The most expensive "no" in Wall Street history, Bear Stearns turned down half of KKR for free, he left with $10k at 32, started an industry

Bear Stearns no longer exists, his firm manages $500 billion

"if you always worry about what you can lose and never worry about how much you'll make, you'll always make money"

"if you don't like change, you're going to like irrelevance a lot less"

bookmark and watch it today - it will change the way you think about risk, failure, and building something from nothing ↓

"I read everything: Annual reports, 10-Ks, 10-Qs, biographies, histories, five newspapers a day. On airplanes I read the instructions on the backs of the seats. Reading is key.

Reading has made me rich over time."

— Warren Buffett

🚨 REALITY CHECK: There are 7 mental models that exist purely to keep successful people from becoming delusional.

Munger. Buffett. Taleb. Howard Marks. Gary Klein. They all used different frameworks to stay humble after winning.

Here are 7 prompts based on them: 👇

I find that reading various magazines covering business and technology and ideas can be helpful for expanding your Latticework of mental models (s/o Charlie Munger). Some of these magazines cover a large variety of topics/ideas.

“Munger explains: “Models have to come from multiple disciplines because all the wisdom in the world is not to be found in one little academic department… Fortunately, it isn’t that tough because 80 or 90 important models will carry about 90% of the freight in making you a worldly-wise person.”

That said, Munger points out that there is no ‘master list’ that will work for everyone, rather you will need to build and continually update your list of mental models depending on your challenges, needs and context.”

When Munger said this, I think he was really talking about core academic disciplines such as psychology, physics, biology, etc. But I beleive the same concept can be expanded beyond that. You learn new concepts and ideas.. some will replace old ideas you once had because the new information is superior in discovering the truth of how the world/things actually work.

You continually learn and it all meshes together, forming “the latticework” as Charlie would call it. You rely on this latticework and it improves over time. Some of the concepts you learn will sometimes pop up and prove to be useful when you least expect it.

An example is this excerpt below, which got my gears turning about the oil industry. I realized I really don’t understand anything at all about how the oil truly works or impacts the world economy. I would like to better understand this. Surely, understanding how the oil industry works will prove to be beneficial in better understanding how the world works… in one way or another.

I hear Oil 101 is a good book to start with.

Luis Enrique ha ganado 3 Champions como entrenador.

Se levanta a las 6:00, entrena en ayunas y cena hasta 6 huevos diarios.

Pero su enfoque de la salud difiere del típico entrenador de élite.

Aquí 6 cosas que hace a los 56 para un físico de hierro (y cómo aplicarlas hoy):

À 33 ans, Rockefeller était déjà milliardaire.

À 38 ans, il contrôlait 90% du pétrole américain.

Il allait à l'église chaque dimanche. Et ruinait ses concurrents chaque lundi.

Il avait compris quelque chose que ses rivaux n'ont jamais voulu admettre : la majorité des hommes sont fondamentalement FAIBLES. Et il avait construit un système entier pour exploiter cette faiblesse.

5 stratégies qu'on ne vous enseignera jamais dans une école de commerce. 🧵

When Henry Ford arrived in England, he asked for the cheapest room in town.

The clerk at the counter was confused.

Standing in front of him was one of the richest and most famous men in the world the founder of Ford Motor Company.

Yet his coat looked old.

His suitcase was plain.

And instead of luxury, he simply asked:

“Where’s the most economical place to stay?”

The clerk stared at him for a moment before asking carefully:

“Excuse me… are you Henry Ford?”

Ford nodded.

Still shocked, the clerk said:

“Your son stays in the finest hotels and wears expensive suits.

But you’re asking for the cheapest room… wearing an old coat.

Why?”

Ford smiled and replied:

“All I need is a place to sleep.

Wherever I go, I’m still Henry Ford.”

Then he touched his coat and added:

“This belonged to my father. It keeps me warm. That’s enough.”

And then came the line that stayed with people:

“My son still worries too much about what others think.

I learned long ago that you don’t pay for approval.

I didn’t become rich by spending money.

I became rich by understanding what matters and what doesn’t.”

That’s the difference between looking wealthy and understanding wealth.

Real confidence doesn’t need luxury to prove itself.

Because your value isn’t your hotel room.

Or your clothes.

Or the opinions of strangers.

You are who you are wherever you are.

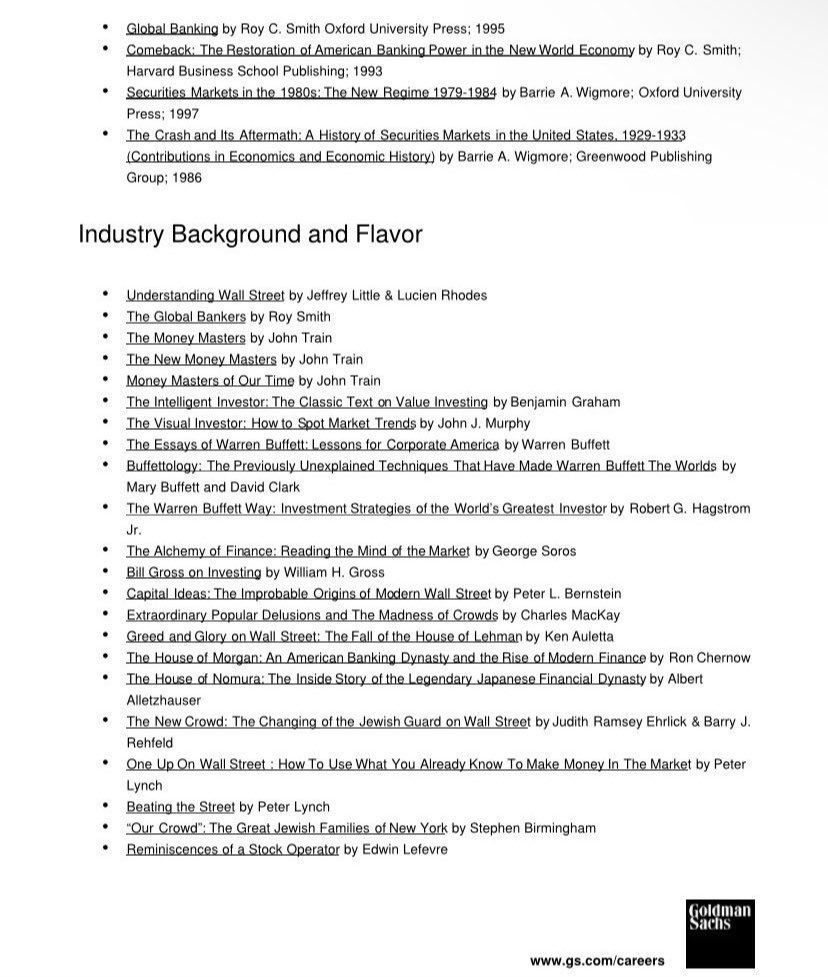

Want to know what it takes to make it on Wall Street?

This Goldman Sachs "Recommended Reading" list, given to incoming analysts, covers everything from market psychology to complex derivatives.

Bookmark this tweet so you don't lose the ultimate finance syllabus.

1/2

Berkshire Beyond Buffett

I finished this masterpiece few months ago, an outstanding read, easily a 10/10.

The book offers remarkable insights into Berkshire Hathaway’s subsidiaries, how they were founded, how they operate, and how they ultimately became part of the Berkshire family under Warren Buffett. The stories, the culture, and the emotional journeys behind these businesses are all captured beautifully.

Before reading Berkshire Beyond Buffett, I often wondered what would happen to Berkshire after Buffett, whether the company would retain its legacy and continue operating with the same discipline and culture. After finishing the book, I am far more confident that Berkshire will continue to thrive with or without Buffett. The company’s decentralized model, strong culture, and the autonomy given to its subsidiaries create a structure built for long-term durability.

One of the most impressive aspects is how many family businesses willingly choose Berkshire as their acquirer. They trust Berkshire’s promise of independence and appreciate that their unique culture and legacy will remain intact. This approach makes Berkshire Hathaway one of the most distinctive organizations in the corporate world.

Overall, Berkshire Beyond Buffett is an insightful and inspiring read for anyone interested in business, leadership, or the philosophy behind one of the world’s most successful companies.

Nicolai Tangen has interviewed all the most important CEOs and investors in the world (that's what $2T AUM buy you: lots of access). He has also interviewed a fair number of HF managers. Here are my favorites. Even so, it's almost 4 hrs. But I recommend actually listening, over the gemini summary.

Chris Hohn: https://t.co/5CdNm3fHI6

Paul Singer: https://t.co/DLq2U0atoa

Marc Rowan (not a HF, still interesting): https://t.co/k2BHwbPJFv

Stan Druckenmiller: https://t.co/H4sOAC1mU4

Ken Griffin: https://t.co/iepjcVwGOZ

At 81 he manages $72 billion, and says markets right now are "just about as risky as I've ever seen" and AI is "way over its skis"

He has never celebrated a winning trade in 47 years, this is the most feared investor on Wall Street

the full story is in this 40-minute interview - every satisfword of it is worth your time ↓

Chris Hohn did a 90-minute sit-down with Nicolai Tangen and then dropped an investor letter the FT got hold of last week.

You’d think the guy who printed a record $18.9B last year would be doing victory laps. Instead he’s quietly rewiring his whole portfolio.

My favorite takes from both:

1.The most important thing in investing isn’t growth. It’s barriers to entry. Growth without a moat is the airline industry: 5% volume growth for 100 years and basically zero cumulative profit.

2.There are only about 200 companies on earth he considers high-quality and investable. His fund holds 15.

3.Average holding period: 8 years. Some positions 13. “You have to hold the company forever, because the stock market may be at very bad prices when you want to sell.”

4.His real test for a moat: can the company price above inflation? A 20% margin business that prices 1% above inflation grows profits 5% faster than revenue. Forever. Almost no companies can do this.

5. Industries he won’t touch: banks, autos, retail, insurance, tobacco, asset managers, fossil fuel utilities, airlines, wireless telecom, media, advertising. On banks: “sooner or later someone without a lot of intelligence comes to run them, and then it can be toxic.”

6.On AI generally: call centers go bankrupt. Indian outsourcing coders are next. But for everyone else, AI lowers costs and raises productivity. Companies with real moats become MORE valuable.

7. Here’s the punchline. The FT got hold of his investor letter. He cut his Microsoft stake from 10% of the fund to 1%. Roughly $8B sold. He’d held it since 2017 through a 400% rally. His reason: AI could disrupt Office and Azure faster than the market thinks.

8.He moved that capital into Alphabet. Doubled it from 3% to 5%. Now his largest tech position. The world’s best quality investor sold Microsoft and bought Google because he thinks Google’s moat is more durable in an AI world. Not the consensus trade.

9.The underlying thesis: “AI eats software.” If AI agents do the work humans used to pay per-seat SaaS licenses for, the whole SaaS model gets re-rated. Oracle, Adobe, Salesforce all ~40% off highs. Microsoft 25% off. Market is starting to agree.

10.When to sell? Not when something gets expensive. When conviction drops. Valuation is one variable, conviction is the other. What kills you isn’t being wrong, it’s permanent loss of capital.

11.He admits hardcore activism doesn’t work anymore. Too much of the shareholder base is passive index funds. And even when activism wins, you usually win in a bad business. “The business always wins.”

12.Counterintuitive take: there are more good companies in public markets than in private equity. The best businesses are too big for PE to buy. And when public companies sell something to PE, they’re selling the assets they want to get rid of.

13.On intuition: “thinking without thinking.” Pattern recognition from 20 years of reps. It’s how he sniffed out Wirecard while the German establishment was defending it. “Most investors trust authority too much.”

14.He basically stopped shorting. “You’re going to be eventually right but not be able to fund the losses.” The first guy to short Wirecard had to cover 19 years before it hit zero. Buffett told him he and Charlie studied shorting and concluded it was too hard.

15.He gives almost everything away. ~$500M a year. $10 prevents an unwanted pregnancy in Africa. $40 saves a child from severe malnutrition. $50 prevents permanent blindness.

16.Tangen asks: advice to young people? Hohn, who runs the world’s most profitable hedge fund: “Go on a spiritual path.” The guy who made $18.9B last year ends the interview saying only purpose and meaning matter.

The headline: the world’s best quality investor just sold his biggest tech compounder because he thinks AI is breaking the moat. Quietly, with conviction, on an 8-year horizon, while everyone else is still buying the AI winners of 2023.

Paul Singer lost 88% of his parents' life savings, then he built a fund that has made money almost every single year for 47 years straight

This is him explaining the one rule that made it possible

"my dad was a retail pharmacist, he and I traded tiny amounts of tech stocks, between 1967 and 1974 we found every possible way conceivable to lose money"

"when I started Elliott in 1977 with $1.3 million from friends and family, I was determined to engage in a strategy that made money all the time"

I read over 1,000 pages on how John D. Rockefeller approach his work.

These are my top 5 takeaways...

1. He saw business as war.

Rockefeller saw business like a game of chess. From his biography it says:

"He studied, as a player at chess, all the possible combinations, which might imperil his supremacy."

2. He planned relentlessly before executing.

As a boy he would play chess with the other kids:

"When playing checkers or chess, he showed exceptional caution, studying each move at length, working out every possible countermove in his head.

‘I’ll move just as soon as I get it figured out,’ he told opponents who tried to rush him.

‘You don’t think I’m playing to get beaten, do you?’"

“This part was vintage Rockefeller: He slowly and secretly laid the groundwork, then moved with electrifying speed to throw his adversaries off balance.”

3. He worked as though his life depended on it

At his first job at Hewitt and Tuttle they would make him collect payments. Sometimes people would refuse to pay him.

His biography says:

"Sitting outside in his buggy, pale and patient as an undertaker, he would wait until the debtor capitulated. He dunned people as if his life depended on it”

4. He had complete focus

Rockefeller said

“Do not many of us who fail to achieve big things… fail because we lack concentration-the art of concentrating the mind on the thing to be done at the proper time and to the exclusion of all else?”

5. Work was religious for him

He believed work strengthened his character, and formed him into a better person.

He said: “I believe the power to make money is a gift from God.

Having been endowed with the gift I posses, I believe it is my duty to make money and still more money, and to use the money I make for the good of my fellow man according to the dictates of my conscience.”

Rockefeller knew he was destined for greatness.