1/

I know it's been a frustrating hold but after watching the entire Investor Day, I truly believe that $PYPL 🔵 is the best risk/reward opportunity in the stock market.

Check out my bull thesis below 👇🧵

If you enjoy, please follow, like and repost! I just started this account and I'm trying to grow it, so I appreciate all the help I can get :)

@Kross_Roads This seems like a flawed study? If someone searches men's shoes they will not get an AI summary and will be more likely to then click a link. If someone searches a knowledge based query they probably aren't looking to click any links anyway? Or am I misunderstanding

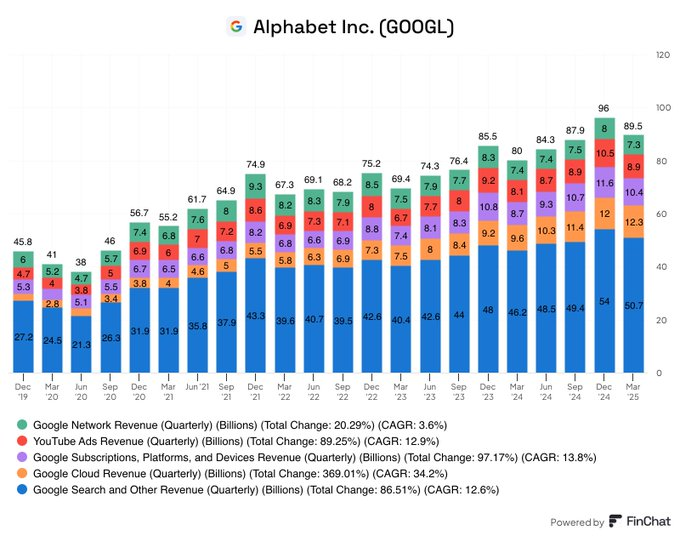

DID AI REALLY BREAK GOOGLE’S MOAT?

At $150, $GOOGL is trading at a $1.7T market cap. But if you break the business down by segments -- the way any rational buyer would in a private market -- you’d never land anywhere near that number. Because the sum of the parts already exceeds the whole.

You wouldn’t know that Google Cloud is scaling into one of the most profitable hyperscaler businesses in the world. You wouldn’t know that YouTube is a hybrid of $NFLX, $SPOT & TikTok -- with better margins. You wouldn’t know that Google Search still controls the digital tollbooth for the entire internet.

Because the market doesn’t care about fundamentals right now. It cares about narrative. And the narrative, since late 2022, has been this: Google missed AI. ChatGPT caught them off guard. OpenAI is the new frontier. Gemini is mid. Google is late.

But let’s pause.

That entire thesis is built on perception. Because when you actually break it down -- when you actually look at the revenue base, the margin profile, the market share, and the product velocity -- it becomes clear that this isn’t a company getting disrupted.

It’s a company getting mispriced.

Lets start with Cloud. A $50B revenue run rate, growing nearly 25% with expanding margins and a Rule of 40 score of 46. That’s better than $CRM. Better than $ORCL. Slap a 40x earnings multiple on it and you’re looking at a $700B valuation.

Now YouTube. It’s a $36B-a-year revenue machine, growing steadily, expanding monetization through Shorts, Premium, and Music, and dominating CTV share in the U.S. $NFLX is trading at 11x sales. Give YouTube the same and you’re sitting on another $400B.

So right there -- Cloud + YouTube = $1.1T. That’s 60% of Alphabet’s market cap today.

And Search? Still a $200B+ machine with 90% global dominance, growing at 10%, and throwing off cash with 35%+ blended EBITDA margins. Show me a business with better numbers.

But the market isn’t pricing Google like it wants the cash flows. It’s pricing it like it fears the future.

I truly believe the market is overlooking what Google is actually doing -- integrating Gemini across its entire product suite, scaling TPUs internally, refining its AI agents quietly but relentlessly, and expanding its enterprise AI footprint with real velocity. This isn’t a company that got caught sleeping. It’s a company that got penalized for not shouting.

And because it didn’t scream loud enough, the market is now giving away core assets -- including the search engine that powers the global internet, still converting traffic better than anything on Earth -- for just 3x sales.

Meanwhile, DeepMind is building some of the most advanced frontier AI systems on the planet. Waymo is still the only autonomous vehicle platform with real traction in U.S. cities. The company is vertically integrating across hardware (TPUs), edge devices (Pixel), and enterprise (Workspace), while playing from a position of absolute financial strength.

But none of that is getting priced in. Because investors are modeling fear. They’re reacting to vibes. And for those with discipline -- those who understand that the best entry points often come wrapped in skepticism -- this is the kind of dislocation you wait for.

Eventually, the story will catch up to the substance. But by then, the price won’t.

Implied move for $HIMS is +-20% after the bell today.

My prediction is -12%. Literally nothing backing that number up but my gut. What do you guys think?

$META truly is a beautiful business model.

They have shown elite pricing power these last few quarters as they have continued to raise prices 10% YoY, which has contributed largely to their revenue growth.

They can justify the price increases due to more targeted and improved ads from their AI developments.

I can see them continue to raise prices at least 5% for years to come

ChatGPT came out November 2022 by the way.

Continue to say $GOOGL $GOOG will be affected by LLMs when they are as good at product driven queries as Google Search. If they do, Gemini is well positioned to be that leader.

For now, the search business remains safe and strong

$GOOGL $GOOG earnings today.

The main thing investors will be looking for:

- How have they been able to monetize their AI features (AI mode & overview)

- When and what kind of ROI can we expect on their heavy CAPEX that spooked investors last time around?

- Google Cloud Progress

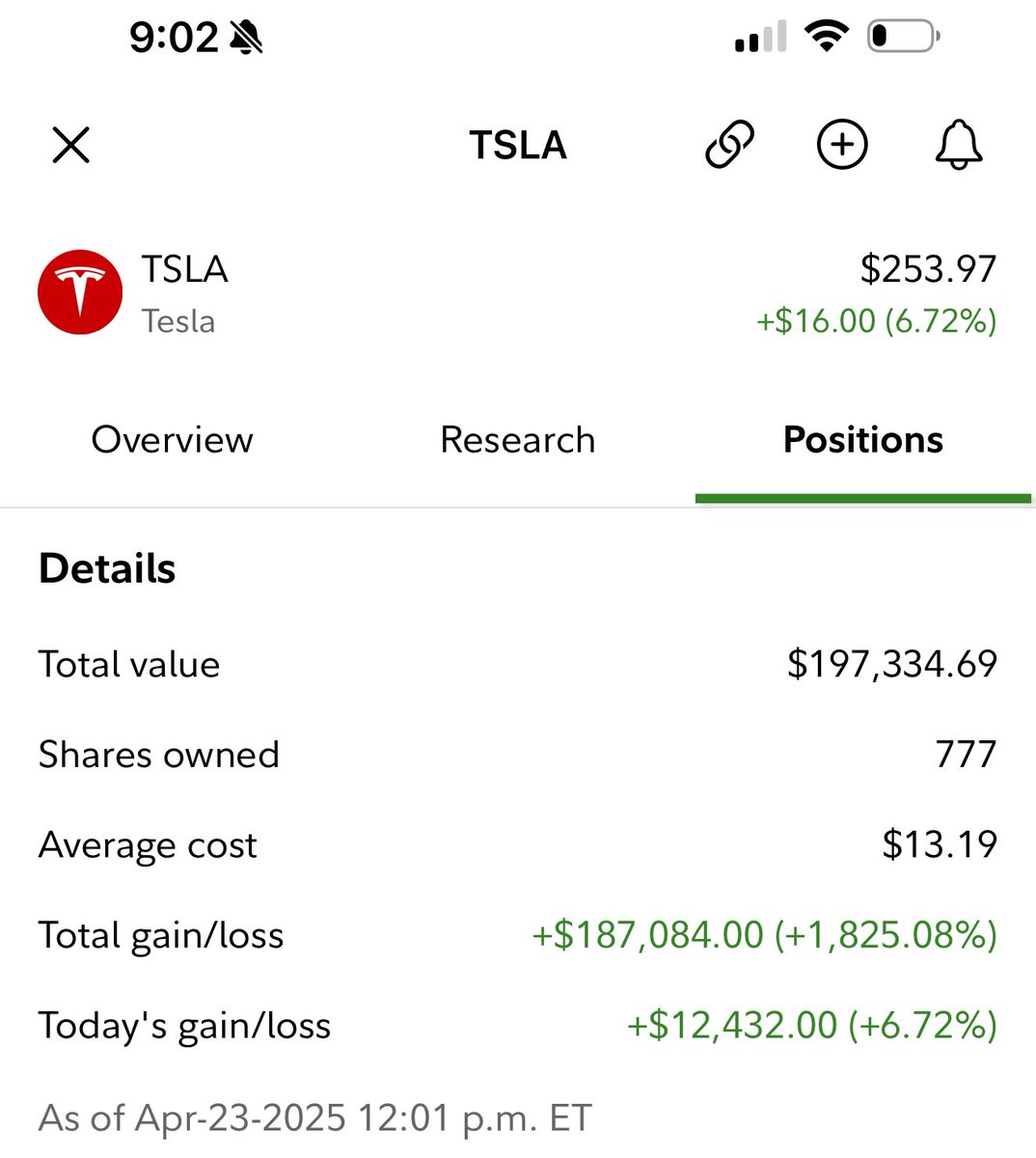

Jeremy’s getting a lot of flack for selling $TSLA right now. People are telling him to wait for the robotaxi rollout at the very least.

IMO that stuff is already well priced into the stock. With how the car business is struggling the stock should be much lower, but the hope for the future keeps it afloat.

You make the decision that seems the best to you at a current point in time and that’s what Jeremy did. Can’t hate on that.

Another buy the dip situation in the market for me.

Continuing to add to $PYPL $HIMS $META $AMZN, as those are some of the best risk-reward opportunities in the market right now.

What's everyone else been buying?

Yeah I make that point later in the thread I referenced. Right now LLMs aren’t better than $GOOGL at those kind of searches but yes they can become better.

If they do become better, who better than $GOOGL with their existing ad network, data, and pricing system to capitalize on that?