Management of a logistics company and a market favourite in 2022 estimated that the useful life of its vehicles is 3.86 yrs as opposed to 8 years as per Schedule II. Plant and machinery was 5 yrs as opposed to 10 yrs. Reflects true reality of the business. 1/2

@Prashanth_Krish The operating word is "Beginning". To paraphrase Chuck Prince the music is still playing quite loudly but the ppl are starting to get tired.

I m sure you will be able to list out multiple companies where the accounting/ narrative is quite aggressive to hold onto market caps.

The tide is beginning to go out and we are beginning to see those who are swimming naked.

The funny part is, most people always knew who forgot their trunks - they were hoping that the high tide would last forever.

It is a quasi borrowing structure for airlines taking additional debt from the govt with the OMCs as the conduit as opposed to borrowing it from banks.

Either ways the burden has now shifted from the OMCs to the airlines and the govt largesse is over. 2/2

Airlines have two options.

1) Take pain now at mkt driven prices and enjoy benefits when prices drop.

2) Defer the pain with govt funding the OMCs for now & when prices drop airlines will bear additional cost and return money to govt thru OMCs.

1/2

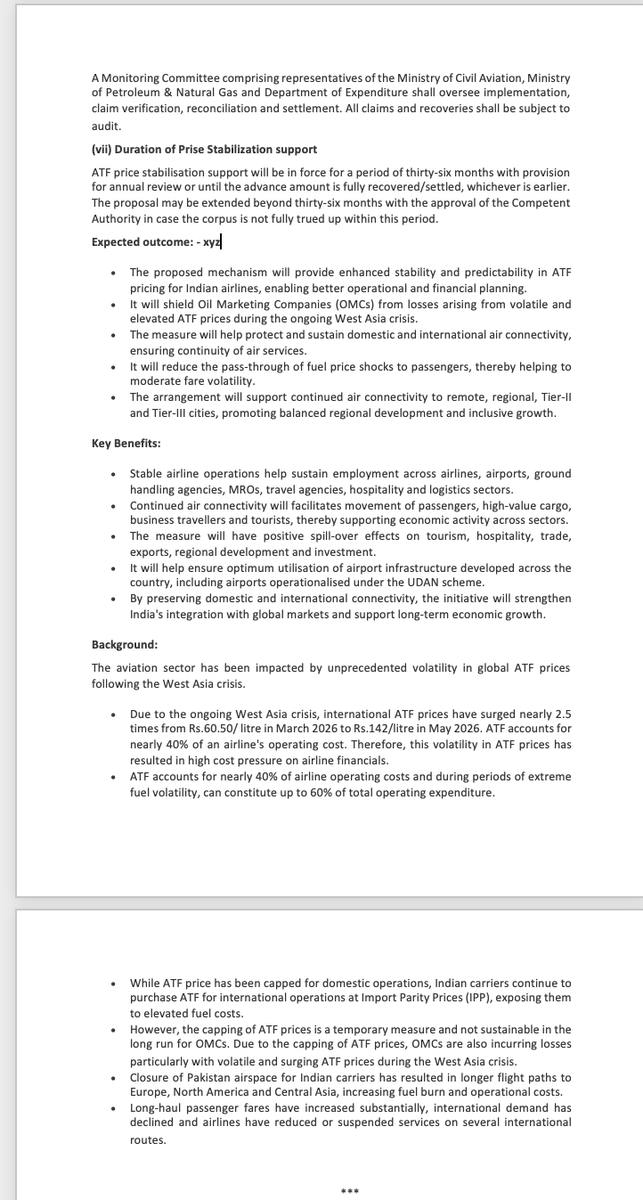

CABINET APPROVES ATF STABILISATION FUND

The government's move to create a price stabilisation fund for scheduled Indian airlines towards ATF pricing is a very welcome step; it will bring some stability against the rampaging ATF prices that we have witnessed, especially on the International sectors, due to the West Asia crisis.

This ATF fund will protect the OMCs against the vagaries of rising costs of ATF and is in the form of a repayable one-time advance to the OMCs, which will be passed on to airlines who want to participate in the scheme. As per Mr.Ashwani Vaishnavs statement, it is also intended to cover Airlines impacted by the Closure of Pakistani Airspace, and that is a welcome step, to restore some sanity in International fares.

The stabilisation price for ATF of Rs. 75.60 is a huge step and will be welcomed by all domestic and international operators, as we had seen that open market prices were applicable for international flights and those had risen as high as Rs. 145 per litre.

This ATF fund is a temporary measure for 36 months and is on a repayable basis by the OMCs and will depend on a case-by-case basis, as per MOUs to be signed with the airline companies that wish to participate.

Our view of 3 months ago was that Indian Airlines would suffer for the next two quarters due to the overarching impact of the Pakistani airspace closure, the West Asian crisis, Oil Price spike, the increase in insurance premiums and operating costs, longer routes, additional ground halts and the softening of international demand due to war. The first green shoots that we will see can only be in Q3, or if the the oil price ends right away, then perhaps during the Diwali-Xmas season.

Either way, Indian airlines need much more support from the government across the board.

I commend the Union Cabinet for taking such a step and actually bailing out the airlines, though it’s not enough to remove the strife we have seen in the aviation sector. It is a big step.

One does hope that the PM and Cabinet bring to bear on various states to rationalise ATF or bring it under GST, and that airport operators also rein in taxes, charges, CUTE, and PSF, etc., so that airlines can have an easier time and an expectation of reasonableness in operational costs across the board, and passenger airfares can be brought down to more reasonable limits and Fuel Surcharges removed.

@PMOIndia@narendramodi@MoCA_GoI@RamMNK@DGCAIndia@airindia@IndiGo6E@flyspicejet@AkasaAir@OfficialStarAir@mohol_murlidhar@samirsinha69

@Prashanth_Krish Its a valid business strategy which takes you to 65% mkt share, almost monopolistic power in most routes coupled with slot capturing. Having reached there, logically the end game should be super normal profits and pricing power. That seems to be elusive.

Eco 101 - Most industries, if unit revenue drops coupled with lower capacity utilisation, logical reasoning would be that there is excess capacity. Markets believes otherwise, ignoring that the monopolistic mkt leader is unable to pass on costs.

Indigo

The convenience of the first degree of thinking & why most analysts (writing off a one-time loss due to Dec disruptions) will prove horribly wrong.

While some analysts focus on IndiGo’s headline CASK decline (4.73 vs 4.83 YoY) as a sign of efficiency, a deeper look at the Q3 FY26 investor presentation reveals structural pressures that go far beyond one-offs.

Capacity expansion is proving more challenging than advantageous.

Key observations from the data:

Capacity grew strongly..

But unit revenue fell sharply. ASK (Available Seat Km) up 11.2% YoY (45.4 bn vs 40.8 bn), yet RASK (Revenue per Available Seat Km) declined 4.5% to INR 5.20 from 5.44.

Yield also dropped 1.8% to INR 5.33 from 5.43, and load factor eased 240 bps to 84.6%.

Revenue growth lagged capacity.

Revenue from operations..

Rose only 6.2% YoY, despite the 11% capacity increase. Other income grew 21.2%, but core operational revenue growth was muted.

Non-fuel costs ex-forex actually rose

CASK (Cost per Available Seat Km) ex-fuel ex-forex increased to INR 2.96 from 2.90 YoY.

This reflects INR depreciation (~ a 5.8% impact), contractual escalations (linked to labour & manufacturing-linked), and higher airport charges following privatisation (CAGR of ~12-18% across domestic & international airports).

Wide-body international expansion...

Adds pressure, with 16 wet-leased aircraft in total, including 7 wide-bodies (2 B777 and 5 B787). These operations are significantly impacting unit economics - new international routes via wet lease are a key contributor to the RASK decline.

Structural headwinds lie ahead as do mounting dollar liabilities (finance leases, sale & leaseback) with USD/INR now above 91.

Costs cannot be fully passed on in a low-fare environment model, and eventually, net revenue takes the hit.

New FDTL regulations will require more pilots; the demand-supply gap is pushing salaries higher, plus joining bonuses & ESOPs a recent addition to costs.

Upcoming London Heathrow flights (starting Feb 2026 from Delhi) will face longer routings due to Pakistan airspace closure, leading to higher fuel & operating costs.

Industry-wide context..

With>1,000 aircraft on order across IndiGo, Air India, and Akasa (50%+ deliveries in 2026–2030), supply growth will outpace demand if yields remain under pressure.

IndiGo has reached a massive scale with a huge order book, but sustaining profitability amid rising fixed costs, forex exposure, airport fee inflation, and risky low-cost wide-body international expansion will be the real test ahead.

Indigo still trades at nearly 4 times industry averages...

PE of over 40, while the global industry average is less than 10 PE

That this playbook that has been played in the past for very long periods of time, markets tend to have short memory of this playbook and how it crashed. 3/3

Regulatory capture and political benevolence is often mistaken for inherent competitive strength of a business. Markets more often than not in its warm glow ignore everything around including the fragility associated with it. 1/2

At the bottom of these pack of cards, is invariably the financial shenanigans, afterall organisations that cut corners have it written into their DNA. There are generally more cockroaches in the kitchen. 2/3

The silver lining in the Indian context, from the Trunp induced global reset and impending slowdown is that it will hopefully wake up the political establishment to carry out serious reforms.

As the old saying goes “ Never let a crisis go waste”.

We have lived in a world of higher weightage to ROCE and shareholder value. The Chinese have shown an effective alternate model. ROCE’s have lower weightage over other considerations.

We are moving slowly closer to a Bretton Woods moment. What form it will take and how to position the portfolio is going to require out of the box thinking, something beyond my pay grade.

1) A 25% haircut on dollar reserves for the world and the associated economic shock 1/2

2) US shifting its role from a benevolent dictator policing the world sea and trade to making the world pay for the security umbrella that it provides.

What form it will take is anybodys guess. Francis Fukuyama’s End of History might see a Fourth Turning. 2/2

INDIA'S FEDERATION OF AUTOMOBILE DEALERS ASSOCIATIONS (FADA) REPORTS THAT AUTO DEALERS ARE CAUTIOUSLY OPTIMISTIC ABOUT THEIR EXPECTATIONS FOR MARCH 2025.

Interesting titbit on Ray Dalio being labeled as the “Uncle of Chicken Nuggets” if not the father for his role in the creation of chicken nuggets😊.

There is also some side discussion on US debt 😜.

https://t.co/koF3r1drDP

Good conversation with Paul Singer of Elliot Investmemt. Some interesting thoughts on investing burnout and fatigue which we all experience at different points of time

https://t.co/RYf8w5CcIX