Learning how to emulate water will be the biggest catalyst for your growth that you’ll ever learn

Always moving. Always finding a way. Regardless of the variables.

Find your way through

HISTORY WILL REPEAT:

When Jerome Powell became the NEW FED CHAIR in February 2018, SPY crash 4%.

Kevin Warsh is the NEW FED CHAIR on May 15, 2026.

He does his first FOMC on June 17.

History shows the average max drawdown under a new Fed Chair is -20%.

SPY has NEVER been kind to regime change at the Fed.

For people who are worried about the market today, I get it. This stuff is very stressful.

So I put together a chart of all of the times the VIX (the "fear index" of the market) was up over 30% in a day (like today) in the past ten years.

23 out of 25 instances the market was higher one month later. The only two times it wasn't was Feb 2020 when Covid hit the economy in March 2020.

What is the underlying message? When people are afraid, they make bad decisions. Do the opposite.

Attached is a chart summarizing my results.

$onds this is from the March Q4 Conf call.

I’ll say it til I’m blue in the face. “World view is massively accretive”. Actually that’s the understatement of the year

We’re talking a program of record for Air Force. 250 flights. And golden dome. 200ish flights.

And so much more

1000s of flights a year. If the flights last 100 days (makes math easier) and we price at say $40,000 a day (likely higher) WV will generate $4 b in annual revs for EACH 1,000 balloons.

Wanna say $20,000 a day pricing. Then $2 B. Or $60,000/day then $6 B in annual revs

This is so nutty. If we’re talking $4 B annual WV revs in 5 plus years then WV is worth $20-40 B at 5-10x rev multiples. Too much? Fine. Haircut it all you want. And it’s still massive

Planet labs is probably best comp and trades way north or 20x revs as I posted recently

Accretion accretion accretion

$ONDS This is bullish

Quick explainer for those unfamiliar:

Options flow measures what traders are actually doing with their money in real time.

When it collapses during a selloff, it means panic i.e. traders pulling positions, buying protection, going defensive, etc.

When it holds steady, it means they are not concerned and they are staying positioned.

Last time $ONDS had a crash this size, flow collapsed to near zero and had to slowly rebuild back to 750,000 before the price recovered.

The panic had to fully play out before the bounce happened.

Today, flow never left 750,000 through the entire 14% drop.

Basically, flow didn’t flinch today.

The options market is already sitting at the exact level that preceded the last recovery without going through the “fear” cycle first.

Last time the market had to earn its way back, but this time, it stayed put.

The smart money looked at today’s drop and saw an opportunity.

That’s all you need to know 🤷♂️

The 7-second cold wrist rinse was tested on 3,000 soldiers after combat simulations.

Cortisol dropped 52% within 90 seconds. Heart rate fell an average of 22 beats per minute. The Navy classified the protocol in 2009 and kept it secret until 2023.

The mechanism is radial artery cooling. Your inner wrists have the thinnest skin and the largest surface-to-volume ratio for blood vessels. 7 seconds of cold water cools the blood passing to your brain, which signals your hypothalamus to downregulate stress instantly

You've splashed cold water on your face. You've taken cold showers. Both work, but they're inconvenient.

The SEAL protocol takes 7 seconds, requires no undressing, and can be done at any sink. Soldiers used it before night missions to fall asleep fast.

The military classified this because a free 7-second stress fix would reduce demand for combat stress medication ($400M annually).

The 2023 declassification came after a FOIA lawsuit filed by a veteran.

The fix: run cold tap water over your inner wrists for 7 seconds. Both wrists. Do it when you feel a stress spike.

Within 90 seconds, your heart rate will drop. No shower, no ice.

Just 7 seconds.

Taxes must be paid, but I am happy to have increased my position in Ondas by nearly 150% this year from 1.9M to 4.8M shares.

This reflects shares that I have both purchased (via the OAS exchange early this year) and now earned via RSU grants that vested this week, both net of tax considerations.

The shares I received this week where the first award I have earned since joining Ondas in 2017.

There is a lot more work ahead. 👊🏽

@YoYInvestor@OndasHoldings Absolutely agree. There’s a lot of noise in the market rn with it being so frothy, but what they’re building is loud and clear. The impact and ripple effect is imminent.

Nearly impossible to ignore..

Appreciate all of your articles brother. You’ve been crushing it

You are simply not bullish enough on the absolute titan being created with @OndasHoldings

Execute. Dominate. Win.

Empower. Inspire. Uplift.

Patience. Take a stride every day. Leverage your team.

Execute.

Dominate.

Win.

It’s time people start thinking way bigger about $ONDS could turn into.

This brand new investment cycle doesn’t end without the creation of enormous market capitalization.

Pay attention to the companies that are positioned ahead of the curve and already winning.

Not a single company in the world has the portfolio, talent, capital, global scale, and strategic partnerships that $ONDS has.

I will say it until I am blue in the face…

This is a monster in the making.

$ONDS today’s $4.8 mm 3 month contract with the navy is beyond incredible. Why? It is for one balloon. And $4.8 mm for 90 days is $53k per day pricing. So if this mission is extended in perpetuity (sure sounds like it will be) it would be $19.2 mm in revs for one coverage area.

Want some silly math? What if there are 1000 such coverage areas? Meaning 4000 3 month balloon missions. At $19.2 mm per annum that would equate to $19.2 B in annual revs

I know. I know. This is crazy talk. And not my expectation cuz ONDS would be a $1000 stock if so

But don’t forget WV CEO on Q4 call said he sees 1000s of missions per year. He specifically cited Air Force demand for 250 balloons . And golden dome for 100s

Anyway looking more and more like world view by itself will contribute north of $1 B a year in revenues in say 5 years

And world view could be worth over $10 B by itself. Or over $20 bucks a share Plus sentrycs at $2 B ish ($4) plus everything else, plus other amazing massive accretive deals teed up and ready to go

The party is just starting

Soon the market will understand the world view math. When it does, Katy bar the door

I don’t mean to short change any of the other amazing ONDS units by focusing on WV. But WV is one massive market inefficiency staring us in the face

I wonder what the clown who claims horrendous capital raise would think of the WV deal which was enabled by the capital raise he stupidly calls horrendous. Hmmm. Horrendous analysis I say

Buying WV for $150 mm and likely seeing its value skyrocket to $10 B plus is my kind of accretion all day long

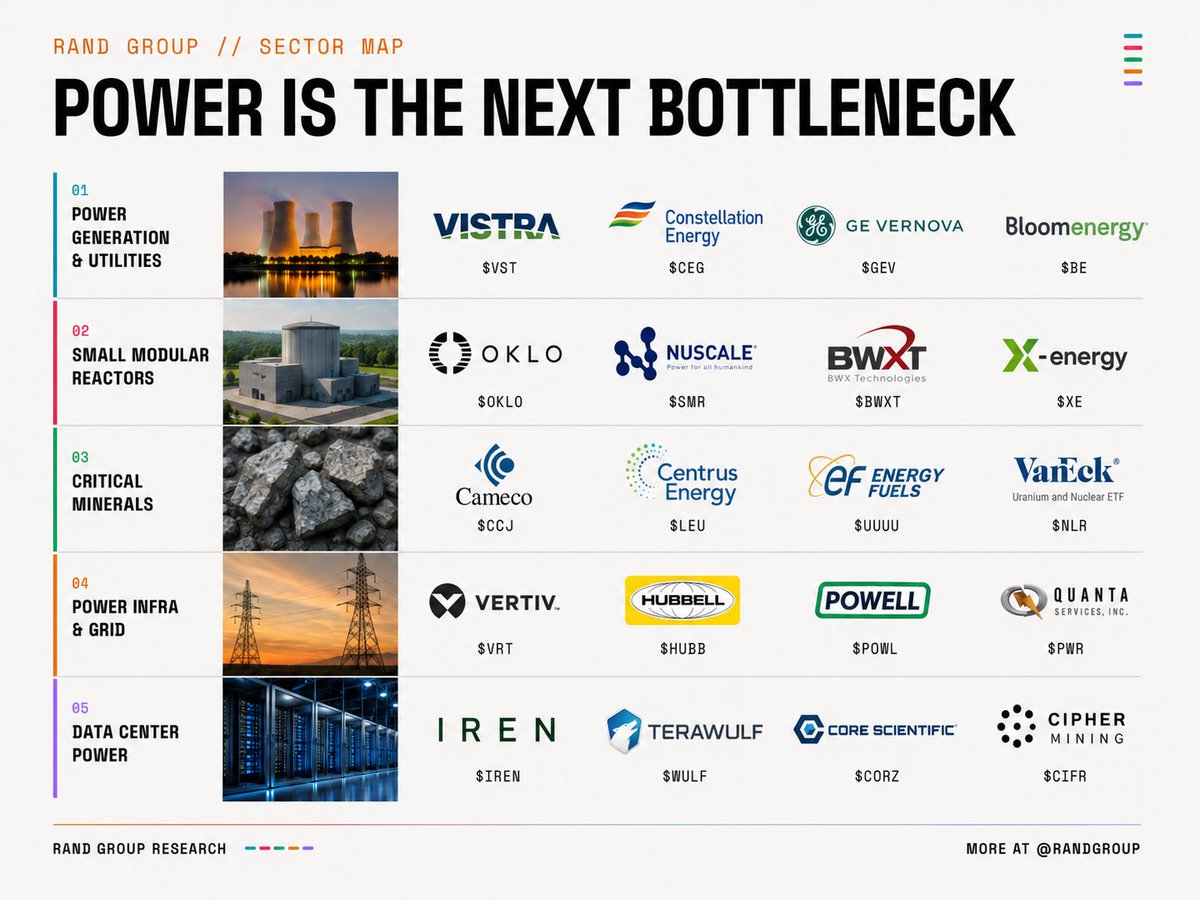

Every hedge fund I respect is suddenly talking about the same thing, and... it is not the chips.

It is the one bottleneck that breaks the entire AI story if it is not solved. Around 20 public companies sit on it. I put them all in one map across 5 layers.

Let's dive into it 🧵

Here is the thing nobody priced in two years ago. We spent a decade with flat electricity demand in this country. Utilities planned around it. Then AI showed up asking for gigawatts at a time.

The Electric Power Research Institute now thinks data centers could eat 9% to 17% of all US electricity by 2030, up from roughly 4% in 2023. Former Google CEO Eric Schmidt told Congress the sector may need 67 more gigawatts by the end of the decade. That is not a tweak to the demand curve. That is a new industrial revolution landing on a grid built for a different century. Every company below sits somewhere between a power plant and a server rack. This is the map.

🔌 POWER GENERATION & UTILITIES

Start at the source. These are the companies that actually make the electrons. For years this was the most boring corner of the market: regulated returns, slow growth, dividend investors only. Then the hyperscalers started signing power contracts directly with generators, and the whole category repriced.

$VST Vistra

This is the one I watch most closely in the group. Vistra signed Meta to a power purchase agreement for roughly 2,600 megawatts at its PJM nuclear sites, which tells you everything about where this is going: tech giants are now buying nuclear output directly. Q1 2026 adjusted EBITDA hit a record for a first quarter at $1.494 billion. They have hedged almost all of their 2026 generation, and they have bought back about 30% of the company since late 2021. A generator that trades like a buyback machine with an AI tailwind bolted on.

$CEG Constellation Energy

The largest nuclear fleet in the country, and the company that put nuclear back on the front page when it agreed to restart Three Mile Island for Microsoft. In January it closed the $21.8 billion Calpine acquisition, adding around 23 gigawatts of mostly gas and renewable capacity, and Q1 2026 revenue more than doubled the year before to $11.1 billion. The thesis is simple: when an AI company wants carbon free baseload power tomorrow, there are very few phone numbers to call, and this is one of them.

$GEV GE Vernova

If you only own one name in this entire map, my honest take is that it should probably be this one. GE Vernova makes the gas turbines and the grid equipment, the literal picks and shovels of the buildout. In a single quarter its Electrification segment booked $2.4 billion in data center equipment orders, more than it booked in all of 2025. Total backlog sits around $163 billion and management pulled forward its $200 billion target to 2027. The gas turbine backlog jumped from 83 to 100 gigawatts in one quarter, and they are raising prices into that demand. This is the cleanest expression of the trade.

$BEPC Brookfield Renewable

Note the ticker: this is Brookfield Renewable, $BEPC, not the $BE on most charts (that is Bloom Energy). Brookfield operates about 47 gigawatts and is developing a pipeline north of 200. It signed a framework with Microsoft to deliver over 10 gigawatts, roughly eight times the size of the largest single corporate power deal ever signed before it, plus a multi gigawatt hydro deal with Google. It also owns about half of Westinghouse alongside Cameco. The patient, contracted, dividend paying way to play the same wave.

⚛️ SMALL MODULAR REACTORS

Now the speculative end. The promise here is clean, firm baseload power in a compact box you can site right beside a data center. The catch: almost none of these are producing commercial power at scale yet, so you are buying a timeline as much as a company. Price that carefully.

$OKLO Oklo

The most exciting and the most expensive name in the room. In May the NRC approved the principal design criteria for Oklo's Aurora powerhouse in under half the usual review time, a real regulatory step forward. The customer pipeline is around 14 gigawatts, anchored by a 12 gigawatt agreement with Switch and a 500 megawatt deal with Equinix, and it added a research partnership with NVIDIA and Los Alamos. Just remember Oklo plans to build, own and operate its reactors and has essentially no revenue yet. This is a call option on a 2028 plus story.

$SMR NuScale Power

The one with the regulatory lead. NuScale has NRC design approval for both its 50 and 77 megawatt modules, which genuinely derisks deployment. It is sitting on about $1.2 billion in liquidity and is working toward a definitive power agreement with TVA through its ENTRA1 partner, with its first project tied to RoPower in Romania. Revenue was a rounding error last quarter because the licensing work wrapped up, so this is still a story about getting the first units in the ground.

$BWXT BWX Technologies

The adult in the room, and the name I would own if I wanted nuclear exposure without buying a lottery ticket. BWXT actually makes money: Q1 2026 revenue of $860 million and net income of $91 million, and it raised full year guidance. It builds reactors for the US Navy, produces medical isotopes, and just acquired Precision Components Group to push into commercial nuclear manufacturing. While the SMR startups sell the future, this one sells into it today.

$XE X-energy

Brand new to the public market. X-energy IPO'd on April 24 at $23 a share, raised about $1.02 billion, and came out around a $12 billion valuation with Amazon as its anchor backer holding nearly a third of the company before the listing. It pairs an 80 megawatt reactor design with its own proprietary TRISO fuel, and its order book already tops 11 gigawatts including Amazon's commitment to as much as 5 gigawatts by 2039, plus Dow and Centrica. Reality check: it lost about $390 million on $109 million of revenue in 2025, and first deployments are not expected until the early 2030s.

⛏️ CRITICAL MINERALS

You can build every reactor on the list above and they are paperweights without fuel. This is the front end of the cycle: mining, enrichment, conversion, and the magnet metals the whole grid runs on. Quick note: I swapped the misfiled Northland slot for Energy Fuels here, which is a genuine US critical minerals producer.

$CCJ Cameco

The blue chip of the uranium world. Q1 2026 net earnings jumped 87% and adjusted EBITDA rose 44% to $509 million on stronger prices and volumes. The kicker is Westinghouse: Cameco owns roughly half of it alongside Brookfield, so it captures both the fuel and the reactor technology side of the renaissance. When people want uranium exposure without a science project, they buy this.

$LEU Centrus Energy

The reshoring play, and a fascinating one. Centrus is the only production ready uranium enricher in America, sitting on a $2.3 billion enrichment backlog, a $900 million HALEU award from the Department of Energy, and a notice from the NNSA that it intends to sole source enrichment work to them. It is pouring over $560 million into its Oak Ridge centrifuge factory and is even exploring a fuel joint venture with Oklo. This is a national security story wearing a stock ticker.

$UUUU Energy Fuels

This is what $UUUU actually is. Energy Fuels runs White Mesa, the only conventional uranium mill operating in the United States, and it is the rare company licensed to produce both uranium and separated rare earth oxides under one roof. Its 2026 uranium guidance implies growth of 50% to 150%, and it is now turning out the dysprosium, terbium and magnet metals that everything from EV motors to grid hardware depends on. Uranium and rare earths, the two supply chains Washington is most desperate to pull back from China, in one company.

$NLR VanEck Uranium and Nuclear ETF

If you would rather own the whole theme in one line instead of picking a winner, this is the basket. $NLR holds the nuclear value chain end to end: reactors, enrichers, miners and the utilities running the plants. A lot of this very map sits inside it, with Constellation, Cameco, Centrus, BWXT and Energy Fuels all among its largest positions. The lazy way to be right about the sector even if you pick the wrong individual stock.

🔧 POWER INFRA & GRID

Between the power plant and the server rack is the least glamorous and maybe most investable layer of all. Transformers, switchgear, cooling, and the crews who build it. The dirty secret of the AI buildout is that the grid itself is the bottleneck. Interconnection queues run years, and the equipment to connect anything is on backorder.

$VRT Vertiv

The purest grid adjacent winner so far. Q1 2026 sales rose 30% to $2.65 billion, with the Americas up 44% on data center demand, earnings per share up triple digits, and guidance raised twice in two quarters. Vertiv makes the power and thermal systems that keep a data center alive, and it just joined the S&P 500. When the chip names sneeze, this one catches it, but the order book keeps validating the story.

$HUBB Hubbell

Boring on purpose, and that is the point. Hubbell makes the electrical and utility hardware, the transformers, metering and grid components, that every new data center and every grid upgrade quietly requires. It will never 10x in a year, but it sells into both the AI buildout and the broader grid replacement cycle at the same time. This is the ballast in the basket.

$POWL Powell Industries

My favorite quiet story in this section. Powell makes custom electrical equipment for utilities, energy and now data centers, and the demand signal is screaming: orders up 97% last quarter, a record $1.8 billion backlog, and right after the quarter closed it landed a single data center order worth more than $400 million, the largest in its history. It did a three for one split this spring and carries no debt. A small cap industrial running into a structural tailwind.

$PWR Quanta Services

The labor. Quanta physically builds and upgrades the grid, the part of this problem that no software fixes. Q1 2026 revenue rose 26% to $7.87 billion and its backlog hit a record $48.5 billion. If all of the generation and transmission above actually gets built, a meaningful slice of it gets built by crews like these. The pick and shovel play on the wires themselves.

🖥️ DATA CENTER POWER

The wild card, and the highest beta corner of the map. These started as bitcoin miners, which means they already owned the one thing everyone now wants: large blocks of interconnected power and the land around it. They pivoted to hosting AI compute, signing leases with the hyperscalers and the neoclouds. Enormous growth, real execution, and serious single customer risk. Size accordingly.

$IREN IREN

The furthest along. Formerly Iris Energy, IREN has a Microsoft AI cloud partnership worth billions, a power pipeline around 4.5 gigawatts, and high performance computing on track to make up the majority of its revenue by the end of the year. It already trades like an infrastructure company rather than a miner, because increasingly that is what it is.

$WULF TeraWulf

TeraWulf describes itself as a power company that happens to build digital infrastructure, which I think is exactly the right framing for this whole row. It has locked in over $12.8 billion of contracted compute revenue through long term leases with the Google backed Fluidstack and Core42, anchored by its Lake Mariner site and scaling toward a gigawatt of power. Its leasing revenue more than doubled year over year. Controlled power, leased to AI, on a multiyear contract.

$CORZ Core Scientific

The contrarian one. CoreWeave tried to buy Core Scientific in an all stock deal, and in a rare moment of shareholder backbone, the holders voted it down in late 2025. So it stays public, and it kept the prize: roughly $10 billion or more of contracted revenue with CoreWeave across about 590 megawatts, while converting its old mining sites into AI colocation. You are betting the company creates more value alone than the buyout offered.

$CIFR Cipher Mining

The earliest stage of the pivot, rebranding toward AI as it goes. Cipher signed a hosting deal backed by Google's Fluidstack, with Google taking around a 5% stake, plus a 300 megawatt arrangement tied to AWS, building toward a contracted compute backlog around $9 billion. Highest risk, least proven, most torque if the leases convert to cash on schedule.

⚡️FINAL THOUGHTS

Step back from the tickers and a pattern jumps out. The market is paying up for the same insight at five different points on the same wire.

The stability lives at the bottom and the middle. Cameco, Hubbell, Quanta Services and BWX Technologies make money today and sell into a buildout that is contracted for years. They will not triple overnight, but they do not need a single thing to go right that has not already happened.

The growth lives at the edges. GE Vernova is the rare name that has both, scale and acceleration, which is why I keep coming back to it. The reactor startups and the former miners are where the imagination is, and also where the disappointment will be when timelines slip, because timelines always slip in nuclear and in construction.

The clearest read of all is that the AI story quietly handed the baton from the chip layer to the power layer, and most people are still watching the wrong race. You cannot run the model without the electrons, and the electrons are the scarce thing now.

I will say the obvious part out loud: this is a map, not advice. I am pointing at where the money is moving, not telling you what to buy. Do your own work on every one of these, especially the speculative names where a single contract or a single regulator can move the whole thesis.

If this saved you a week of research, do me a favor and bookmark it, then send it to the person in your group chat who only owns Nvidia. The power bottleneck is the second half of that trade.

$ONDS (weekly) — Breakout confirmed. First target is $16, and yes, $42 is the next one after that.

We may get a retest of the broken diagonal, and that's the cherry on top—also the spot where I'd add or start a position. Risk/reward from there is absolutely beautiful.

Looking solid so far after a solid period of consolidation.

Ondas’ @WorldViewSpace has been selected by U.S. Naval Forces SOUTHCOM / U.S. 4th Fleet and SMX as the high-altitude balloon provider for a $4.8M, 3‑month Maritime Domain Awareness mission in the SOUTHCOM AOR, supporting counter-narcotics and IUU fishing operations with stratospheric ISR coverage. $ONDS

https://t.co/rGkTgBync1

.@Adobe Photoshop and Premiere — rebuilt from the ground up for NVIDIA RTX Spark.

Up to 2x faster across AI, editing, coloring and effects. Full GPU acceleration. AI-native pipeline.

Coming soon.

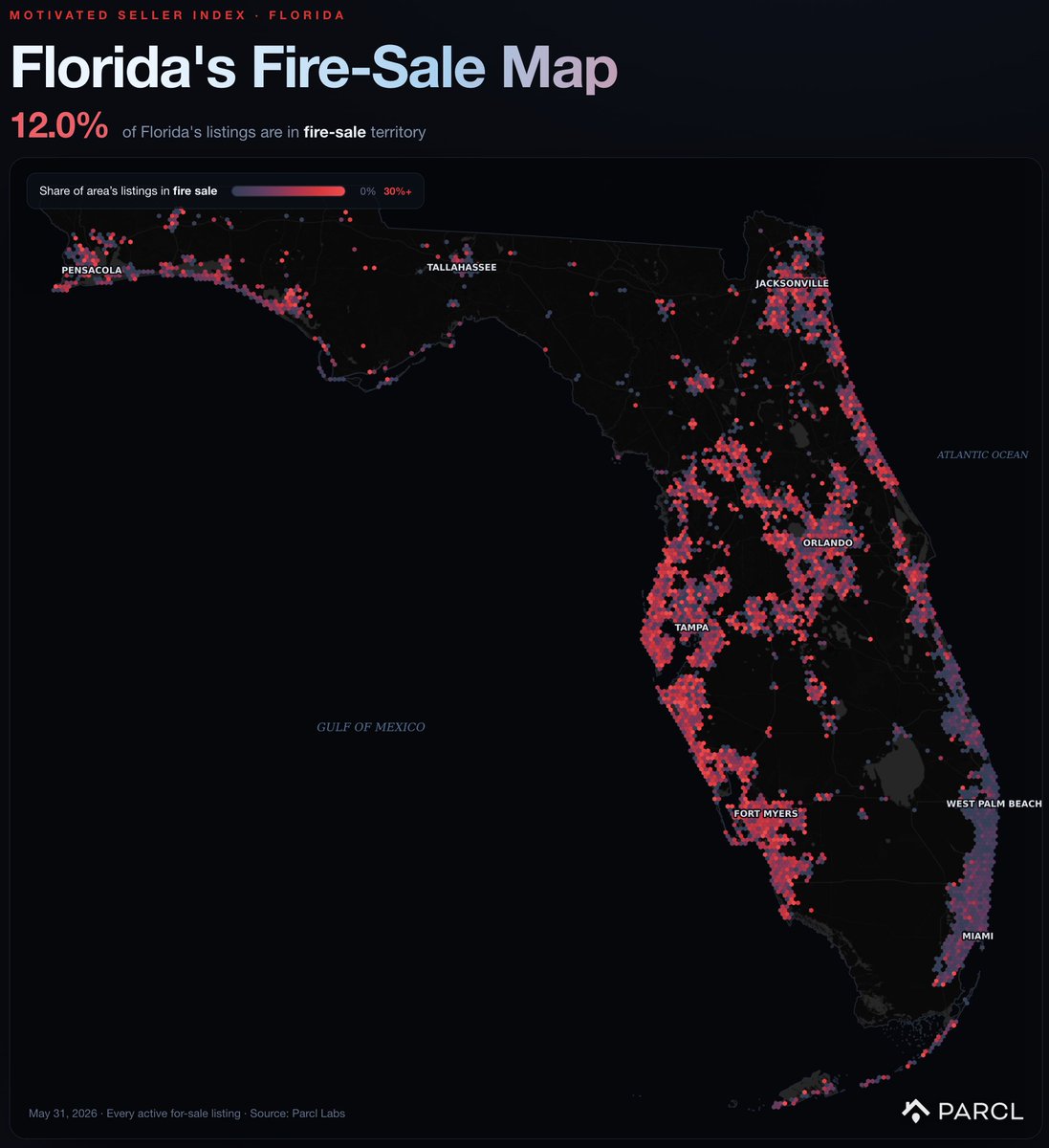

BREAKING - as of this morning, 12% of Florida's for sale homes are in active fire sale territory.

This means they have been sitting on market, the seller is actively cutting prices and increasing the frequency of those price cuts.

The pressure is mainly concentrated in Tampa and Fort Myers, where fire sales now top 30% of listings in some submarkets.

This means sellers cannot find buyers even though they want to.

"So @SimpleScanAI like an SEO tool?"

I get this question every week.

No.

And the difference is about to matter more than anything else in your marketing stack.

A thread by PROPS 🧵

One life tip —

If you’re all time red in your portfolio, and you’re in the mindset of looking to ‘make it back’, just stop.

If you’re trying to make something back, you’ll be in a constant state of psychological weakness and revenge trading.

Trading is literally a lifelong skill. If you get real good, your family, kids, and future generation could be set up forever.

People spend $100K + on University to get a job that will get displaced by AI.

Consider your losses in the market the cost of TUITION. The cost to learn and play the game.

And give yourself a clean, fresh, slate to start off from.

Trust me when I say this is an absolute must.

The more you try to make your losses back, the deeper your hole will become.