@Nale Save that time and money, and use it for mini family roadtrips or staycations every month or two instead. The memories will last for life…

Challenge your kids and have them learn to be competitive and establish teamwork skills in other ways.

An electrified AMG is an oxymoron that AMG enthusiasts do not want.

The Taycan and E-Tron RS were not successful launches for Porsche and Audi (respectively). Why would @MercedesBenz think otherwise on this?

Their EQS and EQC was also a complete flop. If anything that should have been “the winners”. Now they’ve doubled down on electric for their flagship performance line.

As for me “selling my own position”. One of our largest shareholders wanted to increase their position and I was staring at significant CRA bill for taxes owed on stock based compensation. Private sale, off market. I don’t see any red flags with this. The money for CRA has to come from somewhere. Hence why I’ve preferred to accrue it over the years along with a good chunk of my salary…

You may also not be aware, but I took no salary for the first two years.

If I was self-enriching, I definitely am doing a terrible job at it lol. I was bringing home about $1.5M per year after taxes before I started Avant/GTEC. I knew heading into this, there was no way in a decade I would make the equivalent ($15M).

Nice to see M&A activity picking up in the sector.

Safari is 59,000 sq ft, 6,000 KG per annum, had approximately $25M of debt, and sold for $26.5M.

For context, Avant produced double that in FY2025, currently $1.5M of debt. Albeit, Safari has EU-GMP. Still, the disconnect doesn't seem to make a whole lot of sense to me. I think Avant "being priced for bankruptcy" risk is off the table considering we only have $1.5M of debt now. But then again, maybe I am biased.

https://t.co/TBVzDN0Hw3

Actually it’s the opposite. Many on-going consultants and employees including myself, accrued part of our salaries, and bonuses that went as far back as 2022. We didn’t want to get paid until the company was flushed with cash.

However, was there was some pressure internally to get some of that off the books and clean it up. And of course, if we are asking staff and consultants to convert into shares, and our largest debt holder to convert debt into shares, surely I gotta lead by example and do the same.

Fun fact: all the stock based bonuses I’ve received throughout the past 5-years have actually cost me more in taxes due to CRA (that I have to pay with cash!), than the shares are worth today. Quite the opposite of self-enrichment. If I was here for self-enrichment, I woulda sold every single share at $1.00 (pre-consolidation) and sailed off into the sunset with $20M. But of course nobody talks about that 😑.

If that sentiment were accurate across the vast majority of our shareholders, then the share price should be absolutely cratering to $0.20.

But its not, because smart investors understand basic logic a 10-year old would understand. Lower production due to $2M of lighting upgrades... Short term pain, for long term gains. Higher yields, higher THC, higher quality, better smoke. And no, this isn't a theoretical pipedream because we are already using previous models of these lights at some of our other facilities.

Avant Brands Reports Q1 2026 Results Highlighted by 37% Growth in Recreational Revenue

Read the full release here: https://t.co/DtJ7WekGmj

#AvantBrands#AVNT#AVTBF

Avant Brands Announces Strategic Realignment of European Operations and Reclaims BLK MKT™ Brand Rights in Germany and Switzerland

Read the full release here: https://t.co/mqy6wvk30q

#AvantBrands#AVNT#AVTBF

Our debt load is very very realistic vs revenue profile at this point.

$2.68M unsecured convert, and $727,000 on the NFS credit facility.

And we just fully retired the $9.5M secured convert end of last year… remember when I stated on an earnings call that if we had any issues on the $9.5M convert, I would pick up the phone, call them and restructure it, and then I did exactly just that…

Debt can be a scary thing, but not if it’s with friendly groups, and a manageable amount. I think we have proven to shareholders that we are grown adults capable of managing and repaying our financial obligations. It’s time the market start treating us like one…

Our debt load is very very realistic vs revenue profile at this point.

$2.68M unsecured convert, and $727,000 on the NFS credit facility.

And we just fully retired the $9.5M secured convert end of last year… remember when I stated on an earnings call that if we had any issues on the $9.5M convert, I would pick up the phone, call them and restructure it, and then I did exactly just that…

Debt can be a scary thing, but not if it’s with friendly groups, and a manageable amount. I think we have proven to shareholders that we are grown adults capable of managing and repaying our financial obligations. It’s time the market start treating us like one…

How long are we going to be priced for bankruptcy, when are trending the opposite?

Retiring the $9.5M convert, which was SECURED against our real-estate is massive. Our largest monthly obligation, with security, GONE. POOF!

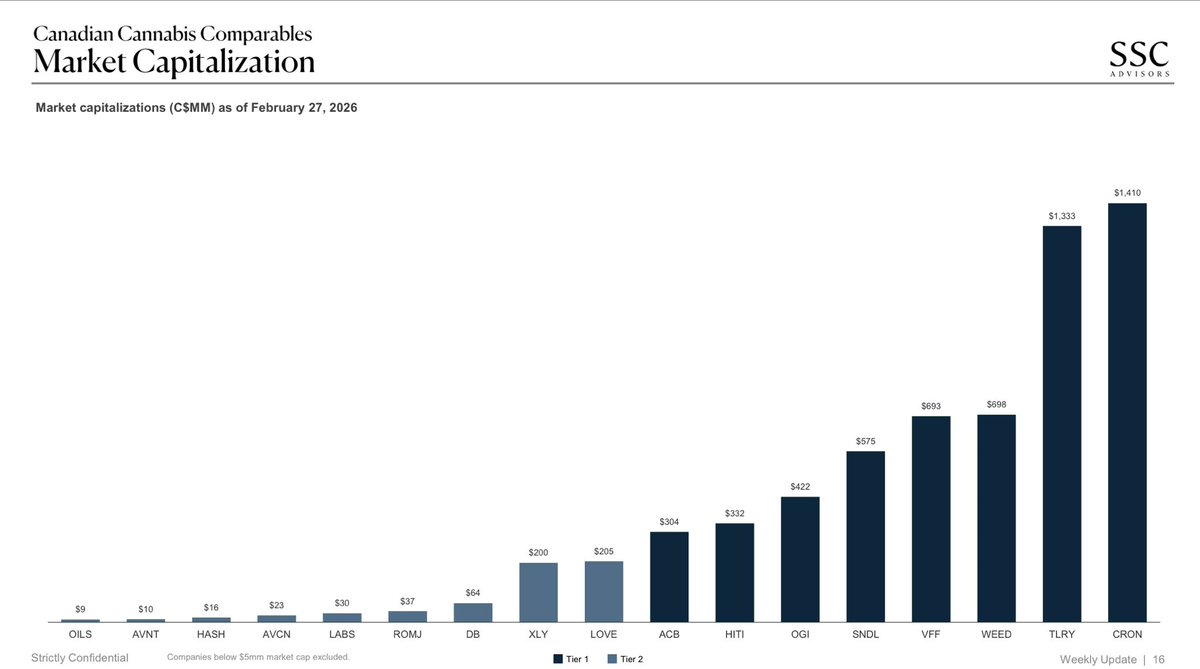

We are the second lowest market cap of all publicly traded LP's. It getting ridiculous, almost to the point where I suspect someone is purposely holding us down.

Avant Brands Reports Audited Fiscal 2025 Results with 19% Recreational Revenue Growth

▪️Record Operating Cash Flow: Generated $5.7 million in operating cash flow, up significantly from $0.5 million in FY 2024.

▪️Recreational Revenue Growth: Increased 19% to $14.8 million, driven by blk mkt™ and Tenzo™ brand momentum.

▪️Gross Profit Improvement: Achieved $4.6 million gross profit, reversing the $1.7 million gross loss in FY 2024.

▪️Positive Adjusted EBITDA: Delivered $2.1 million in Adjusted EBITDA, with positive results in three of four quarters.

Fiscal 2025 marked the moment Avant's operational discipline met its brand potential. We moved aggressively to optimize our cost structure, resulting in a record $5.7 million in operating cash flow and a significant gross profit improvement. Our ability to grow recreational revenue by 19% while the broader industry faced headwinds proves that our 'quality-first' strategy is winning. We've cleaned up the balance sheet, repaid approximately $4.5 million in debt, and fully retired our largest convertible debenture, positioning Avant as a leaner, stronger, and more profitable leader heading into 2026.

Avant Brands Reports Audited Fiscal 2025 Results with 19% Recreational Revenue Growth

Read the full release here: https://t.co/3wY3DJsMGZ

#AvantBrands#AVNT#AVTBF

@JoeRice1848726@canna_canadian@realjordancage I think the valuation collapse was part of the entire industry. From 5-year highs, Canopy is down 99.6%, Aurora 96%, Tilray 97%…. But you must be right, it’s gotta be the conference calls we stopped doing lol.