With the May PPI and CPI in hand, forecasters expect core PCE to print around 0.35% in May.

This would raise the y/y rate to 3.4%. The six-month annualized rate would climb to 4.1%, the highest since June 2023.

Both measures were below 3% in the year-earlier period.

The AI revolution needs more funding:

Net equity issuances are estimated to rise to ~$200 billion in 2026 and surge +500% YoY in 2027, to ~$1.2 trillion, according to JP Morgan.

This includes IPOs, secondary offerings, and other share sales after accounting for buybacks.

Combined, this would be the largest 2-year period of net stock issuance since at least the late 1990s.

This marks a sharp reversal from ~$12 trillion of shares repurchased in the previous 20 years, shrinking the available stock supply consistently each year.

The surge is being driven by SpaceX's, $SPCX, $85.7 billion IPO, the largest in history, alongside upcoming mega IPOs from OpenAI and Anthropic.

At the same time, Alphabet, $GOOGL, Meta, $META, and Oracle, $ORCL, are expected to raise hundreds of billions in secondary share offerings to fund their AI spending plans.

We are about to witness a historic wave of US equity issuance.

BREAKING: US oil prices extend losses to -7% on the day, falling below $76/barrel, on news that the US-Iran deal is expected to include sanctions relief.

Hello @Pepperfry

could you please provide an ETA for the return pickup and refund of Order ID 310837552?

Additionally, I would appreciate an update on the status of the following cases/orders:

• CB-170626-0030

• CB-160626-0054

• EM-140626-0043

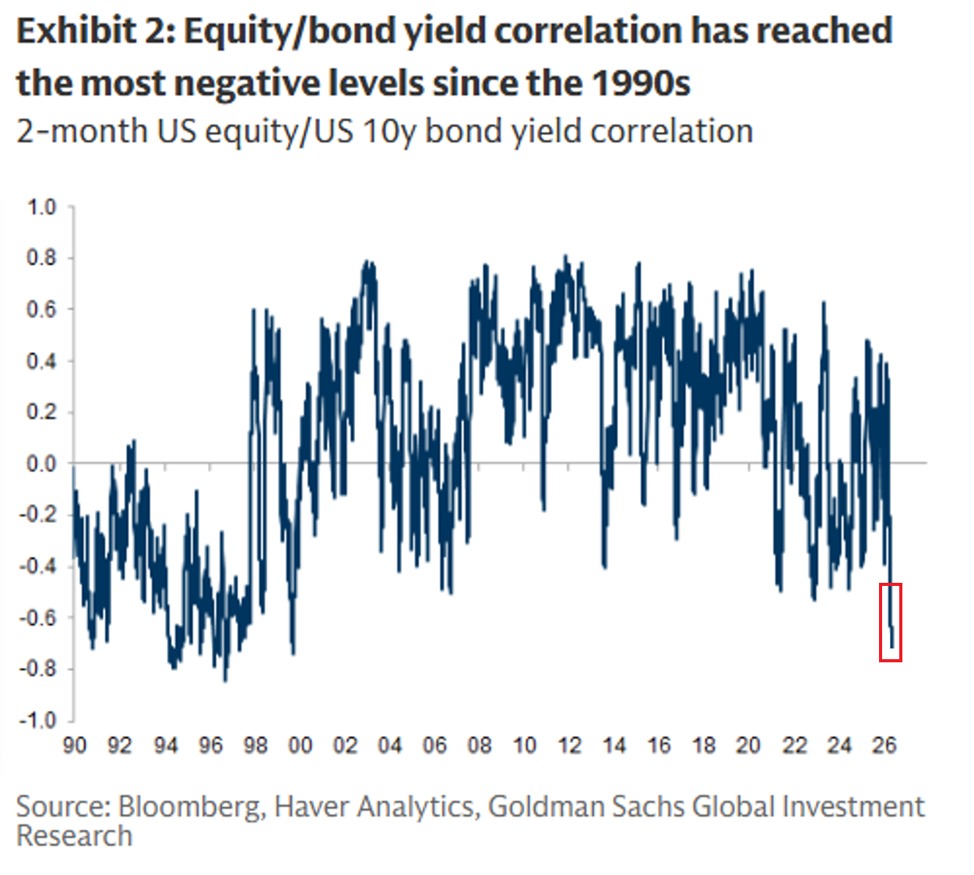

The stock-bond relationship is showing a rare pattern:

The 2-month correlation between US equities and the 10-year Treasury yield is down to -0.70, the lowest since 1999.

In other words, over the last 2 months, stocks and the 10-year Treasury yield have moved in opposite directions by the largest extent this century.

At the start of 2026, a positive correlation of 0.40 was observed, near the highest since 2023.

Additionally, the 30-day correlation is down to -0.68, also the lowest in 27 years.

Not even the 2022 bear market saw such a negative correlation, as the 10-year yield rose, driven by elevated inflation and Fed rate hikes, while stocks fell.

Bond markets are incredibly important right now.

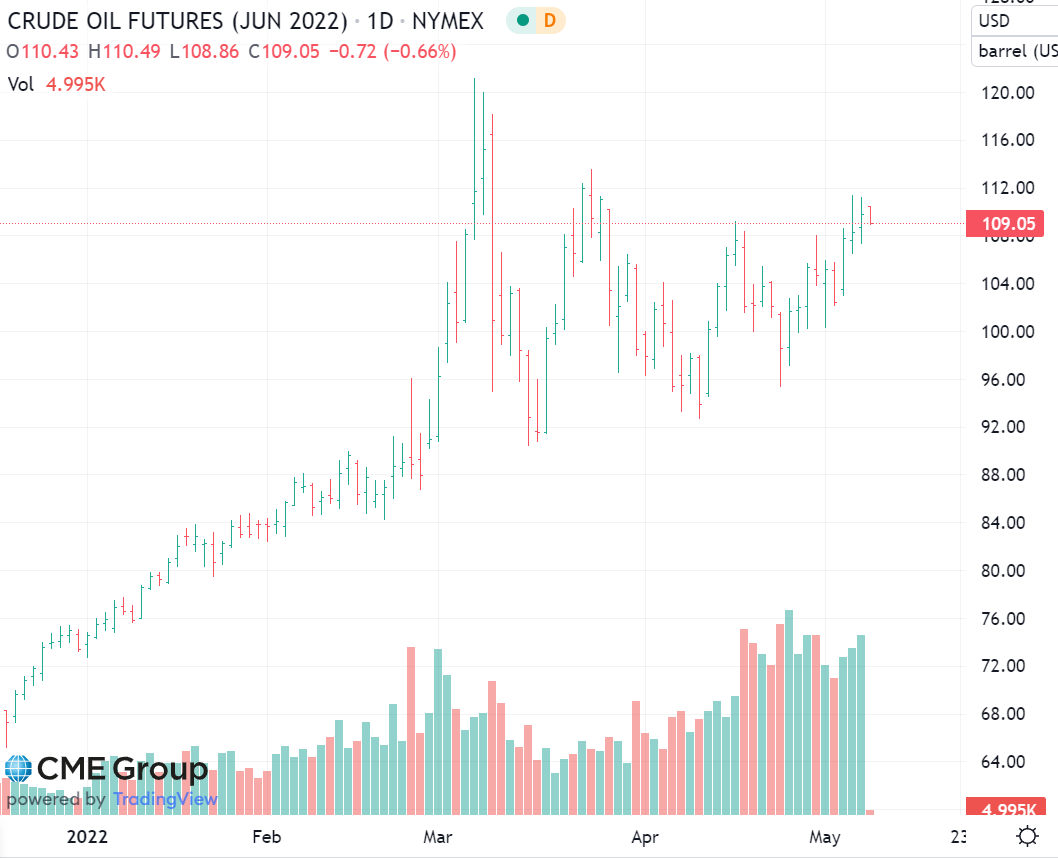

Aramco lowered light crude oil pricing by $2.50 for Europe and for Asia by $4.95. Left US pricing unchanged.

Oil price: down 0.6%.

WTI oil at $109 in the overnight market. The oil market is tight and doesn't seem to be responding to the Saudi price cut, despite China lockdown.

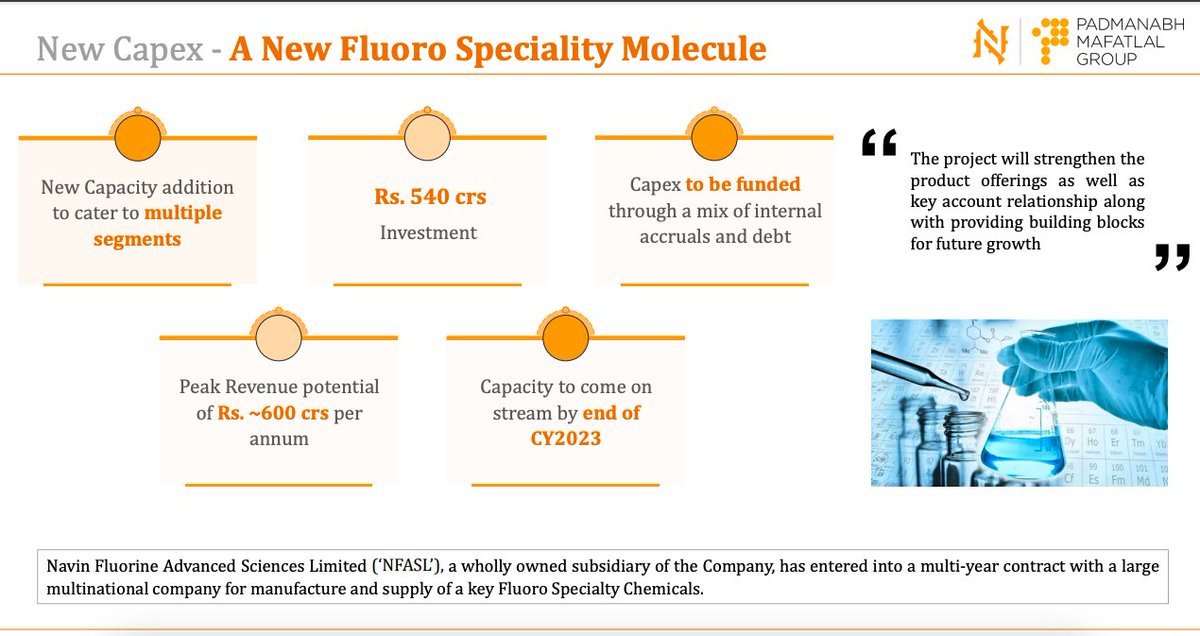

Another 540 crore capex announcement by Navin, this Q legacy mix increased leading to margin contraction as legacy is lower margin.

FY23:- 1300+ Crores of capex on a net block of 377 crores in FY22.

Tailwinds🏎️

BREAKING: RBI Governor Shaktikanta Das says it is necessary to be sensitive to new realities. India is not an island in this connected world. Announces repo rate hike by 40 bps to 4.0 percent with immediate effect.

Maersk's CEO says writing down all assets in Russia to zero.

🔸Congestion at ports has not eased in 1Q.

🔸Freight rates have come slightly off the peak.

🔸The impact of China lockdowns is mainly on the land-side.

#logistics#supplychain

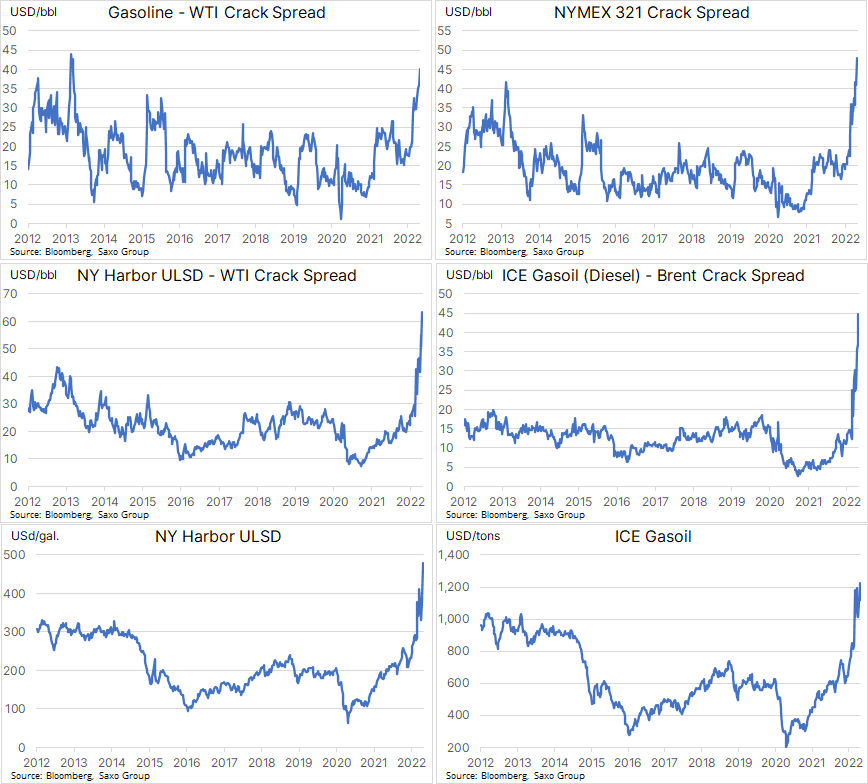

Demand destruction does not need #crudeoil above $150/b as the cost of fuel continues to rise, especially #diesel which trades at or near record levels in US and EU. With crude still rangebound, the crack spreads have soared. #OOTT