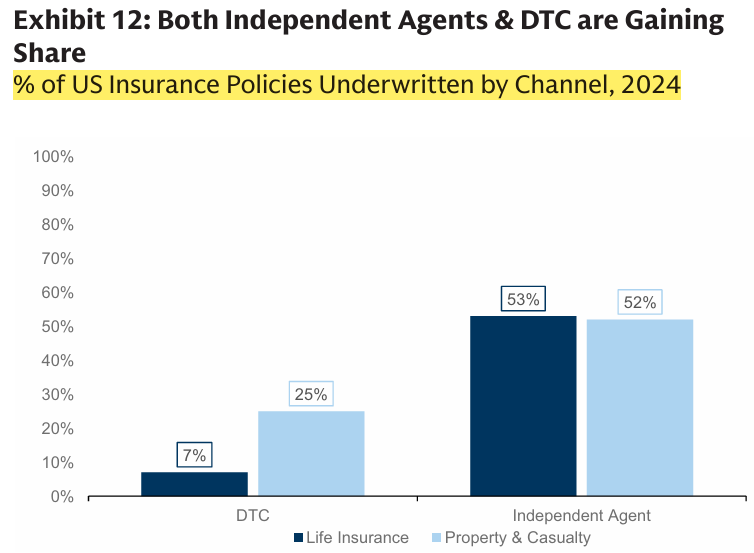

@CedarStResearch I found that $LIFE is providing tech stack to these independent agents against certain % of the written premiums but not sure about other players.

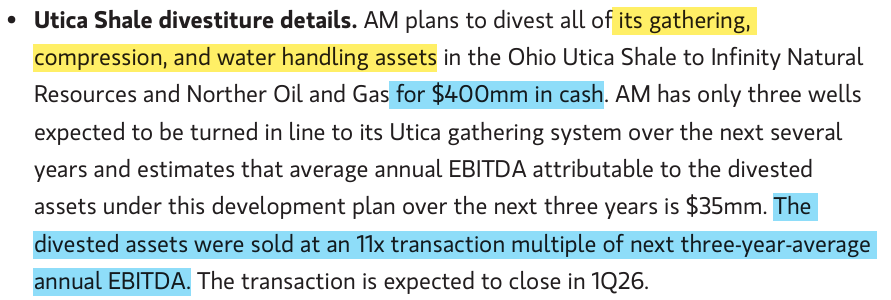

$AM announced to divest its Produced Water handling assets for $400m cash to $INR at 11x EV/EBITDA multiple.

vs. $WBI is trading at 9x multiple currently.

If common shares of $OPITQ are going to be cancelled at the end of the bankruptcy process, why are they still trade on pink sheets and have some value? The NPV of zero is zero.

Is there a scenario where there could be some equity in the new entity for current shareholders?

"Trick of the trade in insurance is how do I originate premium, retain as much of it as I can and cede all the difficult risk back out to the reinsurance market so I can transfer all my earnings volatility to reinsurers."

Pure gold from @CedarStResearch

@JavierBlas@opinion@grok, list the companies leading, who are first movers, or who have an advantage in the area described above, regarding recovering more than 15% of the shale oil in place. Symbols and prices.

On future CapEx and ROI, he said:

“So you're talking about $700 million or $800 million of capital, and we would do that at a really attractive return level (of around 30%)"

Management mentioned similar return in Q3'25 earning call. $WBI

Source: https://t.co/XTJbrpmel2

At WTI $150, an E&P company operating in Permian Basin may not able to pump oil out of the ground despite having the capital, plant, people, oil gathering pipeline if they don't have a way to dispose off the Produced Water(PW).

PW is THE limiting factor, NOT the oil price. $WBI

“We wanted to be able to take our story out, educate the market and show how this is really a superior asset to what exists today and show how it has tremendous long-term growth with great barriers to entry,”

$WBI