Financial planning is like driving a car withclear windshield on a rainy day. It helps you reach your destination faster and safer and navigate life's twists and turns with clarity and confidence. #FinancialFreedom@ActusDei#FinancialFitness

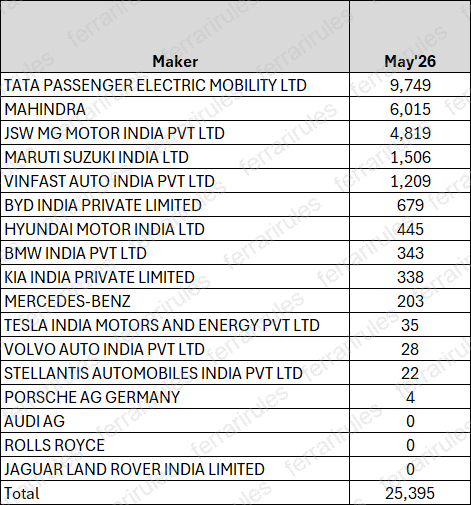

⚡️EV Sales are going to create a new ATH this month, with market share reaching 6.6%

⚡️Some Key Headlines brewing with one day to go

🚗Tata is most probably going to cross 10k EV sales

🚗Mahindra (9e, BE6, 9s) is recording its best month ever - 5646 sold to date

🚗Mahindra 3XO EV, 400 are outselling Kia - 369 vs 338

🚗Maruti has crossed 1500 sales for the EV sales

🚗Vinfast continues to do numbers beyond 1000. Thanks to 701 cabs sold in April and May combined

Two economists just published a mathematical proof that AI will destroy the economy.

Not might. Not could. Will — if nothing changes.

The paper is called "The AI Layoff Trap." Published March 2, 2026. Wharton School, University of Pennsylvania. Boston University. Peer reviewed. Mathematically modeled.

The conclusion is one sentence.

"At the limit, firms automate their way to boundless productivity and zero demand."

An economy that produces everything. And sells it to nobody.

Here is how you get there.

A company fires 500 workers and replaces them with AI. A competitor fires 700 to keep up. Another fires 1,000. Every company is behaving rationally. Every company is following the incentives correctly. And every company is building a trap for itself.

Because the workers who were fired were also customers.

When they lose their jobs faster than the economy can absorb them, they stop spending. Consumer demand falls. Companies respond by cutting costs — which means automating more workers — which means less spending — which means more falling demand — which means more automation.

The loop has no natural exit.

The researchers tested every proposed solution. Universal basic income. Capital income taxes. Worker equity participation. Upskilling programs. Corporate coordination agreements.

Every single one failed in the model.

The only intervention that worked: a Pigouvian automation tax — a per-task levy charged every time a company replaces a human with AI, forcing them to price in the demand they are destroying before they pull the trigger.

No government has implemented this. No major economy is seriously discussing it.

Meanwhile the numbers are already tracking the curve. 100,000 tech workers laid off in 2025. 92,000 more in the first months of 2026. Jack Dorsey fired half of Block's workforce and said publicly: "Within the next year, the majority of companies will reach the same conclusion."

Nobody is doing anything wrong. Companies are following their incentives perfectly. That is exactly the problem.

Rational behavior. At scale. Simultaneously. With no mechanism to stop it.

Two economists built the math. The math leads to one place.

Source: Falk & Tsoukalas · Wharton School + Boston University ·

IT Industry's First Lifeline Against AI

Fortune Headline: AI Proving Costlier Than Human Employees

Vishal Sikka: Token costs are becoming a real issue

Microsoft: Canceling Claude; moving engineers back to Copilot

Indian IT: AI Hybrid + ₹ @ 100 can change arithmetic

INSIGHTS:

First Cracks in the AI Story

a. In recent months, Anthropic’s AI agentic tool Claude sparked a massive selloff in SaaS and IT services stocks, erasing hundreds of billions in market value.

b. On May 22, 2026, Fortune magazine has published an article which says that recent corporate reports are “exposing AI’s real cost problem.”

c. Microsoft has begun cancelling most of its Claude Code licenses, moving thousands of its developers, project managers, and designers back to using its in-house GitHub Copilot CLI.

d. Microsoft isn’t alone. Uber’s CTO said the firm had already burnt through its entire 2026 AI coding budget in just 4 months (Jan to Apr). Meta, Amazon and other tech firms pushing for max use of AI tokens too face the same dilemma.

e. Fortune article says: “These reports may throw cold water on the bets tech industry has placed on AI. While some cling to the promise of an “AI revolution,” the cost of adoption is proving a stubborn bottleneck.”

f. Highlight Line for IT Services: “The economics of replacing or augmenting human labor with AI may be more complicated than some early forecasts originally implied.”

g. Earlier today, Dr. Vishal Sikka posted the Fortune article on his X account with these comments: “Token costs are becoming a real issue. In the weeks/months ahead, I expect more scrutiny of AI usage.”

h. Goldman Sachs recently forecasted that agentic AI token consumption could increase 24x by 2030. So, even if the cost-per-token will fall sharply, aggregate costs will rise.

g. AI compute, inference, energy, and tooling costs (including AI native expert costs) are not going to zero. Just as broadband internet or electricity never became free despite massive improvements in efficiency and scale.

h. Jevons Paradox: As more AI use cases emerge for individuals and businesses, the increased token consumption will outpace falling unit costs.

i. Citing Pew Research polls, Harvard’s Gazette reported last month that public opposition is rising over the large water & electricity demands that data centers impose on communities, while creating almost no new jobs. (1.4 GW Data Center = electricity for a million US homes.)

Indian IT Cost Modeling

Here’s a rough back-of-the-envelope calculation:

The Human Cost

The current cost of a mid-level Indian IT developer is ₹950 per hour (including salary plus fixed & operational overheads).

At the exchange rate of ₹95, this engineer costs the company $10 per hour.

If the exchange rate is ₹100, the cost goes down to $9.50 per hour.

The AI Multiplier

Now train this IT developer on enterprise AI tools. This won’t replace the developer, but it will make him twice as efficient (2x multiplier). So, he can now finish 2 hours worth of work in 1 hour.

Therefore, cost per hour drops to $4.75 (half of $9.50)

Cost of AI Tools

Indian IT companies have to rent AI models from the US. Assume that the cost of AI tooling is $6.25 per hour for every IT engineer using the system.

Total Cost of Operation

$4.75 + $6.25 = $11 per hour

This is the “Indian AI-Augmented Model” @ $11 per hour

Who Wins the Global Price War?

100% AI Model in the US (with high AI native expert salaries, AI token costs, data center power costs, and local overheads & taxes) may cost $15 to $20 per hour.

An India IT firm can deliver the same high-tech AI-driven work at an internal cost of $11 per hour.

Weak ₹ as a Tactical Weapon

With every ₹1 depreciation against the US dollar, an Indian IT export firm’s operating margin expands by 30 to 50 bps (0.3 to 0.5%).

The way China intentionally undervalued its currency for years to dominate world trade, India must also learn to weaponize the rupee to its advantage.

If cracks indeed begin to emerge in AI frontier model cost economics, it will be time for India to go on the offensive and fight the IT & GCC service exports battle on the front foot.

@arabicatrader

Top Economists Say Let the Rupee Fall

Arvind Subramanian: 100 is almost necessary

Arvind Panagariya: Overcome the psychology of 100

Raghuram Rajan: Let ₹ find its level

Gita Gopinath: Let ₹ do its job

D Subbarao: Let the ₹ fall

Will RBI defend or is 100 coming?

INSIGHTS

Government’s Position

Dr. V.A. Nageswaran

Chief Economic Advisor, GOI

May 12 / April 24

Stopping the rupee from falling further is one of the “central macro-economic imperatives” of FY27. India’s rupee is fundamentally “undervalued” (so investors should “buy” it.)

RBI’s Interventions

Reuters, May 20

Reuters spoke to four different bankers (names withheld), who said that RBI’s daily currency market intervention is $1 billion (estimated). This is slowing, but not halting the rupee’s slide.

The RBI has been selling dollars every day in the past 10 days to relieve the pressure on the rupee, the bankers said. This has moderated the pace of losses, but not reversed them.

What the Economists Say

Dr. D. Subbarao

Ex-RBI Governor, Top Economist

May 20 / May 13

When you defend the rupee, the danger is not merely depletion of reserves; it is the credibility trap. If RBI interventions fail to arrest the rupee’s fall, market confidence can evaporate abruptly.

A failed defence is worse than no defence. Exchange rate crises are not pretty. At heart, they are a crisis of confidence.

If the fundamentals dictate the rupee should fall, then the RBI should let it fall. A weaker rupee is going to improve our export competitiveness.

Dr. Arvind Panagariya

Ex-Chairman, Finance Commission

Ex-VC NITI Aayog, Top Economist

May 21

Dear RBI, do not let the psychology of 100 per dollar determine your policy response. The right response at the moment is to let the rupee depreciate.

Trying to defend the rupee will continue to bleed the reserves until they are exhausted. Even NRI bonds are like band-aid. You will eventually have to cross the psychological barrier of 100.

Dr. Gita Gopinath

Ex-Chief Economist, IMF

May 21 / May 18

Currency depreciation forces you to cut back on imports (i.e., reduce your oil consumption, which is anyway the government’s goal.) If you try to intervene, all that happens is you lose your reserves. Let the rupee do its work.

Dr. Arvind Subramanian

Ex-Chief Economic Advisor, GOI

Dec 29, 2025

Allow the rupee to gradually decline by 10% over the next few months. To catch up with Chinese export competitiveness, the rupee at 100 to the US dollar seems almost necessary.

Dr. Raghuram Rajan

Ex-RBI Governor, Top Economist

Jan 25, 2025

There is no need to be overly concerned about the rupee’s big slide. I would let it find its level. Maybe some additional depreciation is useful for Indian exports.

ENDQUOTE

“Recognize reality even when you don’t like it. Especially when you don’t like it.” – Poor Charlie’s Almanac [Charlie Munger]

@arabicatrader

The future of power is not Solar vs Wind vs Thermal vs Nuclear.

It is Solar + Storage + Thermal Backup + Nuclear + Wind.

India's energy demand is too large for a one-source solution.

Here is the data point that proves it.

On 25 April 2026, India hit an all-time peak power demand of 256.1 GW. At that exact hour, solar contributed 24% (58.2 GW) and coal contributed 66% (173.3 GW). Same grid. Same hour. Both essential.

India's electricity demand is now too large, too seasonal, too industrial and too time-sensitive for any single source to solve alone. The opportunity is not in picking the winner. The opportunity is in understanding how the entire stack fits together.

Here is the full power stack and what it actually means for investors.

India had 150.26 GW of solar capacity as of March 2026. FY26 solar addition stood at a record 44.61 GW, almost double the previous year.

Solar is the cheapest and fastest source to build.

Typical tariff: ₹2.40 to ₹3.00 per unit

Typical PLF: 18% to 24%

Construction time: 9 to 18 months

Main cost driver: modules, cells, inverters, land and evacuation.

But solar has one limitation that does not go away with scale.

It generates when the sun is available.

India’s evening peak does not disappear after sunset.

So solar reduces the cost of energy, but it does not solve reliability on its own.

👉Company Associated: Waaree Energies, Premier Energies, Vikram Solar, Adani Green, NTPC Green, Tata Power, Borosil Renewables, KPI Green, Solex Energy.

🔹 Wind:

India had 56.09 GW of wind capacity as of March 2026. FY26 added 6.05 GW, the highest ever in a single year.

Wind is not as cheap or fast as solar, but it improves renewable diversification.

Typical tariff: ₹3.00 to ₹3.70 per unit

Typical PLF: 25% to 35%

Construction time: 18 to 36 months

Main cost driver: turbines, towers, logistics and wind site quality

Solar generates mainly during the day. Wind can generate across different seasons and hours.

Pure solar grids face midday surplus and evening deficit.

Wind smooths that curve.

👉Company Associated: Suzlon Energy, Inox Wind, Inox Green Energy Services, KP Energy.

🔹 Storage: The missing layer

This is where the next decade gets interesting.

India has 7.2 GW of pumped storage operational and 11.6 GW under construction.

BESS has around 13 GWh of committed projects under VGF, scaling towards a CEA target of 47 GW battery storage + 27 GW pumped storage by 2032, or around 411 GWh total storage capacity.

Storage has no “PLF” like generation assets. Its key metric is duration, dispatchability and cycle efficiency.

Battery storage works best for short-duration peak shifting, usually 2 to 4 hours.

Pumped storage works better for large-scale grid balancing and longer duration support.

The Ministry of Power now mandates 2-hour storage equivalent to 10% of solar capacity in new solar tenders.

Storage is no longer optional.

It is becoming policy.

👉Company Associated: Exide Industries, Amara Raja Energy, HBL Engineering, NTPC, JSW Energy, NHPC, SJVN, Tata Power, Torrent Power, L&T.

🔹 Thermal: The reliability backbone

Here is the number that breaks intuition.

India has around 222 GW coal and lignite capacity, but at the April 25 peak, coal supplied 66% of power despite holding only around 42% of installed capacity.

For Q4 FY26, coal contributed around 73% of total electricity generation.

This is because installed capacity and actual generation are two different things.

A 1 GW solar plant does not generate like a 1 GW coal plant.

Typical tariff: ₹4.00 to ₹5.50 per unit

Typical PLF: 55% to 70%

Construction time: 4 to 6 years

Main cost driver: coal, transport, boilers, turbines and emission control

Solar is cheaper, but coal is dispatchable.

Coal plants can generate through the night, during cloudy periods, weak wind cycles, seasonal hydro shortfalls and evening peaks.

That is why India plans to add 80 GW of new coal capacity by FY32 even while pushing renewables aggressively.

Thermal is not disappearing.

Its role is changing from only base-load generation to backup, balancing and reliability support.

👉Company Associated: NTPC, Adani Power, Tata Power, JSW Energy, CESC, Coal India, BHEL, Thermax, Power Mech Projects, ISGEC Heavy Engineering.

🔹 Nuclear: The clean base-load option

India has only 8.78 GW of nuclear capacity today, but the target is 100 GW by 2047.

Nuclear is the smallest piece today, but possibly the most strategic over the next 20 years.

Typical tariff: ₹3.80 to ₹7.50 per unit

Typical PLF / availability: 80% to 90%

Construction time: 8 to 12+ years

Main cost driver: upfront capex, safety systems, specialised equipment and long execution cycle

Solar is variable.

Wind is variable.

Storage is duration limited.

Thermal has emissions.

Nuclear gives clean round-the-clock power.

The Prototype Fast Breeder Reactor at Kalpakkam achieved first criticality on 6 April 2026, with commercial generation expected by September 2026.

The government has committed ₹20,000 crore to the Nuclear Energy Mission, opened the sector to private players, and large groups like Tata, Reliance, Adani, JSW, Jindal and Hindalco have submitted bids for Bharat Small Reactors.

SMRs are being positioned for steel, aluminium, data centres and green hydrogen.

All of them need clean 24x7 power.

👉 Value chain: L&T, BHEL, MTAR Technologies, Walchandnagar Industries, HCC, Bharat Electronics.

🔹 Transmission: The silent capex cycle

Everyone watches generation.

Almost nobody watches the wire.

India’s transmission network crossed 5 lakh circuit kilometres in January 2026 and needs to reach 6.48 lakh ckm by 2032.

Transformation capacity must grow from 1,407 GVA to 2,342 GVA.

Inter-regional transfer capacity must rise from 120 GW to 168 GW.

Total transmission outlay is estimated at ₹9.15 lakh crore by 2032.

Every GW of solar in Rajasthan and every GW of wind in Tamil Nadu is useless without the grid to carry it to Mumbai, Bengaluru, industrial corridors and data centre clusters.

👉 Value chain: Power Grid Corporation, Hitachi Energy India, GE Vernova T&D India, Siemens, ABB India, CG Power, Transformers and Rectifiers, Voltamp, Shilchar Technologies, Apar Industries, Polycab, KEI Industries, RR Kabel, Skipper, Kalpataru Projects, KEC International, Techno Electric.

The question is not "which energy source wins". The question is "who supplies the components that every source needs".

1. Solar needs modules, inverters, cables, transformers. 2. Wind needs turbines, towers, blades, gearboxes.

3. Storage needs batteries, power electronics, EPC.

4. Thermal needs boilers, turbines, emission control, fuel.

5. Nuclear needs reactors, heavy fabrication, precision components. All of them need transmission, switchgear and the grid.

The most resilient bets in the next decade may not be on a single generation theme. They may be on the picks-and-shovels that every theme depends on, regardless of which source wins the next tender.

India is not transitioning to renewables. India is layering renewables on top of an expanding thermal base, adding nuclear underneath, wrapping the whole thing in storage, and binding it together with transmission.

That is the power stack worth building a thesis around.

📌Disclaimer: For educational purposes only. Not a buy or sell recommendation.

@JSPWorks have you not read other party manifesto? or did you read west bangal manifesto ? it's all over the country trend n not TN alone as you presented

@nehanagarr it shows your lack of understanding of state level politics - it's about what people think , as the same peopl in 2021 gave huge victory - do not generalize with manifesto many don't even know

India's defence budget crossed ₹7.85 lakh crore this year. 75% of capital acquisition is locked for domestic companies only.

But most investors stop at HAL, BEL, Mazagon Dock. These are assemblers. The missile itself is built by a completely different set of companies.

A quick breakdown of who actually builds India's missiles:

BrahMos went from 15% Indian-made components in 2015 to 70% today. Target is 85% by end of 2026. New Lucknow plant takes annual production from 100 to 300 units. Export pipeline is building towards ₹5 lakh crore by 2030. $450 million in export orders already signed.

Every one of those 300 missiles needs seekers, boosters, titanium forgings, guidance electronics.

Here's who supplies what:

Bharat Dynamics (BDL): India's sole missile manufacturer. Akash, Astra, MPATGM. Order book ₹26,000 crore. Two new plants coming in Telangana and UP.

Data Patterns: Developed the Fire Control System for BrahMos. Testing seekers. All-time high order book at ₹1,868 crore. EBITDA margins 35-40%. Revenue growth guidance 20-25% CAGR.

Astra Microwave Products: Builds RF and infrared seekers. Executing 70% of the QRSAM missile programme. Order book ₹2,226 crore. Q3 FY26 EBITDA margin hit 31.7%, highest in 8 quarters. 95% of new orders from defence.

Solar Industries: Made the transition from mining explosives to missile propulsion. Supplies solid propellant boosters for BrahMos via DRDO tech transfer. Also making Pinaka rockets and 155mm ammunition. Defence order book alone is ₹16,600 crore.

MTAR Technologies: Precision components for liquid propulsion engines and Agni missile programme. Q3 FY26 revenue up 59% YoY. Profit up 117%. Order book ₹2,395 crore.

PTC Industries: Titanium and superalloy castings for BrahMos, Pralay missiles, and now Blue Origin and Honeywell Aerospace. 9-month FY26 revenue up 95%. Building titanium capacity to 6,000 TPA. Management targeting 10-15x revenue growth over 5-7 years.

Premier Explosives: Akash missile propellants. Long-term contract with BDL. Quiet but locked in.

Goodluck India: Steel and alloy forgings for Pinaka rockets and BrahMos components.

DRDO conducted the first salvo launch of the NASM-SR anti-ship missile this month. Goldman Sachs projects the Indian defence market to grow 6x to ₹10 lakh crore over 20 years.

The assemblers get the headlines. The supply chain gets the orders.

Educational only, not a recommendation.