Build'n Stablecoin POS for Merchants 🤹 @spendcodes

Not Big Short Michael Burry 📉

Not Bishop Curry of Duchess Markle 🇬🇧

Curry like #30 🏀 NYCMarathon '24 🏃

3B+ Meta, Cash App users get Stablecoin Wallets in 2026 | MPE 2026 Berlin

Michael Curry from Spendcodes discusses how Stablecoins are quietly going live & the emerging dynamic that is driving the transformation.

#stablecoins#merchant#merchantservices#fintech@CashApp@Meta

"The most durable infrastructure companies don't wait for external developers to validate their tech. They build the application themselves first — on top of their own rails — and use it to prove out the capabilities they're asking others to build on."

This Exactly. @tokendispatchhq just posted "The Second Attempt" about Meta putting stablecoins into WhatsApp, Instagram, & Facebook.

Customers choose apps.

App developers are choosing Stablecoins...

Finally getting to this, but I take the other side from @pitdesi and @NikilKonduru:

Merchant acceptance is important for stablecoins, even in the US.

(Long post, with tl;dr at the bottom)

But building a good merchant acceptance product does not mean building your own two-sided network or trying to end-run the card networks, as Nikil and Sheel suggest. That is certainly a fools' errand. Stablecoins have no killer consumer benefit that would drive people to prefer stables over cards.

Building merchant acceptance just means building the ability for POS systems to accept direct payments from stablecoin wallets, in a single tap.

This was the issue we had at @GooglePay: credit cards are so sticky in the US because they're great.

They're:

- easy to use

- let you purchase on credit if you don't have the cash

- connect to your bank account

- give you good rewards (sometimes)

- let consumers dispute transactions

- insure you against fraud and loss

However, the stablecoin bet is that more and more dollars at rest are increasingly going to be tokenized. (As are other assets - stocks, money market funds, bonds, loans, etc.)

But credit cards are also:

Dumb (or rather, analog). Because txn's aren't programmable, they won't let the user set preferences or decide in-the-moment how they want to pay for something:

- direct debit?

- put on credit? split into four payments?

- liquidate a certain asset for a big txn?

As assets (including money) all become machine-readable (ie: tokenized) people and businesses will increasingly be able to set rules using natural language LLMs for how transactions should net out against their finances.

Why would consumers prefer this?

- smart application of rewards programs based on the transaction type

- no more credit limits: if your card maxes out at $10k, you can still make a $15k purchase with stables if all your assets are tokenized and can collateralize the purchase

- don't have to worry about paying the card off or checking your statement; preferences can be pre-programmed

- programmable -> new features can be built directly into POS payments, like splitting a lunch bill between multiple people and allocating tax and service charges

---

The big friction between where we are now and good stablecoin merchant acceptance is the user journey.

Credit cards are super easy to use: you don't even have to swipe anymore, you just tap-to-pay.

People in the US are increasingly leaving their physical cards and wallets at home, and just using their phones for T2P. Which is good for stablecoins: As Android and Apple open up their NFC, more smart POS providers will build NFC-readable stablecoin wallet apps. That is how POS systems build functionality to debit from stablecoin wallets directly.

That is the 'killer app' to make T2P from a stablecoin wallet a completely indistinguishable experience from a credit card.

---

That said, rewards are still a big missing component. It's hard to sell any consumer on saying goodbye to their airline miles.

Smart payment products (@PayPal? @CashApp?) need to figure out how to recreate rewards programs that speak to a new generation of consumers (moving beyond airline and hotel points), offering merchants a way to easily accept stablecoin txns at POS using T2P for 1.5% or 2% instead of 3% or 4% txns fees.

That is a material adoption challenge that people (wrongly) try to wave away sometimes.

---

I think for this reason that merchants and corporate payors will be faster to adopt stablecoin T2P or POS payments than consumers: their transactions are larger, they're more predictable (recurring monthly billing), and they're often more complex.

They also require more features like smart expensing, intelligible transaction strings, memos, and machine readable receipts.

---

I don't think this is a threat to @Visa or @Mastercard (which Nikil implied). I believe the opposite: you can see both of these networks starting to experiment with stablecoin settlement and payments.

I think the opposite is actually true: you'll have plastic debit and credit cards that sette in stablecoins.

But these cards will be unnecessary. And moving through fiat will be unnecessary.

Merchants will settle and hold funds in stables and users will pay in stables, making the conversion to fiat superfluous.

Some benefits to the card networks here:

- CC txn's are normally a long journey, involving multiple vendors: initiation, authorization, clearing, settlement, funding.... Stablecoin-to-stablecoin transactions collapse a lot of those functions into one and simplify, giving the networks an incentive to push more of their txn volume to stables.

- It's easier to incorporate anti-fraud rules like biometrics (for mobile T2P) and behavioral signals (eg: one-off big purchases or geo-tagging) into machine-readable transactions like stablecoins, giving the issuers an incentive to push consumers to stablecoins, since they are normally the party that bears liability for fraud loss.

---

So, tl;dr -

1. Merchant acceptance for stables is important

2. It won't end-run the networks. Rather, it will come from POS providers first and then the card networks will become the key settlement providers.

3. "Why would consumers switch?" is still the biggest question, but the rise of mobile payments and T2P will play a big role.

4. Corporate payors will adopt before consumers.

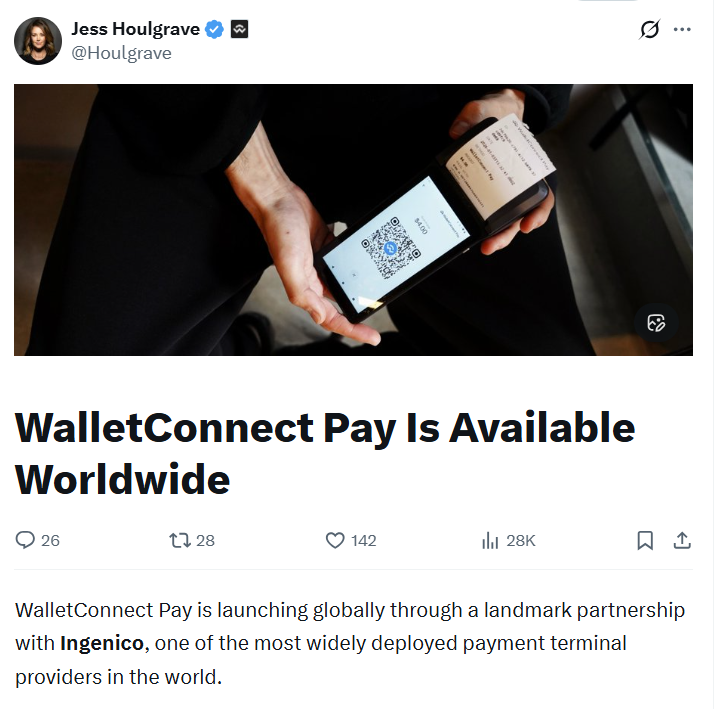

CFBR - 👏 Congrats @Houlgrave on the @ingenico partnership! Seeing native stablecoin rails reach the terminal level is a massive milestone for those of us building in the 'Wallet to Merchant' space.

These rails aren't just "future tech"—they are a superior experience and settlement reality today. Excited to watch the market reaction as this rolls out in the wild! We’re just getting started...

Two years ago, while in Berlin, I decided to shift focus and build for two years ahead... Today, I’m honored to be invited back to Berlin to speak at Europe's biggest Merchant conference with thought leaders I admire to talk about Stablecoins, user + builder adoption, and the future of retail.

To my friends and conference colleagues in Chicago, Berlin, Mexico City, New York, and beyond… Looking forward to reconnecting. Let's onboard the world!

#MPE2026 @mpecosystem

🚀 TOP voices in payments at #MPE2026

Meet the leaders shaping the future of merchant payments — live in Berlin this March.

🎤 Yousra Pesquet

🎤 Mark Beresford

🎤 Ed Adshead-Grant

🎤 Michael Curry

🎟️https://t.co/aWxo3PWj8P

As a further point on this topic, the crypto industry should 100% be talking to all the major retailers (@amazon, @Walmart, @Target, etc.) as this is yet another extension of banks weaponizing regulations to destroy the business model of actual sellers.

1/ How Banks Learned To Stop Worrying And Love Stablecoins—When we announced Libra, the reaction from the global financial establishment was, to put it mildly, "energetic"...

3/ If you could hold a digital dollar on your phone that moved instantly, why would you keep your money in a checking account that pays zero percent, charges fees, and effectively closes for the weekend?

Cash App, MetaMask Mobile, and the Base app (Coinbase Wallet) will bring the combined mobile Stablecoin user base up to 100 million+ in 2026.

Interested in the future of payments and rewards? 👇