$PSC is an exploration & development mining business focussed on battery & electrification metals across Zimbabwe and the broader sub-Saharan African region.

$PSC Country Manager Mwelwa Manda sat down with @FinInsightZam to discuss our recently upgraded Mineral Resource Estimate at the Mumbezhi #Copper Project in Zambia. Watch the full interview here: https://t.co/mtoOWSqKqz

We bid farewell to a towering figure of tradition and leadership. His Royal Highness Chief Mpezeni IV, a symbol of courage, resilience and cultural pride for the Ngoni people and the nation at large.

May his spirit rest in eternal peace, and may his legacy endure forever.

$PSC MD & CEO @SamHosack recently spoke with Financial Insight Africa at Mining Indaba 2026 on Zambia’s copper sector, local workforce development, community engagement and the long-term opportunity at the Mumbezhi Copper Project. Read more: https://t.co/2OVu170VRs

$PSC Country Manager Mwelwa Manda spoke with Clarence Chongo from Financial Insights Zambia on the recently upgraded Mumbezhi Copper Project MRE (208Mt @ 0.49% CuEq). Watch the short snippet below.

Today on #AfricaFreedomDay, we honour the resilience, unity and progress of African nations. Prospect is proud to contribute through our work in Zambia, advancing the Mumbezhi Copper Project to support, local partnerships, long-term growth and development.

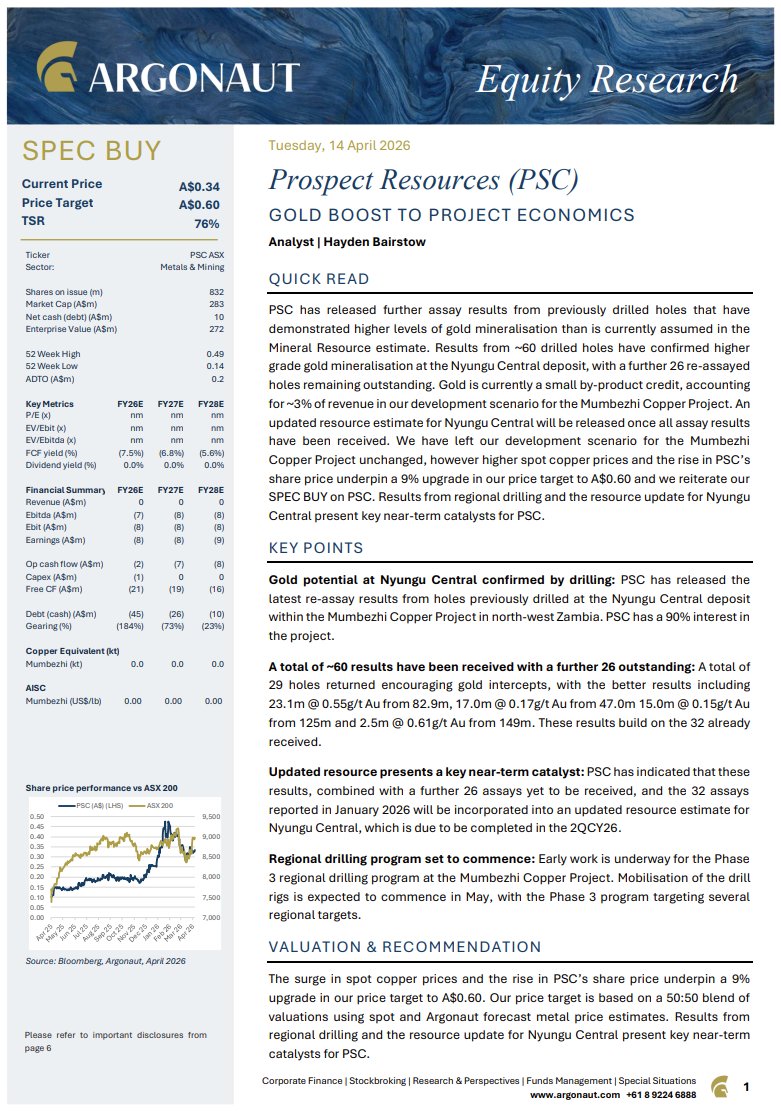

$PSC

$PSC is featured in an article by @StockheadAU , recognising the strong development potential of our flagship Mumbezhi #Copper Project. Phase 3 drilling is currently in progress at Mumbezhi. Read more here. https://t.co/WSDchQNJWS

$PSC MD & CEO @SamHosack provides video commentary on our upgraded Mumbezhi Copper Project MRE in Zambia, now 208Mt @ 0.49% CuEq, and the start of Phase 3 drilling. Thank you to our shareholders for your ongoing support as we advance Mumbezhi: https://t.co/ySXWBotPag

New research coverage highlights the growing value of the Mumbezhi Copper Project, with Argonaut increasing its $PSC price target by 17% to A$0.70 following the upgraded MRE and stronger gold credits: https://t.co/SIrnRfJt5d

Updated MRE at the Mumbezhi Copper Project has increased to 208.1Mt @ 0.42% Cu (0.49% CuEq) for 877kt contained copper, with gold resources up 106% to 262,100oz. Phase 3 drilling is now underway targeting further growth across the project: https://t.co/vBjkG6AIWY

$PSC

Phase 3 drilling has commenced at the Mumbezhi Copper Project in Zambia, with ~26,000m of diamond, RC and aircore drilling planned to target further resource growth at Nyungu Central and key regional prospects: https://t.co/3D5z5nVR1B

$PSC

On 20 April, $PSC officially handed over the Matebo Local Court in Zambia to the Government and Matebo community. The court was built and donated by Prospect, with Kalumbila DC Chair Shadrick Munjunga in attendance. A meaningful milestone supporting local access to justice.

Happy Labour Day! Today we recognise the dedication of workers across all industries and levels whose efforts continue to move the country forward. Prospect is proud to be working in Zambia and support long-term growth through our Mumbezhi Copper Project.

$PSC #LabourDay

$PSC reports further strong gold re-assay results from Nyungu Central at the Mumbezhi Project, Zambia, highlighting significant by-product potential and supporting plans for an updated MRE in Q2 2026 and upcoming Phase 3 drilling: https://t.co/mGsOfGh92m

Today, $PSC celebrates Kenneth Kaunda Day, honouring Zambia’s first president. As we reflect on his legacy of unity, resilience & progress, we remain committed to supporting Zambia’s long-term growth through the Mumbezhi Copper Project. Happy Kenneth Kaunda Day!

$PSC reports a strong March quarter, with contained copper at Mumbezhi increasing 50% to ~772kt, growing polymetallic upside and ownership rising to 90%. Well funded to accelerate drilling, resource growth and development through 2026: https://t.co/8Pbw1uCruf

Whilst there are no published academic studies that formally document systematic poly-metallic discounting of copper equities, in reality market evidence suggests that one exists.

The observation is that when by-product metals lack confirmed recovery data, market analysts face a binary choice: Model them at risk-adjusted value; or Ignore them. The reality is that most choose to ignore them.

The result is that by-product upside on projects like Mumbezhi is excluded from valuation models until testwork forces inclusion. The discount is not irrational … it is a rational response to unconfirmed data. But it creates a persistent and exploitable gap between intrinsic value and market price.

CRU formally acknowledged in its 2020 report for the International Seabed Authority that "determining a fair value for polymetallic resources is highly challenging." A 2025 Nature Communications paper demonstrated that traditional models systematically undervalue poly-metallic mine outputs, with by-product economics creating non-linear interdependencies that single-metal valuation frameworks fail to capture.

The data from M&A transactions supports this too – here’s what major producers actually paid:

- BHP paid a 49.3% premium for OZ Minerals' copper-gold-nickel assets.

- Zijin paid 57% above market for Nevsun's Timok copper-gold project.

- BHP and Lundin paid a 32.2% premium to acquire Filo del Sol's copper-gold-silver resource in 2024.

In every large copper transaction since 2010, the highest premiums went to assets with material by-product credits. Acquirers price poly-metallic inventories at full value, whereas public markets discount them until testwork resolves the uncertainty.

The re-rating catalysts are identifiable and sequenced:

- Maiden resource delivery: 30-60% valuation appreciation observed across comparable projects.

- Economic study completion incorporating by-product economics: 40-100% re-rating as projects transition from geological potential to quantified economics.

These are documented patterns across the exploration and development lifecycle.

The window is the period between by-product identification and by-product confirmation for @ProspectResLtd. That is where the gap between market price and intrinsic value is largest.

Prospect Resources notes the latest research from Argonaut Equity Research following our Nyungu Central re-assay results, highlighting stronger gold mineralisation, key near-term catalysts and maintaining a Spec Buy with a A$0.60 price target: https://t.co/VdWiU4u46i

Gold re-assays at Nyungu Central confirm widespread gold mineralisation,with intersections in 29 of 32 holes. Results support strong by-product potential (with cobalt) alongside copper.Further assays due this month; MRE update in Q2: https://t.co/dwgLhA1iC6

The real cost of adding gold and cobalt circuits: Most investors treat poly-metallic complexity as a binary - either the by-products are recoverable, or the processing is too complex to model with confidence. The engineering data tells a different story.

Adding a gravity gold circuit to a conventional copper sulphide flotation plant costs between $2 million and $10 million at typical development scale. That is 1–1.5% of total plant capex. It recovers free gold directly to doré, achieving 99% payability versus 85–93% if gold is left in copper concentrate. At $3,000/oz gold, that payability gap is worth $150–435 per ounce … every ounce, every year, for the life of the mine.

The cobalt data point is equally specific. Glencore's Kamoto Copper Company in the DRC publicly approved a cobalt debottlenecking project at $15.8 million in December 2017 … 3.6% of their $437 million base processing plant. Full cobalt product dryers added a further $49 million. These are formally published board-approved figures, not estimates.

The conclusion is direct. For a copper-gold-cobalt sulphide project, like our @ProspectResLtd Mumbezhi project, the capital required to unlock full by-product value is modest … in the range of 3–15% of total plant capex depending on product specification. Against a by-product revenue stream that can compress C1 cash costs by tens of millions of dollars annually, the return on that incremental investment is among the highest in mining.

What the market prices as processing complexity is, in most cases, a recoveries confirmation problem … not an engineering one. The circuits are standard. The reagents are proven. The cost is known.

The gap closes when metallurgical testwork publishes the recovery numbers. That is the relevant catalyst … not a change in the engineering, but a change in the market's willingness to price what the engineering already shows is achievable.