$SIF appears to be offering a massive info arb right now. the more I research this, the more excited I get. Top-line revenue numbers appear to be optically compressed too with some customers now starting to supply their own raw materials. The value of these materials is being completely excluded from the reported net sales in Q1, something that was not present in their earlier annual filings.

While this depresses headline revenue, it simultaneously reduces COGS, meaning the impact on gross profit is entirely neutral. If SIFCO had procured these materials themselves, their reported top-line for the quarter would have been noticeably higher. The quality of these earnings is vastly superior to what the market is currently pricing in.

Furthermore, management explicitly noted that their recent margin surge is being driven by a strategic shift in sales mix and the exit of lower-margin business. As this transition continues, don't be surprised to see SIFCO's numbers continue to inflect with structurally higher margins as Mr. Market finally catches up to the story.

Looking deep into $SIF (SIFCO Industries). It looks incredibly enticing optically with a highly relevant thematic tailwind and a great setup! Well positioned for the aerospace and defense recovery, driven by surging Boeing 737 MAX/787 production and record, stable F-35 contracts from Lockheed. The chart looks great with a low Float and Peter Abrahmson acquiring 6.4% of the float. The backlog is expanding rapidly and jumped $20 million from $119.2M at the end of Q4 2025 to $139.5M by Q1 2026.

Important to note that the earnings quality is high but is currently being masked by LIFO accounting; if FIFO had been used, inventory values would have been $11.1 million higher in Q1 2026, meaning the company's true earnings power is significantly depressed on paper.

Valuation appears cheap too with Enterprise Value below $100M. Given its recent return to profitability and a Q1 sales run-rate pacing near $96M annualized.

Could do really well here as throughput and margins continue to inflect!

$DUOT receives $50.4M from the sale of new APR Energy. Gives them good additional capital runway to execute. Pretty much the only pure-play modular data center company on the market.

The setup for $DUOT looks good from a risk/reward prespective as several massive catalysts start to converge. The biggest immediate one is the recent FTC filing confirming Elon Musk is acquiring the parent company of APR Energy. Since DUOS holds a 5% equity stake in that entity, this buyout could act as a massive value unlock driver.

Beyond the APR stake, the operational side is rapidly derisking as well. They have a $176 million contract locked in with Founders Fund-backed Hydra Host, and the $15 million prepayment is already sitting on the balance sheet. The management noted that this relationship is increasingly getting stronger. When you pair that with the news this morning that Armada just raised capital at a $2 billion valuation, the space is starting to get some eyeballs.

The stock is still highly speculative but has a compelling multi-thematic exposure across GPUaaS and Edge AI with the incredibly strategic asset of secured power in Tier 3 and 4 markets. The CEO's track record is strong and he also noted having open conversations with hyperscalers for a potential strategic investment, the stock could catch a bid.

$WATT CEO/CFO (a lot can be said about that) bought 1,867 shares today at $26.47. This was a widely followed name on here in Q1. Given the market backdrop, this could get interesting.

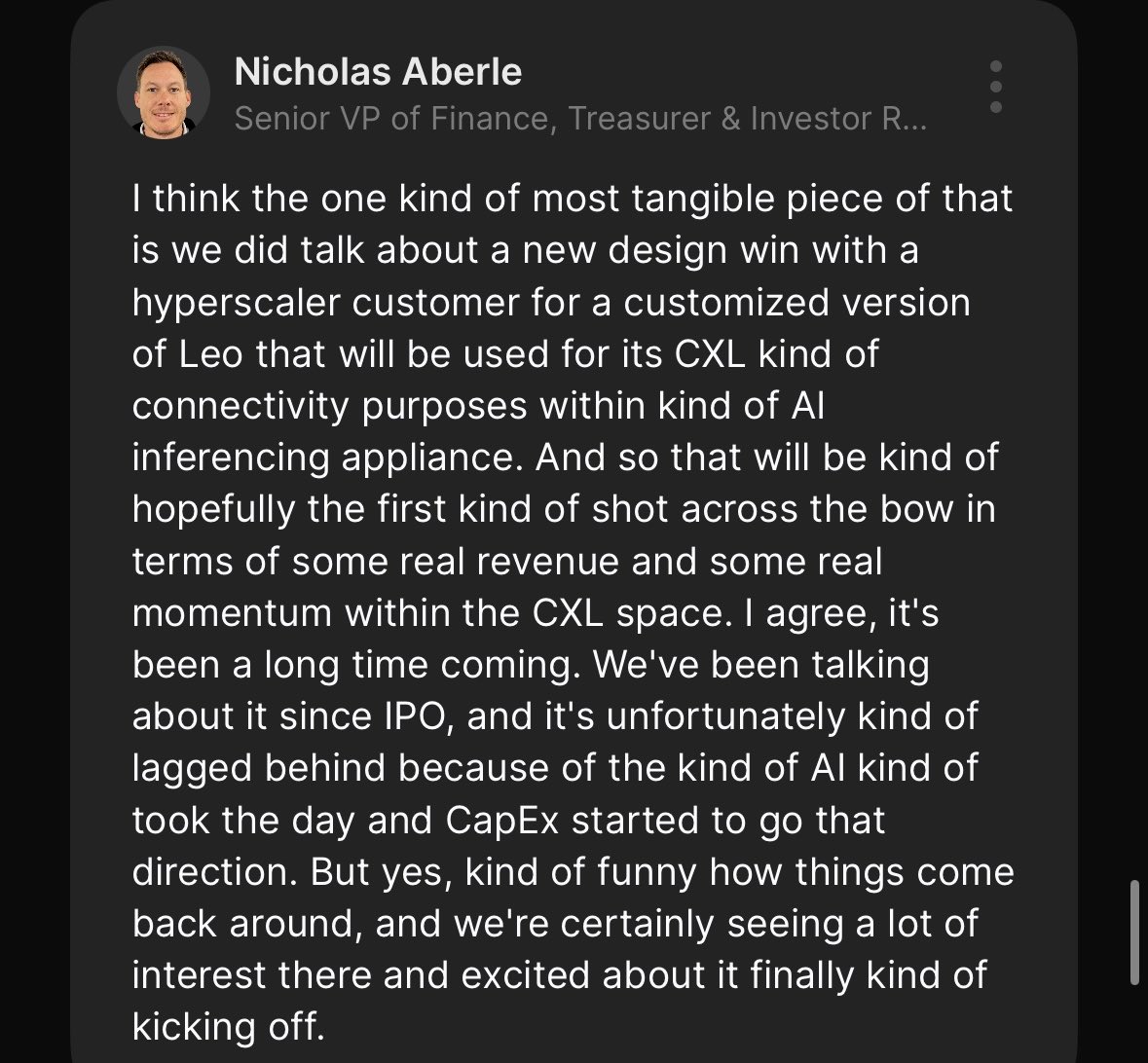

$ALAB talking about CXL in their TD Cowen presentation today. It’s clear everyone is increasingly looking to get the most from every penny spent on memory. CXL was part of conversations in 2025 but didn’t generate material revenue last year, though that is clearly changing. $PENG remains the absolute best way to play this theme.

@Venu_7_ $SHLS is also looking very good too. BESS optionality, cheap valuation, and with the factory relocation done, subsequent quarters should look better.

The setup for $DUOT looks good from a risk/reward prespective as several massive catalysts start to converge. The biggest immediate one is the recent FTC filing confirming Elon Musk is acquiring the parent company of APR Energy. Since DUOS holds a 5% equity stake in that entity, this buyout could act as a massive value unlock driver.

Beyond the APR stake, the operational side is rapidly derisking as well. They have a $176 million contract locked in with Founders Fund-backed Hydra Host, and the $15 million prepayment is already sitting on the balance sheet. The management noted that this relationship is increasingly getting stronger. When you pair that with the news this morning that Armada just raised capital at a $2 billion valuation, the space is starting to get some eyeballs.

The stock is still highly speculative but has a compelling multi-thematic exposure across GPUaaS and Edge AI with the incredibly strategic asset of secured power in Tier 3 and 4 markets. The CEO's track record is strong and he also noted having open conversations with hyperscalers for a potential strategic investment, the stock could catch a bid.

Back in $ZVIA after the call on Wednesday. We traded this very well in Q4 2024 and were lucky to take profits on time. The call was extremely encouraging and the company is showing signs of a real inflection here:

1. Revenue & Volume:

This was Zevia’s best quarter since going public as they recorded first quarter growth of 21%. The growth was entirely volume driven (20.4%) which is a great sign.

2. Channel Expansion:

They executed a successful national Costco rotation and saw acceleration in velocity at Walmart. The e-commerce business is also outperforming expectations. They have expanded in Kroger as well adding incremental flavors along with regional players like HEB and Publix. This quote was particularly interesting to me about Costco:

“The advantage of the national rotation… strengthens our velocities in the markets in which we have permanent distribution as well as helps to spur discussions about future rotations… the hope is that we would get another national rotation in the balance of the year.” — Amy Taylor

3. Cardi B Campaign upside:

This is arguably the most exciting social arb development. Zevia signed Cardi B as a brand ambassador who has the 25th most followed Instagram account. Thisc ould be a step change in reach and awareness for Zevia which they have lacked for years.

This awareness seems to be translating already as the management said that between Cardi B and other marketing programs during the month of March, Zevia saw its highest ever organic social media reach and the highest level of social media engagement of any month since the brand’s launch.

4. Profitability:

Adjusted net loss was just -$0.1M in Q1 2026, compared to -$4.2M a year ago. Selling and marketing as a % of net sales improved dramatically from 40.3% → 31.5%, demonstrating strong operating leverage as revenues scale.

5. The Setup for the Rest of 2026

Net sales guidance raised to 7% growth at midpoint, which I believe is being sandbagged massively after the impressive Q1 results. Q2 comps might be a little harder to lap but comps will get easier in Q3 and Q4.

TLDR: Q1 2026 represents a clear inflection driven by and record revenue growth, a near break-even EBITDA result, broad channel distribution gains, and the launch of the highest-reach marketing campaign in the company’s history. The packaging refresh is still rolling out and the Cardi B summer campaign hasn’t fully hit yet, meaning the biggest catalysts are still ahead. Low conviction position due to the chart looking ugly but risk/reward appears asymmetric

$ZVIA Investment Thesis: Asymmetric Upside Potential Amid Emerging Trends

After recent analysis, I’ve shifted my stance on Zevia, due to the October Amazon data showing a significant surge in e-commerce sales. While the upcoming Q3 results may still underperform based on September data, I believe the guidance could surprise positively, creating an asymmetric risk-reward scenario.

Analysis based on Amazon sales data estimates their Amazon sales for the past month around $2.5M, which annualizes to roughly $30M. Their e-commerce sales are generally around $3M/quarter. With e-commerce making up close to 9% of Zevia’s total sales, this implies total quarterly sales could approximate $75M, and on an annualized basis, reach $300M (currently @ $160M). Given this growth trajectory, an emerging company in the Stevia beverage category should conservatively trade at 2x revenue, putting the potential market cap around $600M—representing an 8x upside from current levels. There are a lot of assumptions in the calculation which are not perfect but the margin of safety looks good due to the potential upside.

Management has also mentioned a $12M cost-cutting initiative and hinted at a major distribution partnership announcement. Sentiment on TikTok is starting to build, with the Stevia-based product gaining popularity among health-conscious consumers, positioning Zevia to grow alongside competitors like Olipop and Poppi.

This is a speculative play due to liquidity concerns and a potentially weak quarter coming up, but I am initiating a 2% position based on the substantial upside. The stock has regained compliance, and any good news could lead to outsized rewards.

Keeping an eye on Dr. Zevia (healthy version of the #2 soda - Dr. Pepper, Caramel Soda and Root beer flavours which have been driving the sales.

Back in $ZVIA after the call on Wednesday. We traded this very well in Q4 2024 and were lucky to take profits on time. The call was extremely encouraging and the company is showing signs of a real inflection here:

1. Revenue & Volume:

This was Zevia’s best quarter since going public as they recorded first quarter growth of 21%. The growth was entirely volume driven (20.4%) which is a great sign.

2. Channel Expansion:

They executed a successful national Costco rotation and saw acceleration in velocity at Walmart. The e-commerce business is also outperforming expectations. They have expanded in Kroger as well adding incremental flavors along with regional players like HEB and Publix. This quote was particularly interesting to me about Costco:

“The advantage of the national rotation… strengthens our velocities in the markets in which we have permanent distribution as well as helps to spur discussions about future rotations… the hope is that we would get another national rotation in the balance of the year.” — Amy Taylor

3. Cardi B Campaign upside:

This is arguably the most exciting social arb development. Zevia signed Cardi B as a brand ambassador who has the 25th most followed Instagram account. Thisc ould be a step change in reach and awareness for Zevia which they have lacked for years.

This awareness seems to be translating already as the management said that between Cardi B and other marketing programs during the month of March, Zevia saw its highest ever organic social media reach and the highest level of social media engagement of any month since the brand’s launch.

4. Profitability:

Adjusted net loss was just -$0.1M in Q1 2026, compared to -$4.2M a year ago. Selling and marketing as a % of net sales improved dramatically from 40.3% → 31.5%, demonstrating strong operating leverage as revenues scale.

5. The Setup for the Rest of 2026

Net sales guidance raised to 7% growth at midpoint, which I believe is being sandbagged massively after the impressive Q1 results. Q2 comps might be a little harder to lap but comps will get easier in Q3 and Q4.

TLDR: Q1 2026 represents a clear inflection driven by and record revenue growth, a near break-even EBITDA result, broad channel distribution gains, and the launch of the highest-reach marketing campaign in the company’s history. The packaging refresh is still rolling out and the Cardi B summer campaign hasn’t fully hit yet, meaning the biggest catalysts are still ahead. Low conviction position due to the chart looking ugly but risk/reward appears asymmetric

The setup for $DUOT looks good from a risk/reward prespective as several massive catalysts start to converge. The biggest immediate one is the recent FTC filing confirming Elon Musk is acquiring the parent company of APR Energy. Since DUOS holds a 5% equity stake in that entity, this buyout could act as a massive value unlock driver.

Beyond the APR stake, the operational side is rapidly derisking as well. They have a $176 million contract locked in with Founders Fund-backed Hydra Host, and the $15 million prepayment is already sitting on the balance sheet. The management noted that this relationship is increasingly getting stronger. When you pair that with the news this morning that Armada just raised capital at a $2 billion valuation, the space is starting to get some eyeballs.

The stock is still highly speculative but has a compelling multi-thematic exposure across GPUaaS and Edge AI with the incredibly strategic asset of secured power in Tier 3 and 4 markets. The CEO's track record is strong and he also noted having open conversations with hyperscalers for a potential strategic investment, the stock could catch a bid.