Meet my mascot @fastxyz - a demon.

When working on the design, I wanted to create not just a picture, but a character with character. He is the embodiment of audacity and intelligence. He was born in the very heart of the infinite number π². When the numbers began to square, there was so much energy that it took shape. Now he is here to monitor the order in calculations and a little troll those who are afraid of complex tasks.

His mission is to simplify the complex, but keep it professional. He does not respect boring rules, but is fanatical about elegant solutions. His audacity comes from knowledge: when you know exactly the result of the equation, you do not need to prove anything to anyone. 😈

Meet pryanik.pie — my onchain agent on @pieverse_io.

Wallet, skills, deployed in Telegram. Took about 60 seconds.

https://t.co/vPOZ50crud

@pieverse_io@pieverse_agent0

Last week’s ETF flows showed a clear divergence across crypto assets.

$BTC ETFs recorded $1.039B in net outflows, ending a six-week inflow streak. $ETH ETFs were weaker, with net outflows in all five trading days and a total weekly outflow of $255M. From a flow perspective, the main pressure was concentrated in the two largest assets. Yet SOL ETFs pulled in $58.12M and XRP ETFs absorbed $60.50M.

Flows and prices together suggest that market preferences were being repriced rather than broadly withdrawn.

The divergence tells a story worth unpacking.

Macro is the primary culprit behind the reversal. The Iran war continues to drive energy prices higher, the Strait of Hormuz remains disrupted, and ECB chief economist Philip Lane last week explicitly flagged that the oil shock "may well require" rate hikes. A Bloomberg survey now prices two ECB hikes in 2026 — June and September. Meanwhile, anticipation around Waller taking over at the Fed is adding another layer of hawkish uncertainty, with markets beginning to reassess the pace of any resumed balance sheet reduction. Two major central banks leaning tighter simultaneously is exactly the kind of environment that prompts institutional risk reduction in assets like BTC and ETH first.

But SOL and XRP bucking the trend tells a different story. Their inflows are being driven by crypto-native logic, not macro allocation. XRP continues to attract pre-positioning around the CLARITY Act's expected progress — regulatory certainty is a catalyst that doesn't care about ECB rate paths. SOL's recovery looks more like mean-reversion buying after weeks of overselling. Neither asset is responding to the same demand signals as BTC and ETH, which explains why they can diverge when macro headwinds build.

Core view: the ETF outflows have now been confirmed in price. BTC has broken below $77K. ETH has broken below $2,200. Flows and price are now moving in sync to the downside. AUM still holds at $104B, but continued macro pressure will test that floor. The key variables ahead: if the ECB hikes in June and Waller signals renewed tightening, reclaiming $80K becomes a heavier lift. If geopolitics ease and oil retreats, flows return. Right now, bears have the momentum.

The divergence persists: macro-sensitive money is reducing BTC exposure, regulatory-driven capital stays in XRP, SOL catches an ecosystem bid. ETH is still waiting for its own narrative — and the cost of waiting is showing up in the price.

Short-term disruption or trend shift? Drop your take 👇

#Bitcoin #Ethereum #XRP #Solana #CryptoETF #MacroCrypto #BTC #ETH

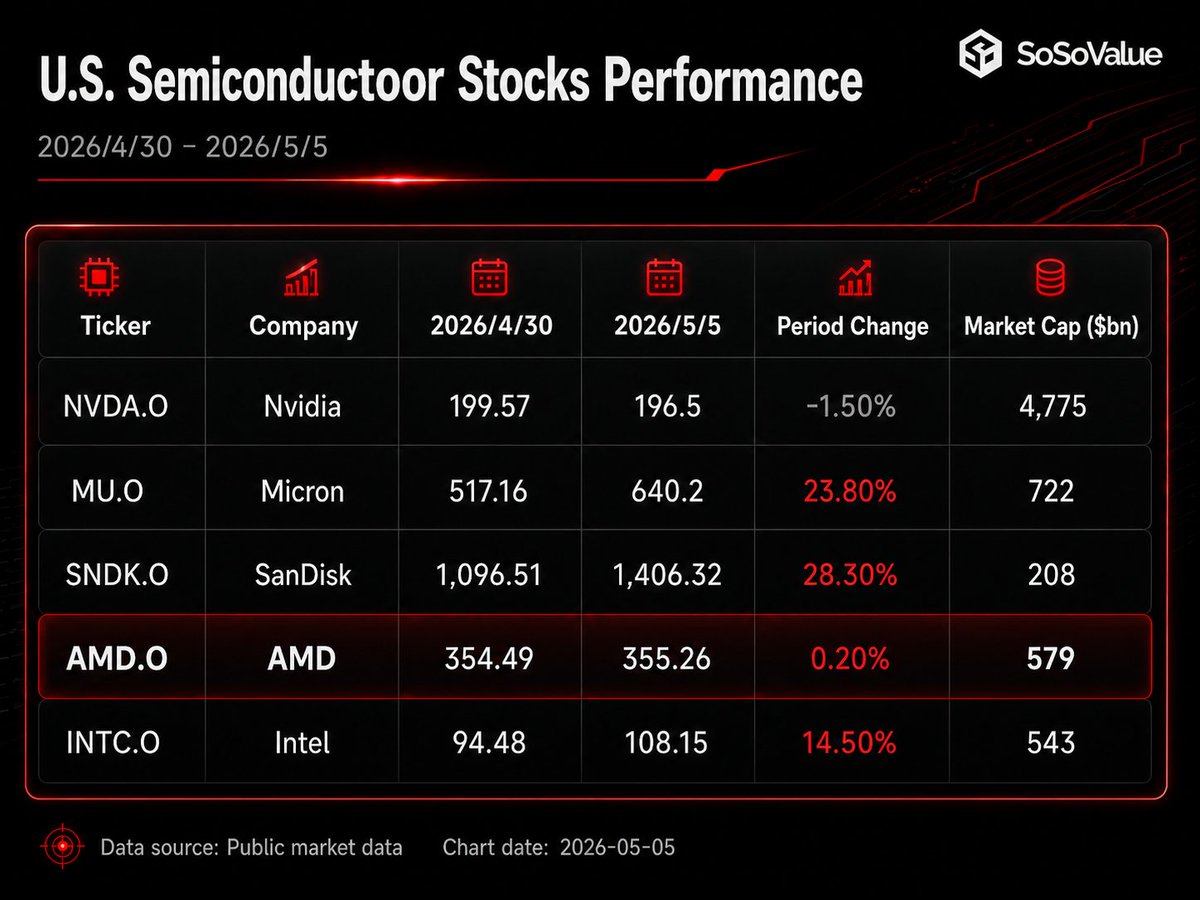

🚨SoSoValue Flash: Hormuz Skirmishes Ignite Noise, AI Shifts into "Seesaw" Mode

💥 Core Catalyst: Truce Extensions & Tehran ShadowsA direct military flare-up occurred as Iran accused the U.S. of striking a tanker, triggering IRGC retaliation against warships followed by U.S. counterstrikes. However, Trump maintains that the ceasefire holds, and Washington’s "self-defense" framing signals a lack of appetite for full-scale escalation, containing the macro fallout.

🔍 Key Logic Shifts:

1️⃣ Geopolitics: Local skirmishes pushed Brent back above $100, injecting fresh anxiety into the 14-point deal narrative. Yet, as long as both sides signal restraint, the damage to global risk appetite remains localized rather than systemic.

2️⃣ Macro Policy: Japan is suspected of a third FX intervention raid near ¥4.68T. Repeated yen-defense measures are steepening the odds for a June BOJ rate hike, adding pressure to global carry trade dynamics.

3️⃣ AI & Earnings: AI remains the undisputed engine, but internal rotations have begun. After an explosive rally, Memory and CPU players are seeing profit-taking, while NVIDIA and software laggards are catching a bid. Consolidation looms as the market gauges the "post-earnings" narrative.

📊 Trade Setup (SoDEX Assets to Watch):

Core: $USTECH-100 | $CL (Crude) | $XAUT | $BTC

MAG7: $NVDA | $AMZN | $GOOGL | $META | $MSFT | $TSLA | $AAPL

AI Hardware: $SNDK | $MU | $AMD | $INTC

🚨AMD's Second Act: From GPU Challenger to AI Infrastructure Duopoly

AMD reported Q1 2026 results with revenue of $10.25B (+38% YoY), ahead of the $9.84B consensus; Non-GAAP EPS of $1.37 (+43% YoY), also beating expectations. GAAP net income came in at $1.38B (+95% YoY); Non-GAAP net income reached $2.27B (+45% YoY), with Non-GAAP gross margin at 55%. Free cash flow hit a record $2.6B for the quarter, more than tripling year-over-year.

On the surface, the financials were a modest beat across the board — but AMD stock surged more than 18% in after-hours trading, briefly topping $410. The numbers alone don't explain the move. What does: CEO Lisa Su's forward guidance. Su stated that the server CPU TAM will double to $120B by 2030, that annual data center AI revenue is on track to reach "tens of billions of dollars," and reaffirmed a long-term Non-GAAP EPS target of over $20.

⚡️Core Theme: Data Center Takes the Wheel

Data Center revenue reached $5.78B, up 57% YoY, crossing the halfway mark of total company revenue and becoming the primary driver of both top-line and earnings growth — powered by the dual engine of EPYC server CPUs and Instinct GPUs.

The market's historical read on AMD's AI thesis was straightforward: can MI300/MI350/MI450 take share from NVIDIA? What this quarter's management commentary reframes is that agentic AI and inference workloads are driving a significant uplift in CPU demand as well. AI clusters don't just need GPUs for training and inference — they require substantial CPU capacity for orchestration, data preprocessing, head node management, and parallel task scheduling. AMD's advantage is now expanding from a single-point GPU play into a compound architecture: EPYC + Instinct + Helios, together.

Critically, CEO Lisa Su raised AMD's server CPU TAM outlook significantly: the addressable market is now expected to grow at over 35% annually, reaching more than $120B by 2030 — effectively doubling the prior forecast of ~18% CAGR and a ~$60B TAM.

🌞Product Pipeline: MI450 / Helios Enter the Visible Order Cycle

On the AI accelerator front, AMD confirmed that MI450 series GPUs have begun sampling with lead customers, and Helios rack-scale AI systems remain on track for production shipments in H2 2026. Su noted that customer demand forecasts for MI450 and Helios have already exceeded AMD's original 2027 plans, with new customers now in discussions for large-scale deployments — including additional multi-gigawatt opportunities.

More significantly, AMD raised its confidence in 2027 data center AI revenue: management expressed conviction in achieving tens of billions of dollars in annual data center AI revenue in 2027, ahead of the prior long-term target of greater than 80% CAGR.

On the hyperscaler side, the order book is becoming concrete: OpenAI and Meta have each committed to deploying 6GW of Instinct compute; Oracle plans to launch the world's first publicly available AI supercluster powered by 50,000 MI450 GPUs in Q3. Taken together, these three commitments are moving AMD's status as "AI compute's second source" from narrative to reality.

Q2 Outlook: Above Expectations, Data Center Continues to Accelerate

AMD guided Q2 revenue to approximately $11.2B (±$300M), meaningfully above the $10.5B consensus, representing roughly 46% growth YoY and 9% sequentially. Non-GAAP gross margin is guided at approximately 56%. Server CPU is expected to grow more than 70% for the full year, with both data center AI and server businesses projected to deliver double-digit sequential growth.

📈Bottom Line

This quarter isn't just another beat. The on-track delivery of MI450 and Helios has moved AMD from "potential NVIDIA alternative" to "confirmed co-anchor of AI infrastructure."

The after-hours surge to above $410 implies roughly 30x that $20 long-term EPS target — the market is pricing it in today. Notably, AMD had gone virtually nowhere over the prior three sessions, with tonight's after-hours move catching it up to Intel's recent gains. The capital rotation story isn't complicated: last Friday, Western Digital's blowout earnings ignited a fresh AI hardware rally, with funds rotating out of NVIDIA into memory and CPU names — Western Digital and Micron gained 28% and 24% respectively over three sessions, Intel added 15%, and AMD's earnings tonight became the final piece of that rotation trade.

Looking further out, the key variables are whether MI450 and Helios ship on schedule, whether the Meta and OpenAI deployments convert into durable multi-year order flow, and whether EPYC can continue capturing share as AI-driven CPU demand structurally expands.