Just finished my biggest macro piece yet for @blocmates.

If crypto feels sluggish, there’s a reason. The liquidity pipes have been creaking for months, and the macro signals aren’t all pointing in the same direction.

In this report I mapped every major catalyst for 2026 and created a framework on how to think about asset allocation heading into 2026.

Can Avici really scale into a DeFi Bank?

Just finished a protocol deepdive on @AviciMoney for @blocmates (link to the full analysis at the end).

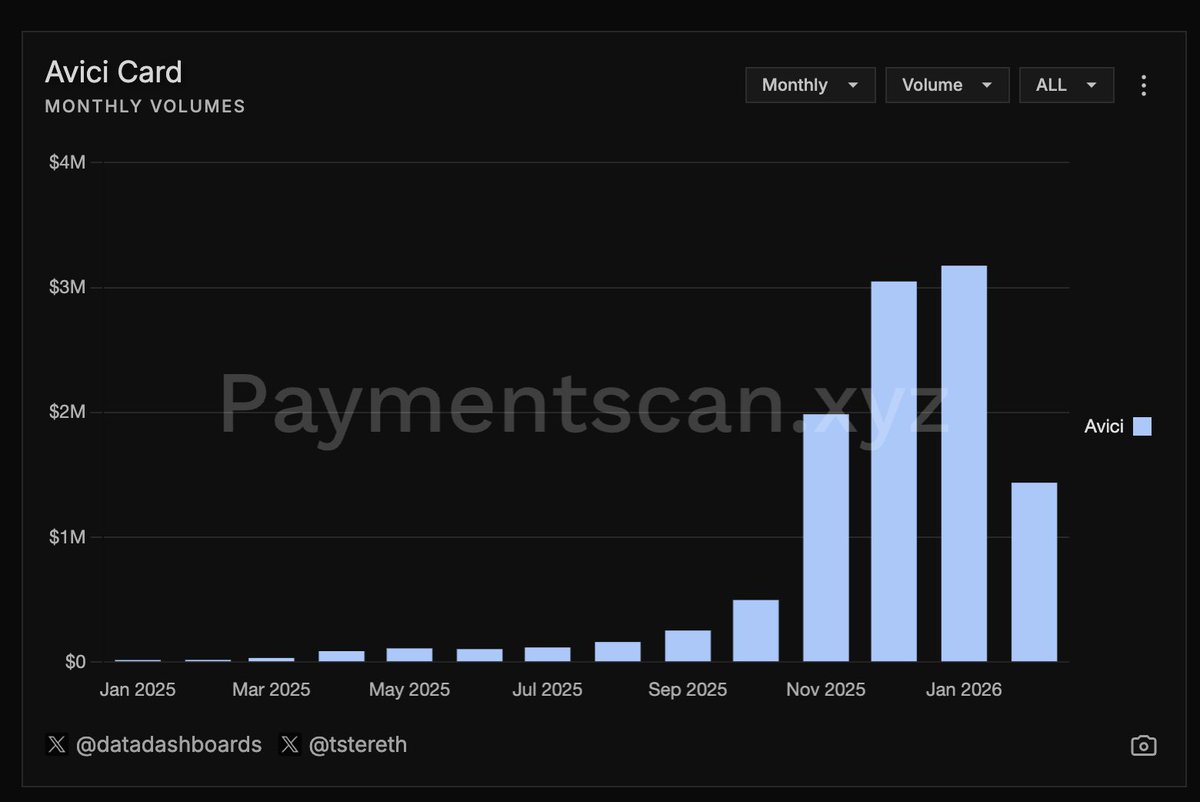

Most crypto cards are marketing tools on TradFi rails. Is $avici any different?

Avici differentiates itself with a recurring revenue engine that cements its survival in this bear market, a roadmap that does not lack ambition, exemplary governance, and a valuation that makes it worth taking a look at.

Using a 7x fintech peer group derived revenue multiple and 350% expected spend growth over the next 12 months, Avici trades at a revenue yield of ~20%. That’s an attractive premium vs benchmark yields derived from staking ETH or SOL. Is it an adequate compensation for the risk?

The sensitivity is high, and depends on sustained spend volume growth and roadmap execution.

Let’s dive into the details 🧵

Governance & our final stance

Where Avici genuinely differentiates is governance. Most crypto business models that failed have governance structures that completely misalign teams, VC’s and minority investors.

Thanks to the launch on @MetaDAOProject , Avici is different, and sets an example:

• No VC allocation

• No team allocation at launch

• Treasury controlled via futarchy (decision markets put the minorities in full control)

• Team incentives are tied to token performance and need to be approved by tokenholders

Alignment is strong, which is a key value driver for long term outperformance.

Our stance:

It deserves a fintech multiple today.

It earns a protocol multiple only if execution matches roadmap ambition.

🔗 Link to the article:

https://t.co/6InET0CMsI

So where is the upside?

The upside sits in the roadmap; we compared each vertical in its extensive roadmap from a risk return perspective and minimal capex requirement to establish an MVP.

Most interesting vertical? Trust Score:

• SaaS-style margins

• Lower capex requirement

• Logical extension of card data

Entering the lending business is higher risk:

• Capital heavy

• Regulatory heavy

• Requires TradFi talent in leadership which it currently does not have

Full rollout of the complete roadmap likely requires substantial capex as current recurring earnings are light to finance the ambitions. This means execution risk.

The bull market will happen in tokens that look and operate more like public equities than traditional governance tokens.

Market is demanding cash-flows, programmatic buybacks, transparent & public accounting, and real onchain business model forecasting with path to sustainable revenues.

It will be very difficult for a lot of teams to swallow this and deal with this new environment, but that is what the next phase will be like, and it will be a massive "trimming of the fat" in the entire industry.

Position accordingly.

Our new @MetaDAOProject Dune dashboard is now live!

Track everything you need to know about their ICOs, ownership coins, futarchy activity, and more all in one place 👇