Prdctnomics - The economics of technology products

@prdctnomics

Building LLM products by day, studying the formula that creates great companies by night. Product, Software, Technology Mega Trends. Not investment advice.

Four years ago, humanoid robots were laughable research toys that fell over during demos. Today, they're attracting billions in investment dollars and sparking a technological gold rush.

Why now? Three forces have collided:

1. AI finally works. The same breakthroughs powering ChatGPT are giving robots the ability to understand commands and learn from mistakes.

2. We're running out of workers. Factories can't find people. Our population is aging rapidly, with fewer young people entering the workforce.

3. Manufacturing is coming home. But reshoring factories to high-wage countries requires automation on an unprecedented scale.

Tesla aims to build 500,000 humanoid robots annually more than the entire industrial robot market today. Figure AI just raised $675 million to push its robots into factories. They're targeting a price under $30,000 less than many cars. This isn't science fiction anymore. It's big business.

Where They'll Win First

Warehouses and factories are the initial battlegrounds. These environments involve repetitive tasks in spaces designed for humans, and labor shortages are severe.

By 2030, humanoids will become common in logistics centers and factories. They might not be your home butler, but they'll transform industrial work.

What steam engines did for muscle power, humanoid robots will do for physical labor.

We're entering a new era where value accrues to physical assets and supply chains/infrastructure are national security imperatives

There will be infinite demand for intelligence and we're rate limited by physics & compute

Lots of opportunities for startups. Bullish on builders

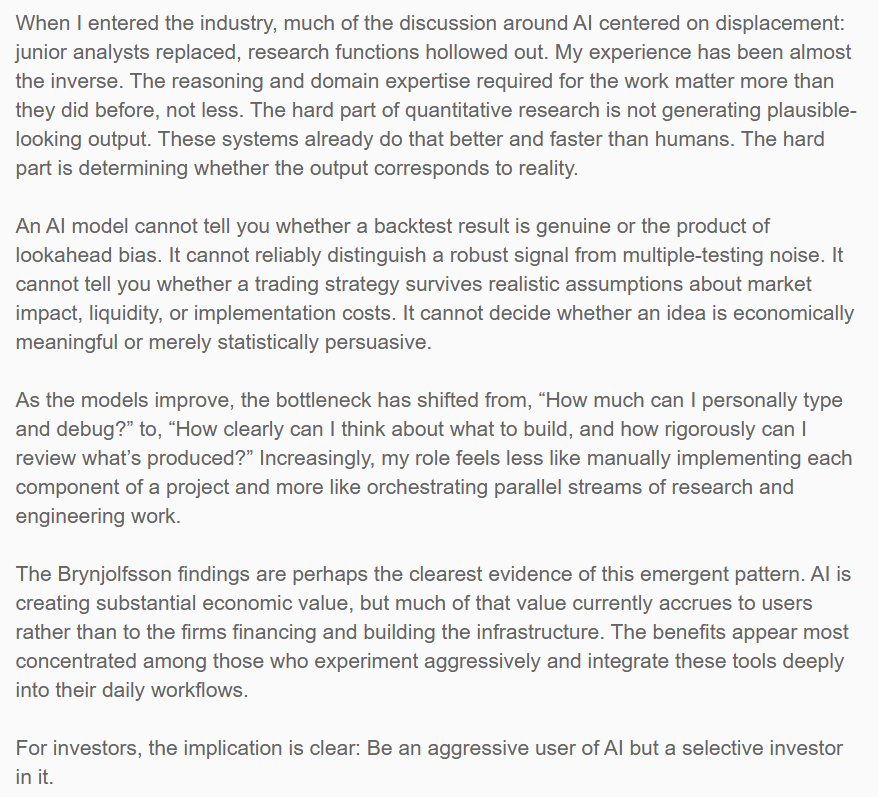

"Reasoning & domain expertise matter more than they did before, not less.

"The hard part of quantitative research is not generating plausible-looking output. AI systems already do that faster than humans. The hard part is determining whether the output corresponds to reality."

Active managers have had to grapple with Mag7 concentration first then single theme AI dominating index concentration for the last 5ish or so years.

Now you have several massive $1T+ IPOs coming to market. Market structure, passive/active distortions, etc. all evolving how this industry works.

“Bloomberg Intelligence estimates S&P 500 funds must absorb 19% of SpaceX's float within 6 months. Russell 1000 and Nasdaq 100 funds will absorb 24%.”

I think this is partially why @OpenRouter just raised $113M+ by @CapitalG

If you are an inference provider you can raise a ton of money now off revenues and amass capital to buy GPUs. You can use these GPUs to offset chinese models going closed source by using them for model training/fine tunes in the future

Inference provider revenues are driven by deploying open source models in an easy and safely accessible way. You can pay 1/100 to 1/1,000 the cost to access GLM/Qwen etc vs centralized APIs and not send your data directly to chinese APIs. Yay I get cheap intelligence and China doesn't see my full conversation history on giving my friend breakup advice.

You leverage that revenue growth (API spend) to buy a capital asset (GPUs) for the future If @alexatallah buys GPUs with this $113M it solves two things. The first is he can lower inference costs even more through owning the hardware (and get a nice multiple on it and take loans against them, and repeat) and second he could use those models for training runs or fine tunes in the future if China goes fully closed source

The other issue is inference providers don't get the same data flywheel an OpenAI or Claude gets (since someone else is running the model and theres no data retention to train future versions). This could negatively impact training runs maybe. I think this is another reason china models go closed source, they want all inference to use that data for training runs and right now they are ceding the revenue and data flow.

Also, despite Meta being open source but not competitive anymore I think we will see some very strong open source AI labs in the U.S. start to pop up as an offset and existing models are good enough for inference providers for the forseeable future. China going closed would accelerate U.S. open source labs too.

At least these are my early contrarian musings. Thanks for tuning in!

I have no idea on OpenRouters plans. I have no ownership but love the product and think its extremely net positive for humanity.

https://t.co/tpD7AlBsM3

I get why the tech outcomes drive some people insane. I’ve joined companies 12 months “too late”, and merely made a good amount of money instead of generational wealth

The people who joined before me weren’t any better or smarter. They just got lucky. Just like someone looks at me and thinks I got lucky

The pure randomness of it all can either drive you crazy or give you an appreciation for the role of luck.

But at the end of the day you are in the driver’s seat. You choose your perspective

What I have come to learn is the people who think they alone earned their accomplishments are the most unhappy. The people with gratitude for the role luck played in their success are able to keep striving for more without losing their mind

They have come to acknowledge that while they can shape the world around them, and tilt the odds in their favor ever so slightly, ultimately a lot of it is out of their hands

I love this idea from Tobi Lutke:

“I take the view that I'm a corporate raider. That Shopify went bankrupt and I bought it on a fire sale and I'm marching in on day one, and that previous management was crazy and we need to turn this place around.”

A kid drew himself sleeping in bed between mom and dad and labeled it 'safe.'

In Japan, this exact sleeping arrangement has a name. They call it 'the river.' Mother is one bank. Father is the other. The child between them is the water. Roughly 70% of Japanese mothers sleep this way with their kids, sometimes through the teenage years. The Western model of putting a kid alone in their own bedroom is barely 200 years old. For most of human history, in most cultures still alive today, kids slept beside their parents.

James McKenna runs the Mother-Baby Behavioral Sleep Lab at Notre Dame. He spent decades watching what happens when parents and kids share a bed. The bodies sync up. Heart rates align with the parent's, breathing falls into the same rhythm, and by morning even sleep stages have started matching. The parent's body, in McKenna's words, acts as a kind of biological jumper cable for the child's.

In 2013, researchers in the Netherlands tracked 193 babies through the first year of life. They measured cortisol, the brain's main stress hormone. Babies who had spent more weeks co-sleeping in the first six months produced less cortisol under stress at 12 months. Sleeping near a parent had rewired the kid's stress system to be calmer under pressure.

Inside the kid's brain at night, the amygdala, the fear alarm, gets more sensitive as the body gets tired. Darkness makes it worse. A 2021 paper in PLoS One from Australian researchers showed that light directly suppresses amygdala activity. Lights off, alarm louder. The whole brain is wired to read 'alone in a dark room' as a threat.

Now add a parent's body to that bed. The kid's nervous system reads warm body, breathing nearby, familiar smell. The threat alarm dials down. Two parents on either side dial it down twice. The drawing is the kid's brain calculating maximum safety: I am surrounded by the people who keep me alive, and nothing can reach me without going through them first.

The arrangement in this drawing is what most of human history called 'sleeping.' Sleeping the kid alone in another room is a 200-year-old Western invention that we forgot was an invention. Every kid who has ever padded into your room at 3am and crawled into the middle of the bed is just trying to redraw the picture.

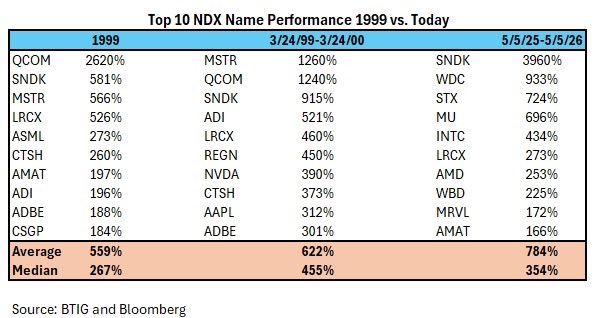

Great commentary yet again from BTIG’s Jonathan Krinsky

•Party Like It's 1999. In 1999, the best performing Nasdaq 100 stock was Qualcomm (QCOM, not rated), up 2600%. The best rolling 52-wk return for QCOM during the entire dot-com bubble was 2600%, so SNDK is beating that by 1300bps. Interestingly, the second-best stock in 1999 was SNDK up 581%.

•More Extreme. If we look at the top 10 performing NDX stocks in 1999, they were up an average of 559%. The top 10 in the year leading up to 3/24/00 were up an average of 622%. The top 10 NDX names over the last year are up an average of 784%, beating both the dot-com periods..

"Back in 1Q’20, Google Cloud was only 27.2% of AWS revenue. Six years later, it has become 53.3% of AWS revenue...I find it quite remarkable that Google Cloud may be ~70-75% of AWS size by next year."

$GOOG $AMZN

I met with the head of investment banking at one of the biggest names in IPOs

He said the public markets only want three things right now

1. Large language models - OpenAI, Anthropic, etc.

2. Defense - Anduril, Saronic, etc.

3. Physical AI (robotics and vertical integrators) - SpaceX, Figure, Zipline, Dandy, Flock, etc.

We're expanding our collaboration with Amazon to secure up to 5 gigawatts of compute for training and deploying Claude. Capacity begins coming online this quarter, with nearly 1 gigawatt expected by the end of 2026.

Introducing Claude Opus 4.7, our most capable Opus model yet.

It handles long-running tasks with more rigor, follows instructions more precisely, and verifies its own outputs before reporting back.

You can hand off your hardest work with less supervision.

What's funny is how wrong all the analogies are here. I would consider the chart already falsified. GPT-3 was *nothing* like an elementary schooler. It was a completely different form of intelligence than an elementary schooler.

Unfortunately I think we'll see meaningful layoffs in software this year. And I want to explain why it's just air cover to call them "AI-driven layoffs", even though every company will do so.

Yes, AI makes companies more efficient. Developers and marketers can do more. CSMs can have a wider span of control. You can answer 70% of your tier 1 support cases with AI. But that's not really what's going on.

But two things are more elemental to the situation, and the actual driver:

1. Valuations have reset, with a totally valid and reasonable focus on free cash flow minus stock compensation. And the math simply doesn't math.

2. Many of these companies staffed up during COVID and never actually took their medicine and got fit. They thought demand would come back and it mostly hasn't. Not in the same way.

Illustrative example, to pick on two companies, Atlassian and HubSpot, that I actually really admire:

- Age: Atlassian is 24 years old. HubSpot is 19 years old - # of employees: Atlassian has 14k employees at $22B market cap. HubSpot has 9k employees at $15B market cap

- SBC-Adjusted FCF: Basically ZERO

That's right. After 20 years, the actual cash generated and available to shareholders is ZERO

I do think the owners of these businesses understand that is no longer tenable.

But they have two issues now:

1. The actual technical talent needs to get paid

2. Their stocks are down 60-70% from recent highs

So here's the situation: They need to start making actual money, they have to pay their tech talent, their dollar grants are going to have serious dilution consequences, and their cost structures are completely bloated for their current market cap, especially compared to more nimble competitors.

If they keep paying all of these people in stock, their dilution will continue and the stocks will continue to be punished. If they pay them all in cash, they will have no fcf.

TL;DR Layoffs are unfortunately the only true answer. They are coming. They will be credited to AI, and that will be air cover for the real problem.

Figma shipped a silent patch specifically to kill figma-use — my open-source tool that did what they wouldn't: an MCP server that creates and modifies designs, JSX export, design linting. Then they scrambled to catch up with their own MCP server.

So I spent the weekend recreating @Figma from scratch.

OpenPencil: reads and writes .fig files, AI chat with full design tools, P2P collaboration with zero servers, ~7 MB app. No account, no subscription.

Three days, one developer, MIT license.

https://t.co/bPtP6JPbq0

Top-5 semicap performance in China

- down by 5% to $34.6B in '25

- AMAT share down from 47% in 2017 to 24% in 2025

- Except for Lam, everyone else declined y/y in '25

- ASML went from #5 in 2022 to #1 in 2024

- TEL, despite free run in China, declined -17%

- KLA first decline since 2018