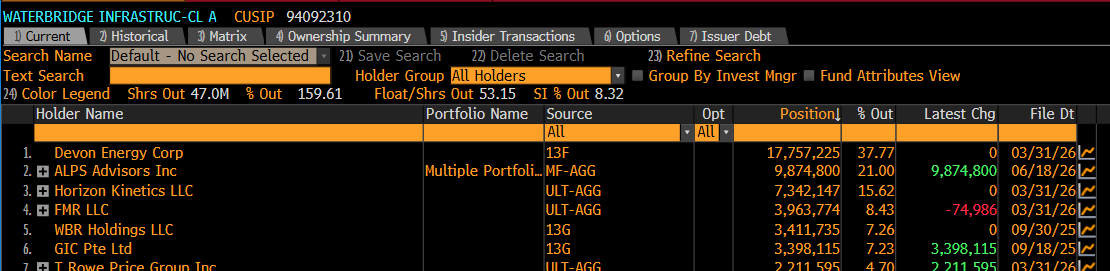

@310Value I was thinking that it got shorted, but it doesn't look like it. Still it's like 16% shorted which is high. Trying to figure out why those people have a position like this when it's likely that these funds won't be sellers anytime soon.

$AMLP bought 21% of class A. This is kind of insane. We have 76M shares of class B that don't trade and more than 80% of class A that are in the hands of long term investors (Devon ~38%, ALPS ~21%, Horizon kinetics ~16% and FivePoints ~7%). And I think that GIC pte is a sovereign wealth fund that owns another 7%. Fidelity another 8%. Not sure what to think...

@charliebilello I have no opinion on $MU but a price to sale on a business that earning growth predicated by margin expansion makes no sense. P/E is pretty much in line with historical.

Sell side analysts consistently underestimate $PGR earnings power, even today as the stock is in a drawdown. The 2021-2025 timeframe was probably the best performing period for progressive as they were completely alone and taking market share like crazy as everybody else struggled. Even today, in a soft market $PGR is in a league of its own.

@BrownMarubozu Obviously there is no appetite for defensive stocks right now (look at the canadian banks valuation) but you’re also fighting a soft market in commercial insurance which I think managers are taking into account

@310Value Makes sense, but seems a stupid way to buy for an active fund and not sure that $WBI is in any passive ETF. But that is the most likely explanation I guess

@ohcapideas@ReneSellmann Not sure that DQ is that important for Berkshire. I think buffet was stuborn with both Geico (not using telematic) and BNSF (not implementing PSR). Hopefully with Abel being an “operator”, he can change that