We have been getting some questions from LPs why we carry the otc amounts at a discount to current spot. We only do trades on highly liquid spot/perp with multiple tier 1 venues and enough history.

The discount collateral formula:

For a deal with n vesting tranches:

Total Value = Σ vᵢ × spot price × min((1 − discount)^(days to vestᵢ ÷ 365), cap)

Each tranche is valued independently, then summed. For every tranche we take the lesser of the time discounted value or the cap, whichever is more conservative.

Worked theoretical example using OTC 9 from the dashboard

OTC 9 is active, 61% vested, 294 day duration, Linear + Cliff vesting. Let's assume it has just 2 remaining tranches:

Tranche A

Tokens (vᵢ) - 5000

Days to vest - 90

Spot Price - $1

Tranche B

Tokens (vᵢ) - 5,000

Days to vest - 294 days

Spot Price - $1

Using a 35% discount and cap = 0.75:

Tranche A: 5,000 × $1.00 × min((0.65)^(90/365), 0.75) ->(0.65)^0.247 = 0.888

We us min(0.888, 0.75) = 0.75 cap kicks in so value carried at in reserves = $3,750

Tranche B: 5,000 × $1.00 × min((0.65)^(294/365), 0.75) (0.65)^0.805 = 0.693

Min(0.693, 0.75) = 0.69 Time weighted discount used so value in reserves = $3,465

Total booked value = $7,215 vs $10,000 market price ~28% markdown.

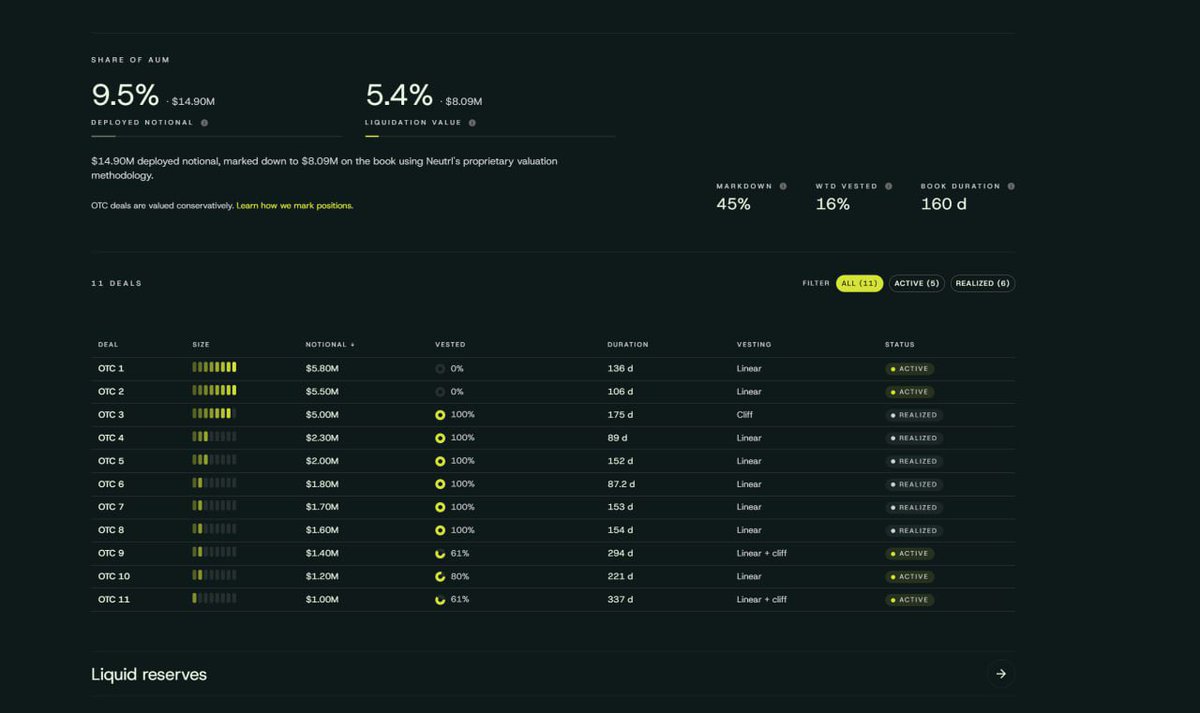

The dashboard shows this in action at scale:

$14.90M deployed (notional for current live deals) ~ 9.5%

$8.09M liquidation value (what it's booked at after discounts to be conservative) - 5.4% shown in reserves

The further out the vest, the harsher the haircut. Even near vesting tranches get capped below spot.

This is intentional conservatism, it means NUSD's collateral is never overstated even at the current 103% .

Imagine controlling one of the world’s most strategic shipping routes and having to ask:

“wait guys who has the multisig” “ledger not detected” “bro approve on the other wallet” “why is gas 47$” “who clicked the phishing link”

🚨NEW: Iran has launched “Hormuz Safe,” a state-backed maritime insurance platform for vessels transiting the Strait of Hormuz that allows settlement in Bitcoin and other cryptocurrencies instead of traditional banking rails or even stablecoins.

The platform is designed to bypass SWIFT and Western financial intermediaries following recent enforcement actions that froze hundreds of millions in Iranian-linked USDT.

crypto is the only industry where people use a product for 2 weeks and get mad they didn’t receive equity in the company.

imagine buying an iphone and tweeting:

“where is my $AAPL allocation?”

Neutrl captures what most market participants never see.

Yield is generated from real trading activity by capturing inefficiencies between OTC and spot markets.

Powered by actively managed, delta-neutral strategies developed by a team of quants.

gNeutrl

“Neutrl will become a blackhole for altcoins.”

I laughed when a fund said this last year.

We have been very risk off with everything in this market, the inbound has been higher than expected recently, and currently sifting and working on a $40M deployment into the top 25 tokens over the next few months.

gNeutrl.

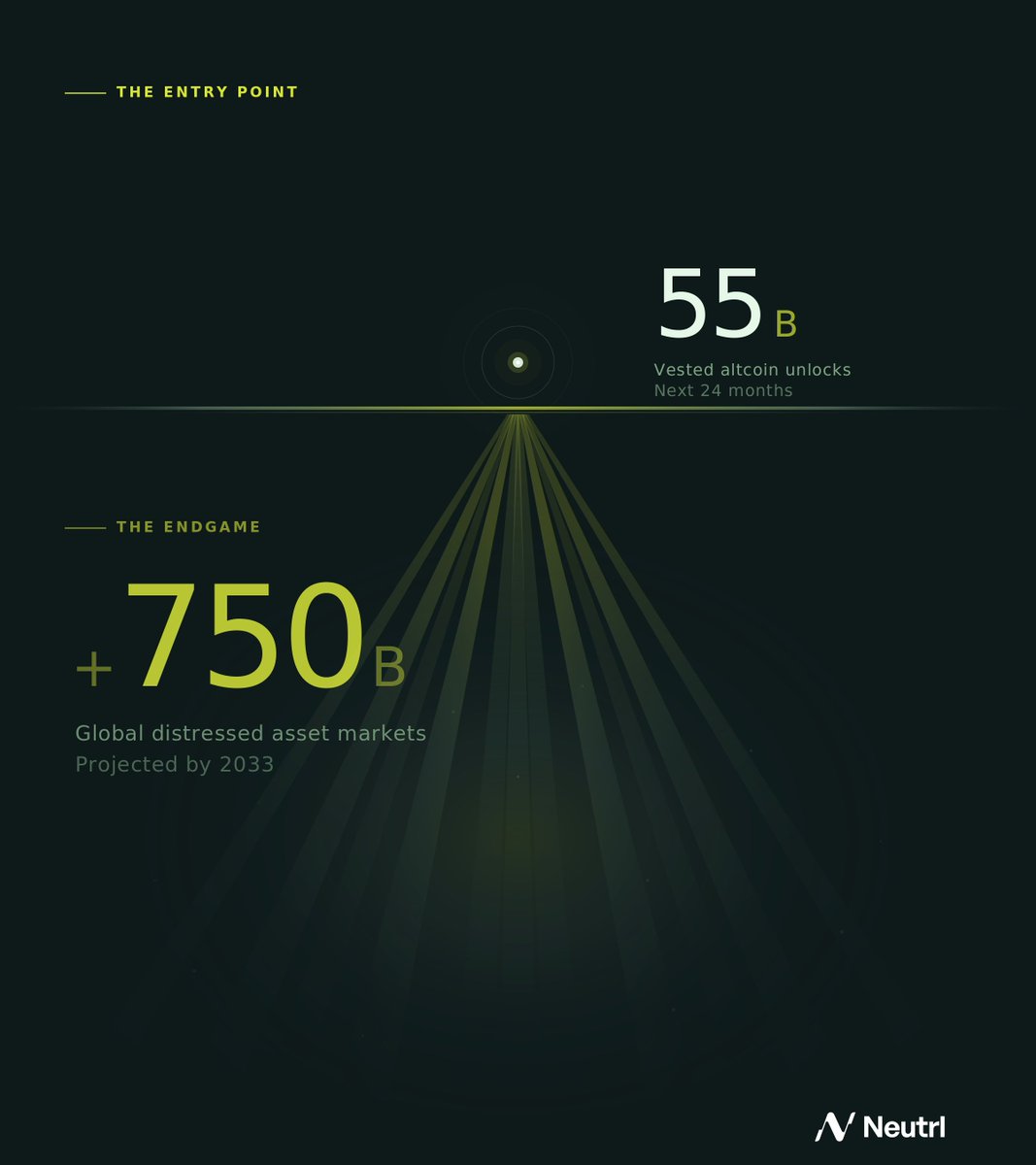

There is over 55B in altcoin supply set to hit the market over the next two years.

Neutrl has found a niche by capturing this flow by sourcing discounted OTC allocations and running institutional-grade strategies to generate non-directional returns.

The current altcoin pipeline is meaningful, but it is just the starting point. The same mechanics behind OTC altcoin deals are not unique to crypto.

They are the foundation of distressed asset markets in tradfi. When liquidity dries up, assets are forced to trade at a discount, and access is limited to a small set of buyers.

That opportunity is already massive and continues to grow, with projections exceeding 750B by 2033.

As private credit and debt markets move onchain, distressed assets are a natural extension.

OTC everything.

few corrections here:

1/ locking requires explicit confirmation, the UI doesn’t “accidentally” lock funds

2/ pendle pools were announced well in advance

3/ total points are ~880B, not 1.22T

also worth noting: points aren’t a fixed-yield product. they’re incentives.

if the strategy is optimizing APR from a speculative airdrop, the system is probably being misunderstood.

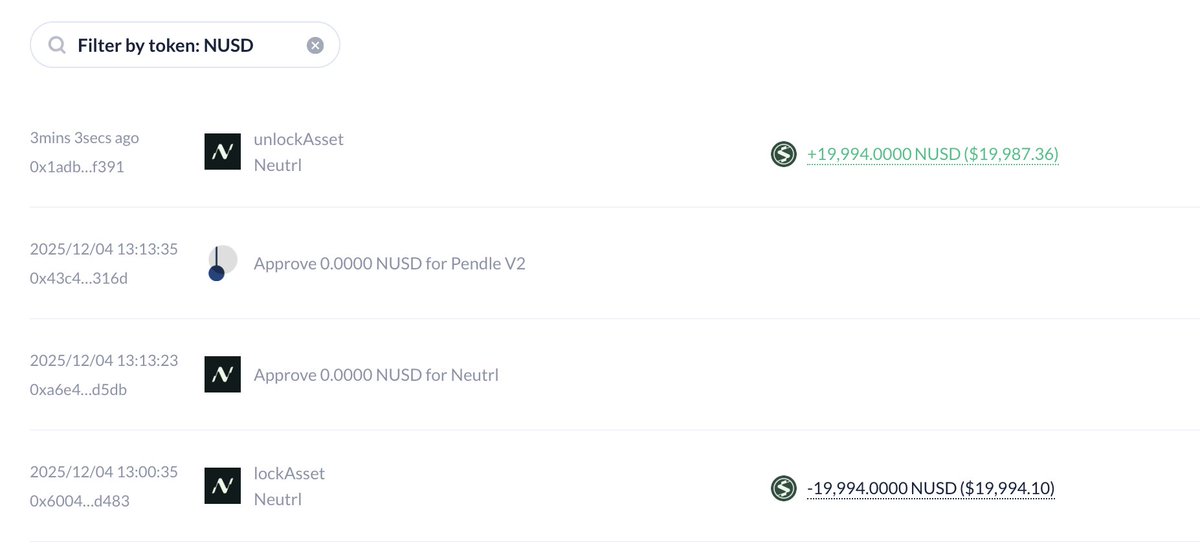

3 months ago, I accidentally locked $20k $NUSD for 3 months due to something weird with their UI at the time. I was supposed to choose stake & lock. After that, they launched a Pendle pool with high multipliers, which diluted the locker option.

Now my 20k $NUSD has unlocked, and I received 53.83M points.

Total points right now are 1.22T (https://t.co/HYNDlo2zfK).

Neutrl @Neutrl currently has TVL stuck around $200M. If we assume the TVL stays around that level for the next 3 months and the point program continues for another 3 months (so 6 months in total), then the total points would reach around 2.45T.

I made a simple table showing the price per 1M points based on different airdrop allocations and FDV assumptions.

If the airdrop supply is 5% and the FDV is $200M, the price would be about $4.07 per 1M points.

In my case, locking 20k NUSD for 3 months generated 53.83M points, meaning I would receive around $219.1 in airdrop value.

That’s only ~4.38% APR.

Looks like it’s not worth locking.

Their multiplier system isn’t fair, and the points are getting diluted very quickly

It’s time to say goodbye if they don’t have a clear TGE date or snapshot. Even with a good tech idea, if the points program is poorly designed, then it’s simply not worth farming.

Senior and Junior sNUSD are now live via @strata_markets.

Strata introduces Senior and Junior tranches on sNUSD, enabling users to access Neutrl’s yield through differentiated structures aligned with varying risk profiles.

tldr:

> usde is the product. yield is the moat

> cutting yield for buybacks → weaker usde → less adoption → less revenue

> still doesn’t offset ena emissions

> optics ≠ value. protect the engine first

what’s the strongest counter-argument?

This was in July 2025. 4 months before Neutrl launch. Our first public talk.

The thesis played out. You will make more money buying tokens at a discount while shorting perps at market price. Too many emissions, not enough capital to bid. Most tokens end up down only over time even if the underlying business is great.

Tremedous bear market and we are still the highest real yield onchain.

We will also be the highest yield onchain when the bull market returns.

gNeutrl.

Neutrl is designed to generate asymmetric yield independent of market direction.

By pairing OTC arbitrage with advanced delta-neutral strategies, Neutrl generates consistent, crypto-native returns regardless of market volatility.

Real yield without directional risk.

gNeutrl

NUSD just crossed a new ATH.

We’ve been growing steadily with organic volume by simply offering the highest risk-adjusted yield in the industry. No leverage. No rented TVL.

Soon, you’ll see new integrations building on top of NUSD, including vaults, lending markets, and other structured yield products to accelerate this growth.

We’ve been intentional with a slow and steady rollout, focusing on the core strategy and building our moat.

The next phase starts soon.

gNeutrl.

I have teams asking Tom, Dick and Harry said they worked with you. How were they?

Please ask us before working or paying anyone. Neutrl is a tight team with a few trusted service providers on custodians, exchanges, security monitoring/prevention and reserve management.

We usually ask other teams as well and verify with @0xGroomLake to do background checks.

There are no outside:

- marketing agencies

- dev shops

- market makers

- traders/quants

- BD people

gNeutrl.

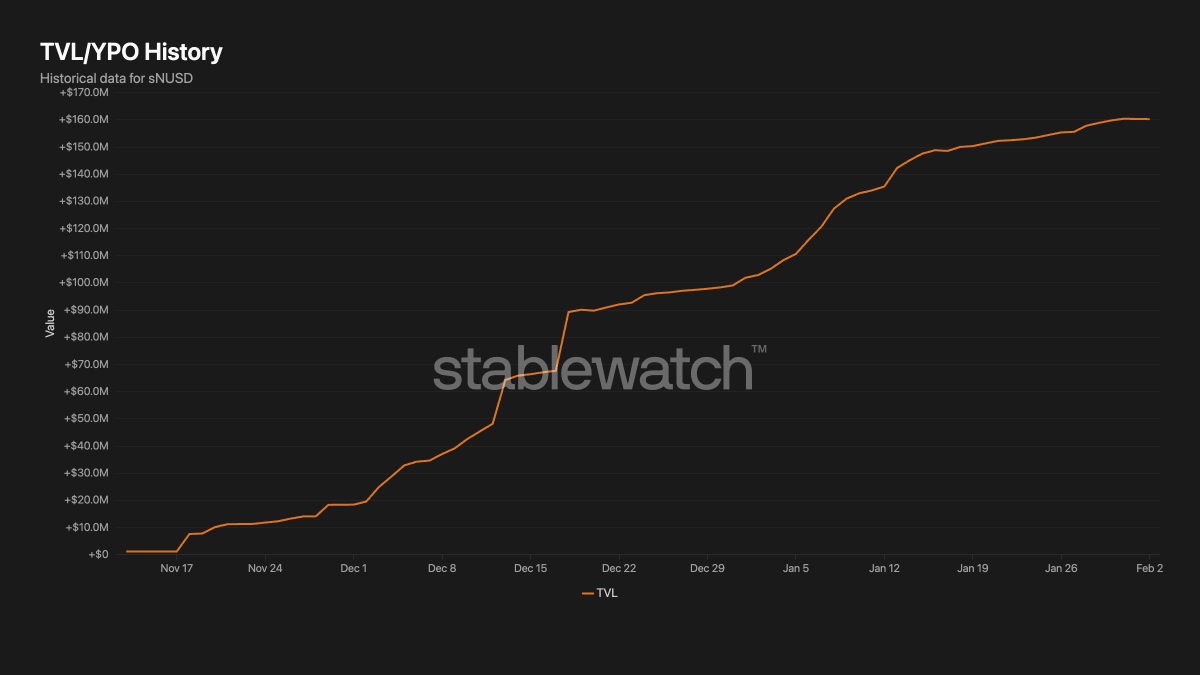

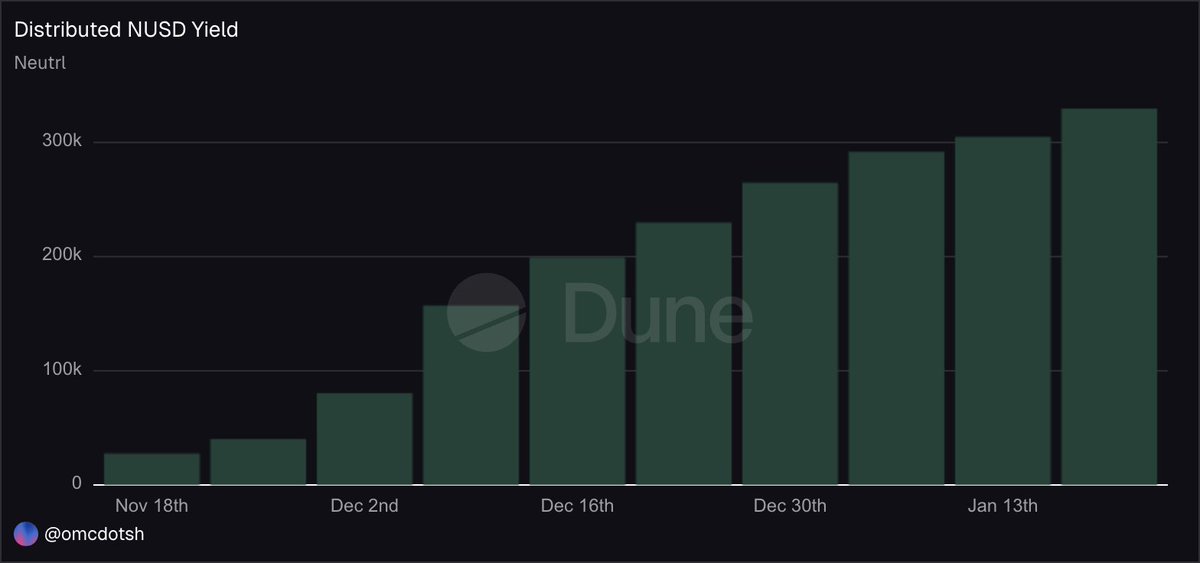

sNUSD has crossed 1.5M YPO in just two months since launch.

This is real yield generated from crypto-native trading activity without leverage or token emissions.

With new catalysts coming online and OTC deals vesting, yield distribution will grow exponentially.

gNeutrl

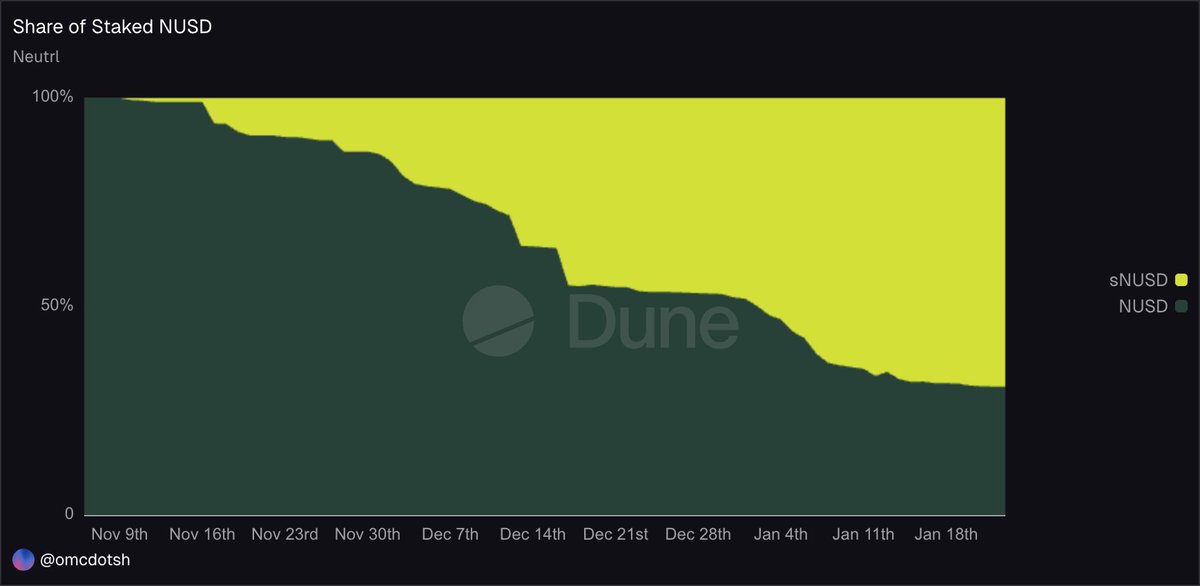

sNUSD staking ratio currently sits at 69% (nice) and still paying out >11% yield.

This represents a ~94% increase over the past 30 days and places sNUSD among the highest staking ratios of any synthetic dollar.

The @Neutrl yield engine is humming along as designed.

gNeutrl

Crypto has an onchain capital problem. There is limited net new capital entering, and a large share of existing liquidity remains concentrated among a small group of established players.

Much of the activity we see today is capital rotating across the same funds, rather than new inflows expanding the market. This has caused the existing incumbants to thrive while everyone else PVPs.

This is why @Neutrl is leaning into a different path this year. We are actively onboarding DATs, family offices, and funds who are new to onchain markets and looking for risk-adjusted yield on their crypto exposure.

These allocators aren’t looking for riskier tokenized versions of legacy products. They want yield that comes directly from crypto-native activity. These have been our largest LPs.

Side Note: I’m still bullish on protocols bringing in exogenous, non-crypto-correlated yield, but there’s also a huge amount of opportunity that already exists within crypto’s own market structure.

gNeutrl