Having recently traded China A shares myself, my impression was that the market is far too easily moved, and even manipulated, by absurd rumors.

At the time, I held a leading Chinese CCL stock. One day, a rumor circulated that Chinese securities regulators were investigating a fund for allegedly manipulating CCL related stocks. As a result, a stock that had been up nearly 7% intraday quickly gave back all its gains and fell back to around flat.

But after local Chinese media looked into the matter, the rumor was found to be false.

A shares are far too vulnerable to rumors. I no longer trade China A shares.

China’s retail sales — a nominal figure — grew just 0.2% in April, marking the weakest reading on record outside the Covid era.

Investor pessimism about consumption has become deeply entrenched: the underperformance of consumer-oriented sectors relative to the broader market has now widened to the largest gap in history.

“Nobody wants to touch anything tied to consumption.” That is, broadly speaking, the prevailing sentiment among onshore investors.

Goldman tries to quantify the net effect of AI both substituting for and augmenting U.S. employment.

Their conclusion: AI substitution in occupations like phone operations and insurance claims administration have reduced monthly payroll gains by around -25K and raised the unemployment rate by 0.16 pp over the past year. AI augmentation in occupations including medicine and education have added +9K to monthly payrolls and lowered the unemployment rate by 0.06 pp. This nets out to a slight -16K drag on payrolls and an increase in the unemployment rate by 0.1 pp.

Caveat: This exercise doesn't account for the possible benefit from either construction hiring due to data-center buildout or AI-driven productivity/income gains.

Sharing a new piece by me and my colleague @shuizaiping2 where we took a deep dive into Xi Jinping’s newly released book on the “correct view of political performance”, a compilation of his speeches spanning more than a decade, many of them previously unpublished!

The timing, obviously, is no accident. Ahead of the Two Sessions, Beijing is clearly trying to push a shift beyond GDP worship and redefine what counts as bureaucratic success.

In fact Xi has long been frustrated with his bureacrats. He complained about officials who “rack up a mountain of debt, pat their butts, and walk away,” chasing short-term growth at long-term cost. He is equally frustrated with the cadres’ lack of motivation: “some officials won’t lift a finger until the Central Committee issues a written directive… Are you telling me that if I don’t personally issue a directive, the work just grinds to a halt?!”

So what’s the new, better KPI, according to Xi? Our takeaway: it’s a trilemma.

From Xi’s speeches, good cadres should be expected to deliver 3 things all at once: strict political loyalty / compliance; new + better quality growth through technological upgrading eg “new quality productive forces”; systemic security (avoiding risks + containing those accumulated over the past decade.)

The problem? Each of these priorities makes sense on its own. But together, they create a bureaucratic trilemma in which officials can realistically satisfy only two of the three.

Is there a way to escape the trilemma? We offer some thoughts...

"This has bedevilled the launch of a property tax, in part because many corrupt officials own several homes. Forcing political elites to come clean would expose pervasive graft—and trigger a pre-emptive wave of home sales when the property market is weak."

Observers fret that Xi Jinping is returning China to Marxism; few notice that, perhaps unwittingly, he has made it a partial tax haven https://t.co/AIwqCKjPt6

Xinhua: "Chinese local authorities have allocated 2.05 billion yuan in funds to directly benefit the public through the distribution of consumption vouchers, subsidies, and cash envelopes during the nine-day Spring Festival holiday." For what its worth, that is well under one-tenth of 1% of the country's 9-day GDP.

https://t.co/jD3zAGjr0x

This chart from the Financial Times illustrates the significant ongoing volatility in precious metals, as speculators have effectively sidelined institutional investors for the time being.

Gold is currently trading down 5%, while silver has slumped 10%.

The pressing question is how long this speculative shakeout will last—and just how much damage we should expect.

All we know for sure is that the extraordinary rise in the prices of both, while driven by fundamental factors, attracted lots of speculators.

Meanwhile, oil prices have also fallen, with Brent down 5%, following a slight cooling in the fundamentally tense relations between Iran and the US.

#economy #markets #oil #gold #silver @FT

TRUMP EYES WARSH FOR FED CHAIR

The Trump administration is preparing to nominate Kevin Warsh as the next Federal Reserve chair, according to people familiar with the matter.

President Trump said he will announce his pick Friday morning, though the decision is not final. The White House and Warsh have not commented.

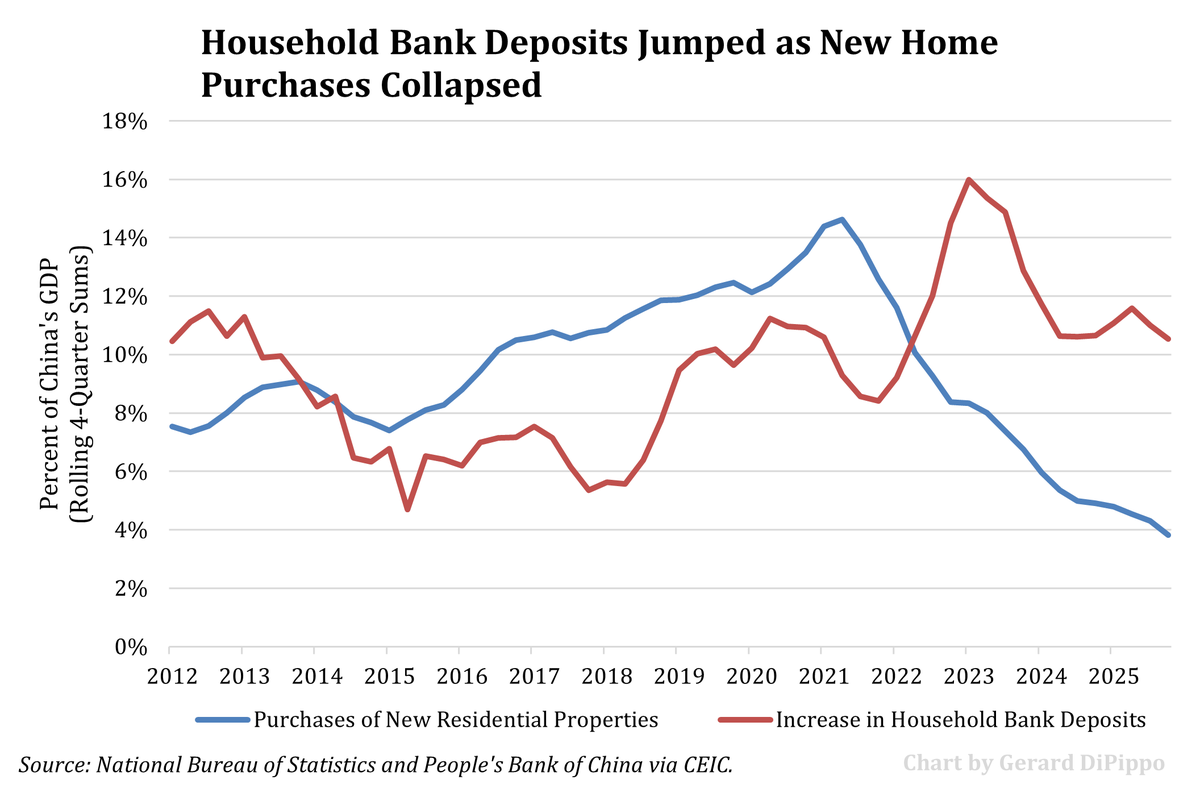

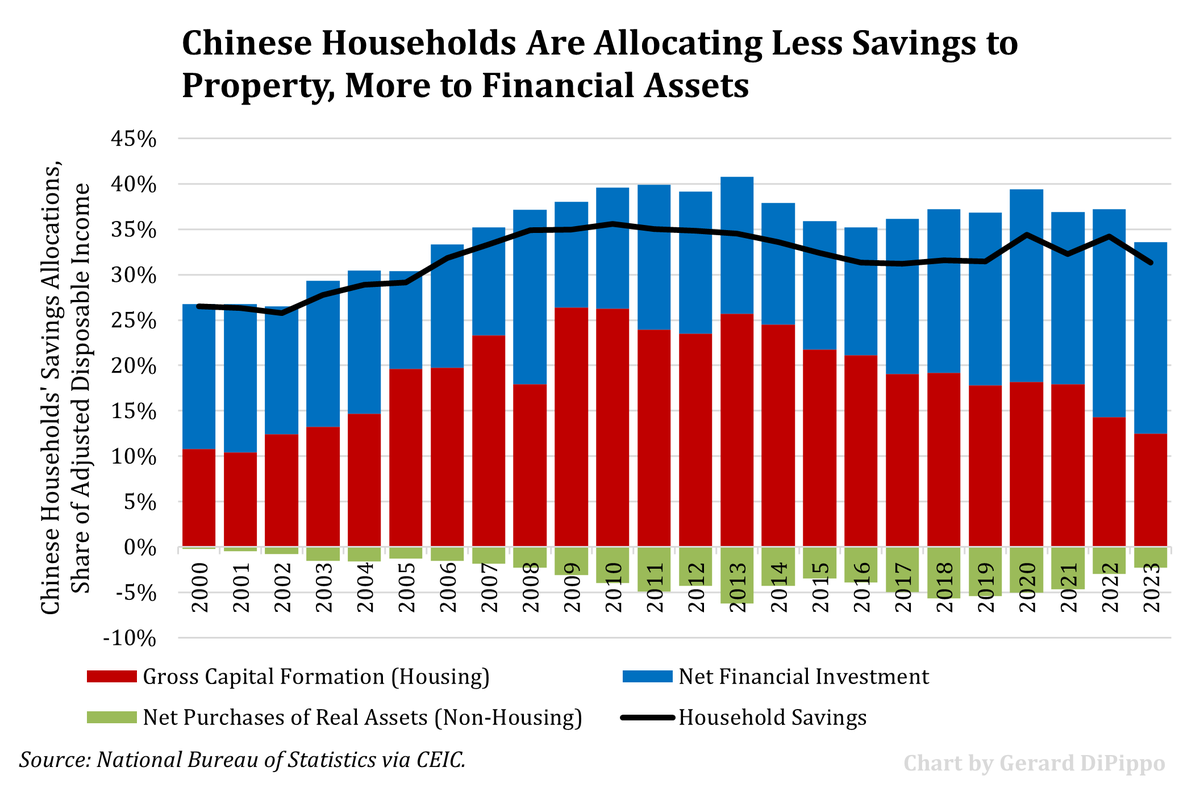

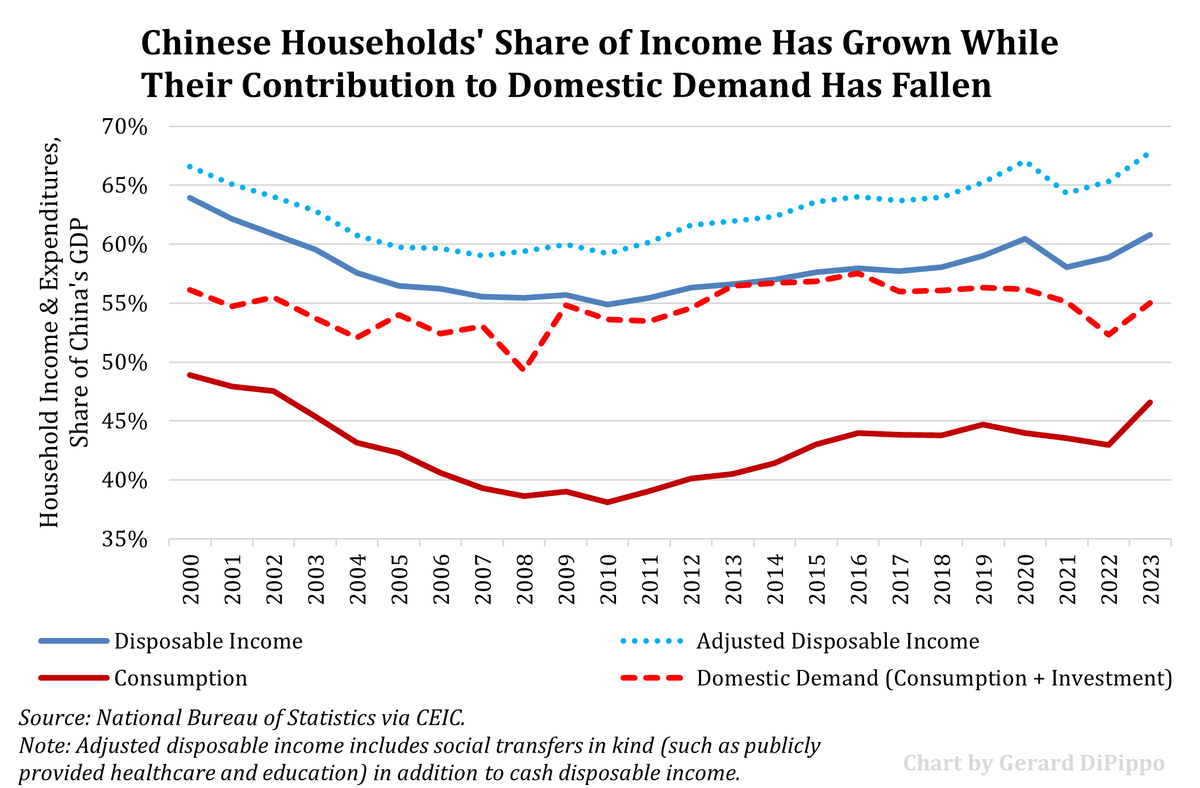

China’s “consumption problem” is often misunderstood, and the property sector is the missing link. It’s true, in accounting terms, that household consumption is low as a share of China’s GDP. But a common mistake is to equate “high household savings” with idle money sitting in a bank account. That’s not how China’s national accounts work.

Looking at China’s Flow of Funds data, it’s clear that household savings are not just financial savings. For much of the past two decades, savings were overwhelmingly allocated to “gross capital formation,” primarily purchases of new housing and related investment. From 2012–21, household capital formation (property) accounted for about 64% of household savings on average. Those “savings” were generating domestic demand through construction activity, upstream industrial demand, employment, and local government revenues. High savings do not necessarily mean weak demand.

That changed after China’s property downturn. As new home purchases collapsed, households shifted savings away from housing investment toward net financial assets (first bank deposits and, more recently, equities). That portfolio shift may be rational for households, but it does not directly create real economic activity in the way housing investment once did.

This helps explain why China’s domestic demand challenge is harder than it sounds. It’s not just about getting households to consume more or save less. It’s about how to replace a massive housing-investment demand engine. Households can only buy so many new goods, absent the need to stock new homes.

One consequence is that household consumption growth is tilting toward services. I estimate that services accounted for roughly 60% of nominal consumption growth in 2023–25. That supports incomes and employment, but it generates relatively less demand for manufactured goods.

Thus, one key tension with the upcoming 15th Five-Year Plan is its top goal of “building a modern industrial system.” From a demand perspective, the old engine is gone, and the new one looks very different.

Bottom line: when thinking about China’s “consumption problem,” think about the property sector and how to fill that giant hole in domestic demand. It’s not obvious how Beijing does that quickly.