Meet our student Owen.

He was honoured at the ACCA Annual Student Summit and Job Fair where he grabbed:

1st in Ghana, 2nd in the world for Strategic Business Leader.

1st in Ghana, 15th in the world for Strategic Business Reporting.

Congrats @ooadantey!!! #UGBSStudents

The Romans called it Panem et Circenses, means “Bread and Circuses.”

The idea is simple. Don’t fix the people’s problems. Just feed them and entertain them.

A satisfied, distracted population never revolts.

Roman emperors perfected this trick 2000 years ago and it has never stopped working.

Lets throw the biggest Easter carnival in the Central Region with top musicians and free condoms. The people are fed. The people are entertained. The people are happy.

There’s nothing new under the sun 👍🏾

TLDR: I am a recovering alcoholic with no fund, no credentials, and no lobbyist. I rebuilt myself from nothing. Then I broke into finance with no degree, no pedigree, and no permission.

I parsed SEC filings for a $31.5 billion private credit fund called Cliffwater. Not because anyone asked me to. Because nobody else would. The filings are public, but they are buried in footnotes that are not indexed, not searchable, and not structured for analysis. I have been told by fund managers that nobody even attempts this.

Billions of dollars in pension capital, and the people who manage money for a living do not bother to read the filings.

So I read them. Every loan. Every amendment. Every semi-annual PIK disclosure. 2,330 positions. I hand-researched fifty.

I found 189 loans where borrowers are paying interest with more debt instead of cash. I found over 50 loans that are not generating enough cash to service their debt at all — carried at par on the books of a fund that has never reported a losing month in 41 months.

The fund's Sharpe ratio is 3.75. Bernie Madoff — who was fabricating returns and could pick any number he wanted — ran a 3.5. He got caught because the numbers were too smooth by Markopolos. The greatest quant fund in history, Renaissance Technologies, runs a five or six.

Cliffwater is claiming risk-adjusted returns that would be impossible even if you insider-traded with perfect information every single time, because the volatility of the underlying markets would still prevent it.

Nobody asked questions.

Bloomberg confirmed 14% redemptions 48 hours after I published. S&P cut the fund's outlook to negative this week. Cash on hand fell 76% in six months.

This is not an isolated fund. This is the structure. $9.4 trillion in private equity. $3.5 trillion in private credit. They all pay their own valuation agents. The valuation agents decide what the funds are worth. No valuation agent has ever been fired for saying the number was too high.

The marks produce the NAV. The NAV produces the fees. The fees come from pensions. The pensions come from firefighters and teachers and nurses in Oregon and California and Illinois who will never read a private placement memorandum in their lives.

Wall Street ran out of rich people. The endowments were full. The sovereign wealth funds were tapped. So they went downstream — to 401(k)s, to retirement accounts, to interval funds sold to people who have no idea what they own.

1. Direct the SEC and FSOC to examine Level 3 fair value practices across interval funds and BDCs.

2. Require that valuation agents be independent of the funds they mark.

3. State publicly that the current self-marking regime creates systemic risk.

4. Mandate position-level mark disclosure for every fund that accepts pension capital.

There are two ways this ends. It breaks all at once like 2008 and we fix it. Or it rots slowly like Japan: one fund blows up, six weeks of quiet, another one, and nobody connects it for a decade while a generation of retirees gets destroyed.

I am not asking anyone to take my word for it. I am asking them to read the filings.

If you know someone in the administration, a regulator, or anyone on a legislative committee, please send this to them. One person learned this from a one-bedroom apartment. Your government can too.

The will is what is missing.

I have gone personally through quant interviews at institutional firms. This article is the closest thing to an insider breakdown I have ever seen shared publicly.

Read it tonight.

This kind of content does not stay public forever.

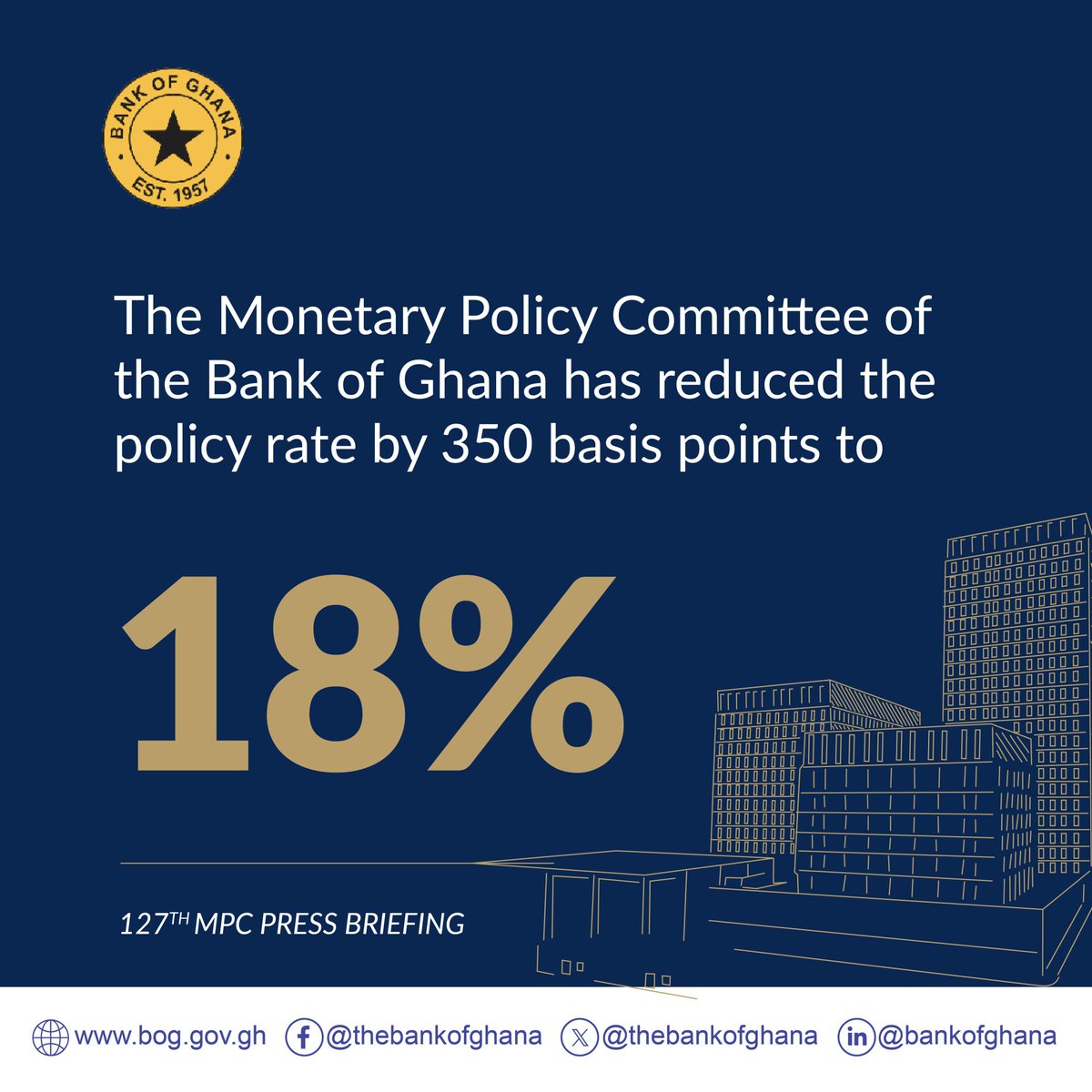

EXPIRATION OF DDEP-INDUCED RESTRICTIONS ON DOMESTIC BOND ISSUANCE

1. The Ministry of Finance announces the

expiration of the restrictions on new domestic bond issuance.

2. The three-year restriction measure was imposed in 2023 to prevent Government from issuing new bonds following the debt default that preceded the Domestic Debt Exchange Programme (DDEP).

3. This comes at a time when inflation is low, investor confidence has improved, and the macroeconomic environment is strong, supported by a robust medium-term debt management strategy and significant buffers.

4. Since 2025, the Government has honoured every coupon payment and obligation under the restructured bonds, demonstrating its credibility, fiscal discipline, and commitment to responsible debt management.

5. The expiration of the restrictions paves the way for government to drastically reduce its dependence on Treasury bills to finance its budget and allows for the issuance of new longer-dated domestic bonds.

6. President John Dramani Mahama’s administration is once again deeply grateful to the Ghanaian people for their forbearance and cooperation during the difficult period.

END

GOVERNMENT DELIVERS ROBUST 2025 FISCAL PERFORMANCE AND BROAD-BASED MACROECONOMIC TURNAROUND

The year 2025 marked one of the most significant economic turnarounds in Ghana’s history.

Government successfully reversed the economic challenges inherited, as evidenced by the following end-2024 indicators:

i. The primary balance on commitment basis recorded a deficit of 3.0 percent of GDP;

ii. The 91-day Treasury bill rate was at an extremely high 27.7%;

iii. The Ghana cedi depreciated by 19.2% against the US dollar; and

iv. Inflation was high at 23.8%.

Through a combination of fiscal discipline, commitment controls, deepened structural reforms, and prudent monetary policy, macroeconomic stability has been restored and public finances placed back on a sustainable path.

Reforms in revenue mobilization and spending control anchored fiscal performance in 2025, resulting in the following outcomes:

i. The overall fiscal balance on commitment basis recorded a deficit of 1.0% of GDP, significantly outperforming the target deficit of 2.8% of GDP.

ii. The primary balance on commitment basis improved significantly to a surplus of 2.6% of GDP, exceeding the target surplus of 1.5% of GDP.

ii. The overall fiscal balance on cash basis recorded a deficit of 3.1% of GDP, better than the target deficit of 3.8% of GDP.

iii. The primary balance on cash basis achieved a surplus of 0.5% of GDP

The strong outturn in the 2025 fiscal performance, coupled with sound debt management strategies, resulted in lower public debt levels.

Ghana’s public debt stock reduced significantly by GH¢82.1 billion, from GH¢726.7 billion (61.8% of GDP) in December 2024 to GH¢641.0 billion (45.3% of GDP) in December 2025. This represents one of the sharpest debt reductions in Ghana’s history.

Beyond fiscal consolidation, significant macroeconomic gains have also been delivered, with key indicators rebounding strongly.

Key Macroeconomic Performance Highlights:

A. Real GDP growth strengthened, with a provisional 6.1% year-on-year growth in the first three quarters of 2025, driven mainly by services and agriculture.

B. Non-oil growth was even higher at 7.5% in the first three quarters of 2025, compared to 5.8% in the same period in 2024.

C. Inflation has fallen for thirteen consecutive months, declining sharply by 19.7 percentage points, from 23.5% at the end of January 2025 to 3.8% at the end of January 2026.

D. Interest rates have fallen sharply, with the 91-day Treasury bill rate dropping from 27.7% at end-2024 to 6.5% in February 2026, lowering government borrowing costs and freeing up credit for the private sector.

E. The average commercial bank lending rate fell sharply from 30.25% in 2024 to 20.45% in 2025. With inflation currently at 3.8%, the downward trend is expected to continue.

F. Credit to the private sector expanded by GH¢17.1 billion in 2025, with further growth expected in 2026.

G. The cedi appreciated against the US dollar by 40.7% by end-December 2025, 30.9% against the pound sterling, and 24.0% against the euro.

H. Our external position strengthened, with the current account recording a surplus of US$9.1 billion by end-December 2025, up from US$1.5 billion in 2024.

I. Gross international reserves reached US$13.8 billion, enough to cover 5.7 months of imports.

The macroeconomic turnaround is broad-based and comprehensive. All sectors of the Ghanaian economy have witnessed remarkable improvement.

For emphasis, between 2024 and 2025:

i. Inflation reduced significantly from 23.8% to 5.4% and is currently at 3.8%.

ii. The cedi appreciated against the US dollar by 40.7% in 2025, compared to a depreciation of 19.2% in 2024.

iii. The 91-day Treasury bill rate reduced from a high of 27.7% in December 2024 to 11% in December 2025 and is currently 6.5%.

iv. Public debt reduced significantly by GH¢82.1 billion, from GH¢726.7 billion (61.8% of GDP) in December 2024 to GH¢641.0 billion (45.3% of GDP) in December 2025.

For those in the 62% tax tap, the new salary sacrifice rule gives you two options:

- Continue to sacrifice and pay 2% NI on money you've not seen... then pay tax on it again when you see it

- Pay 62% tax and keep 38% of money in the red zone

This policy is MAD

There's logic in here based on the policy aims. While I would've preferred a carrot not stick approach - this isn't as bad as it could've been, £12,000 per year is still a reasonable whack for many people.

The stated aim was not to raise revenue but to encourage young people to invest rather than save - both for the economy but also because on average it outperforms.

When I met Chancellor on this a few weeks ago, I pointed out that a blanket cut to the limit would be perverse, to cut cash ISA limits to older people to encourage younger to invest wouldn't work. So the carve out for over 65s makes total sense and I'm pleased she listened.

What needs to happen along with this is better investment education, easier access to guidance, and better investment incentives for young people.

CASH ISA NEWS. Changes from 6 April 2027

Cash ISA annual allowance cut to £12,000 (from £20,000) per tax year

This will not apply to over 65s, who will keep £20,000 cash ISA limit

The shares ISA will remain at £20,000

Remember this ONLY impacts new money being put in, it won't impact money already in ISAs #Budget2026

Our new forecasts for the economy and public finances will be published tomorrow alongside the Chancellor’s #Budget

Follow us for charts and highlights 📊

I’ve worked in private equity, family offices and hedge funds. Analyst, PM, CIO. Seen a lot, learned a lot the hard way. I’ve seen what works, what I think hasn’t worked, what makes people last and get better, and also what gets them carried out.

There’s a lot of garbage advice on Twit. I really hope this isn’t that, and want to see you crush it.

Here are some things that I believe matter (will be a living compilation):

🧵

and here is the link to the paper showing how to manufacture: 2t of gold / GW / year.

https://t.co/8vslsmgX5v

So if 2 TW are produced this way the entire global gold mined in a year (3,000 t) can be generated in nuclear fusion reactors.