trust layer.

That journey now has a name:

On-Chain Community Finance.

#Nexspecto#ContriFi#OnChainCommunityFinance

Our new NexsPaper explores this journey:

From iROSCA to Nexspecto

How one of the world’s oldest financial behaviors can become access-to-financing infrastructure for the digital asset age.

#Nexspecto#ContriFi#OnChainCommunityFinance

Nexspecto’s thesis is simple:

Community finance is old.

ContriFi is its new financial language.

On-Chain Community Finance is its new rail.

#Nexspecto#ContriFi#OnChainCommunityFinance

Digital assets add a new rail.

Stablecoins, wallets, smart contracts and collateral logic can turn community finance into a more transparent and programmable infrastructure.

#Nexspecto#ContriFi#OnChainCommunityFinance

The real innovation is not “digitizing ROSCA.”

The real innovation is upgrading the trust layer of community finance.

From manual records to on-chain traceability.

From opaque decisions to verifiable allocation.

#Nexspecto#ContriFi#OnChainCommunityFinance

This is why Nexspecto is not built around speculation, leverage or yield promises.

It is built around access.

Transparent, community-powered, contribution-based access to financing.

#Nexspecto#ContriFi#OnChainCommunityFinance

ContriFi is not credit in the traditional sense.

It starts with contribution.

Contribution creates rights.

Rights are tracked transparently.

Access is allocated through predefined rules.

#Nexspecto#ContriFi#OnChainCommunityFinance

Nexspecto carries this lineage into a broader, blockchain-native architecture:

Contribution → Rights → Community Fund → Financing Order → On-chain allocation → Access to financing

We call this ContriFi.

#Nexspecto#ContriFi#OnChainCommunityFinance

The iROSCA thesis opened an important intellectual path:

Can rotating savings and finance be reimagined through a digital Islamic finance lens?

That question matters far beyond one model.

#Nexspecto#ContriFi#OnChainCommunityFinance

The logic is simple:

* regular contribution

* shared discipline

* a Community Fund

* access to financing in turn

What is slow alone can become faster with a community.

#Nexspecto#ContriFi#OnChainCommunityFinance

Across cultures, people have always saved together and accessed financing in turn.

ROSCA. Gün. Tanda. Susu. Stokvel. Chit fund. Kou. Gam’eya.

Different names. Same logic.

#Nexspecto#ContriFi#OnChainCommunityFinance

From iROSCA to Nexspecto

How Community Finance Became On-Chain Community Finance

Nexspecto did not begin as another crypto product.

It began with a deeper question:

Can one of the world’s oldest community finance behaviors be redesigned for the digital asset age?

#Nexspecto #ContriFi #OnChainCommunityFinance

Q: What is the plan to revive Nexspecto?

A: Bringing the $700B+ ROSCA market on-chain: integrating RWAs, liquidity partnerships, fiat ramps, and lower fees. Community power + blockchain transparency = global scale.

Q: Who is your primary target audience?

A: Everyday users needing predictable financing, while staying crypto-friendly. Easy wallets, fiat ramps, local ambassadors, and stablecoins make onboarding simple.

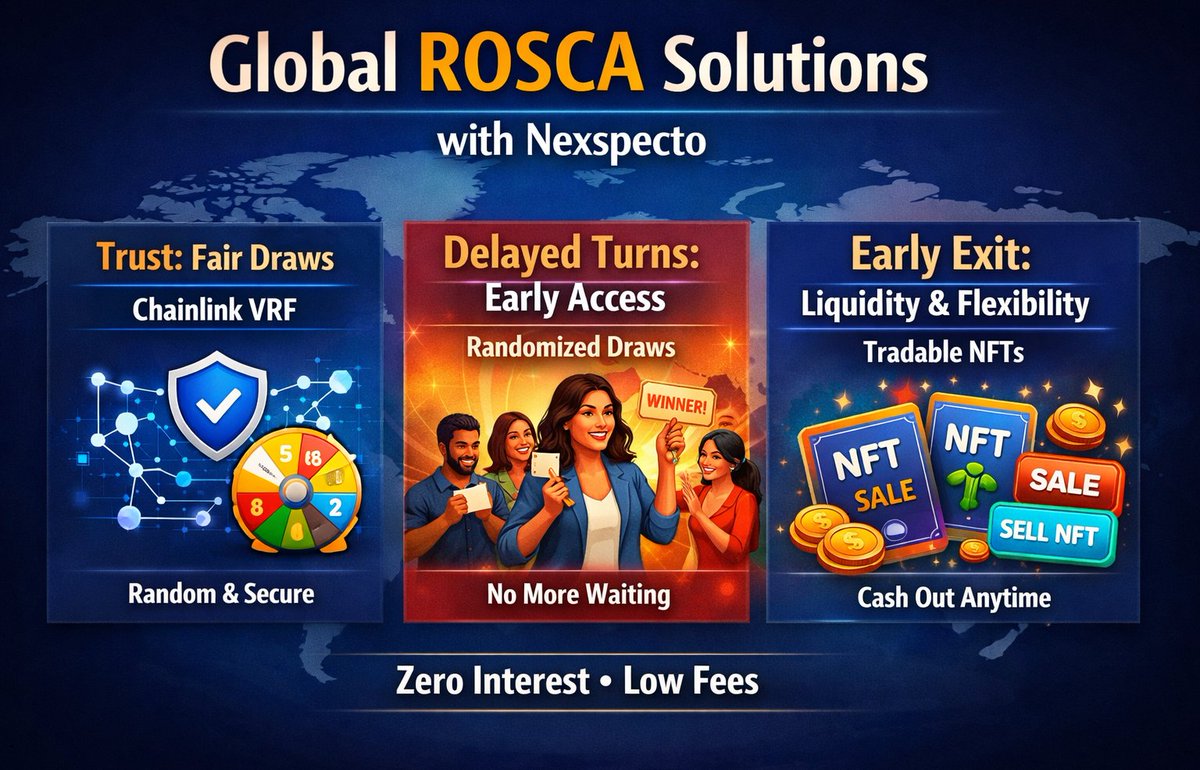

Q: How does Nexspecto solve ROSCA pain points in World?

A: • Trust: Chainlink VRF ensures fair draws.

• Delayed Turns: Randomized draws give early access.

• Early Exit: Tradable NFTs allow liquidity. All with zero interest and low fees.

Q: Will PECTO token holders vote on boosting parameters?

A: Governance mechanisms will expand once token processes are live. For now, community feedback shapes Nexspecto’s evolution.

Q: If many participants liquidate NFTs during a downturn, how does Nexspecto stay solvent?

A: Nexspecto isn’t built on NFT exits. It thrives because contributions continue and allocation rules remain transparent. Liquidity layers are enhancements, not the foundation.