Global company specializing in quantitative research. We are creating a new, technologically advanced, and equitable world of the future.

[email protected]

Quantillion Atlas — daily digest

🟡 Holding pattern: markets await Nvidia catalyst while geopolitical crosscurrents persist

Today's macro pulse: Equities ground higher into the Nvidia earnings print as bond yields paused near cycle highs and Iran diplomacy hints tempered energy-led inflation fears.

• Stocks grind up pre-Nvidia, bonds stabilize. US equities advanced with Nvidia leading ahead of tonight's results — the single most-watched earnings event this quarter. Bond yields paused after a multi-day sell-off but remain near recent highs, keeping risk sentiment on a short leash.

source: investing

• Iran talks in "final stages" — oil and gas ease. Trump signaled US-Iran negotiations are approaching conclusion, prompting crude to slip as tankers resumed transit through the Strait of Hormuz. European natural gas prices also retreated on reduced supply-disruption premium. The UAE's Hormuz bypass pipeline is 50% complete, adding a structural hedge.

source: investing

• ECB June rate hike all but locked in. Sources indicate the ECB has largely settled on a June hike, though July remains an open question. The hawkish tilt reflects persistent core inflation concerns in the eurozone and adds to the global tightening narrative pressuring duration assets.

source: investing

• Dollar near six-week high; gold faces triple headwind. The dollar firmed on rate-hike expectations and residual Iran uncertainty, hovering at a six-week peak. Oil, yields, and the greenback are forming a concurrent headwind for gold, which managed only a marginal uptick despite safe-haven demand.

source: investing

• Indian rupee hits record low; RBI mobilizes $5B swap. USD/INR pushed toward 97 as the oil price shock cascaded through India's current account. The RBI responded with a planned $5 billion FX swap auction to inject rupee liquidity — a signal of acute EM stress from the energy-rate nexus.

source: investing

• Semiconductor names surge ahead of Nvidia print. Lattice Semiconductor and KLA both posted sharp gains, riding pre-earnings momentum across the chip complex. AI-adjacent capex narratives remain the primary bid driver, with convertible bond issuance from AI-linked firms also surging.

source: investing

Summary

Markets are in a classic pre-catalyst consolidation: equities lean constructive on Nvidia optimism and Iran de-escalation hopes, but elevated bond yields and a strong dollar keep the risk surface mixed 🟡. Tonight's Nvidia print will likely determine short-term directional conviction.

Quantillion Atlas — Researched Return (since inception, Jul 01, 2010 to May 19, 2026, 15.9 years)

Return: +2842.94%

Return YTD: +1.32%

1Y Return: +18.67%

3Y Return: +72.55%

CAGR (since 2010): 23.73%

Sharpe: +2.44

Volatility: 6.09%

Max Drawdown: 7.79%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Nvidia #IranTalks #BondYields

Quantillion Research — June additions

Five names from this month's research universe, ranked by our internal Research Score (1–5).

🔘DG — Discount Retail — 4.70/5

Dollar General delivered fiscal-Q4 EPS of $1.93 (~20% above forecast) and 4.3% same-store-sales growth on both traffic and basket size, while expanding full-year gross margin 107 basis points, helped by an 80-bp reduction in shrink.

With ~20,500 stores and roughly 75% of the U.S. population within five miles of one, it trades at a forward P/E near 14 and a PEG of ~0.44. The score reflects a mixed revision trend — 3 upward EPS revisions against 14 down over 90 days.

🔘NBIX — Biotech / Neuroscience — 4.88/5

In Q3 2025, Neurocrine delivered net product sales of $790M, up 28% year-over-year, led by INGREZZA at $687M with record new-patient starts, while CRENESSITY added $98M in just its third quarter on market.

The balance sheet carries $2.1B in cash and no debt, funding sales-force expansion across both franchises — INGREZZA still reaches only ~10% of an ~800,000-patient tardive-dyskinesia population. Ten upward EPS revisions came against five down; the score is held by a richer PEG near 2.9.

🔘QCOM — Semiconductors / Wireless — 4.46/5

Qualcomm beat fiscal Q2 2026 (EPS $2.65 vs $2.55) and shares gained ~15% over the following week. Diversification is showing: automotive revenue hit $1.3B (+38% YoY) toward a $6B annual run-rate, IoT reached $1.7B, and the company secured an AI-chip deal with ByteDance plus a custom-silicon engagement with a hyperscaler. It yields ~1.5% with a 23-year dividend streak. The score reflects a real caution — 23 downward EPS revisions over 90 days and memory-supply constraints.

🔘IBP — Building Products — 4.74/5

Installed Building Products has diversified from 78% to 60% insulation revenue and cut new single-family exposure from 75% to 57% since 2015.

Its Q3 2025 quarter beat with adjusted EPS of $3.18 vs $2.73, and the balance sheet is conservative — net debt to adjusted EBITDA of 1.09x against a 2x target — with ~$213M returned to shareholders over the first nine months of 2025 and 10 upward EPS revisions against none down. The score reflects a full multiple, with a forward P/E near 25.

🔘TCOM — Online Travel — 4.82/5

Trip grew 2025 net revenue 17% to RMB 62.4B on ~RMB 1.1T of gross bookings, with its international OTA platform up 60% and inbound travel to China more than doubling to ~20M travelers.

It holds a fortress balance sheet — RMB 105.8B in cash — and trades at a P/E near 6 with a PEG of ~0.07. The score carries a clear offset: an antitrust review by China's market regulator opened in early 2026, alongside a soft twelve-month share performance.

—

For research purposes only. This is not an investment idea, not investment advice, not a recommendation, and not an offer or solicitation. Quantillion Research Scores (1–5) are an internal qualitative synthesis of data — not a rating of any security or regulated entity. Past performance is not an indicator of future performance.

Quantillion Atlas — daily digest

🟡 Cautious relief: geopolitical premium unwinds, but rate anxiety persists

Today's macro pulse: Iran's reported cessation of attacks on Israel triggered a broad risk-on rotation — oil pared gains, the dollar softened, and US equities opened higher — yet Fed tightening fears and an Asian tech rout remind that the reprieve may be shallow.

• Middle East de-escalation lifts risk assets. Oil prices gave back earlier spikes after Iran signaled an end to its attacks on Israel, removing the acute geopolitical bid from crude. The dollar eased from a two-month high as safe-haven demand faded, while gold found a bid as oil-driven inflation fears receded.

source: https://t.co/DshYaxZydG

• Chip stocks rebound; Marvell added to S&P 500. US semiconductor shares recovered sharply after Friday's sell-off, with Marvell jumping on its S&P 500 inclusion and Cerebras climbing as multiple brokerages endorsed its AI chip strategy. Separately, Google reportedly ordered 3 million AI chips from Intel for 2028 production — a potential lifeline for Intel's foundry ambitions.

source: https://t.co/DshYaxZydG

• KOSPI craters 8%+ on Fed fears and tech contagion. South Korea's benchmark index suffered its worst session in years as hawkish Fed repricing combined with the global tech rout to trigger forced selling across Asian markets. The move underscores how sensitive leveraged Asian tech positioning remains to US rate expectations.

source: https://t.co/DshYaxZydG

• Gold and silver in technical breakdown. Gold's hourly RSI hit 29.9 — deep oversold territory — after falling near $4,367 amid a sharp downtrend driven by rising real yields and dollar strength. Silver confirmed a bearish engulfing pattern, dropping 15% over the past month. Sell-side downgrades on gold miners reinforce the bearish momentum.

source: https://t.co/DshYaxZydG

• Inflation signal with 87% historical hit rate flashes again. A historically reliable inflation indicator has re-triggered, complicating the narrative that the Fed can remain patient. Combined with strong US jobs data reinforcing tightening bets, the macro backdrop favors a "good news is bad news" regime for equities.

source: seeking alpha

• UK commits £1.1B to sovereign AI compute. Britain unveiled a national AI infrastructure plan aimed at reducing dependence on foreign cloud providers and positioning the UK as a European AI hub. The investment signals continued government-level conviction in AI capex despite broader market rotation away from the theme.

source: https://t.co/DshYaxZydG

Summary

Markets are bifurcated: the Middle East ceasefire and chip rebound provide near-term relief, but the KOSPI crash, metals breakdown, and re-emerging inflation signals suggest the rally lacks conviction. The mixed 🟡 sentiment reflects a market caught between fading tail risks and tightening financial conditions.

Quantillion Atlas — Researched Return (Jan 01–Jun 05, 2026, YTD)

Return: +0.98%

Sharpe: 0.23

Volatility: 8.27%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Semiconductors

Quantillion Research — June additions

Five names from this month's research universe, ranked by our internal Research Score (1–5).

🔘KLIC — Semiconductor Equipment — 4.64/5

Kulicke & Soffa's fiscal-2026 momentum is accelerating: fiscal Q2 revenue of $242.6M rose 21.5% sequentially and beat by ~27%, with non-GAAP EPS of $0.79 ahead by ~18%.

Management guides ~28% further sequential growth to $310M in Q3. The strategic driver is thermal-compression bonding for advanced packaging, projected to grow at least 70% sequentially and clear $100M this fiscal year.

Shares are up ~213% over twelve months; the score sits mid-band as the trailing multiple already reflects much of the recovery.

🔘ONTO — Semiconductor Equipment — 4.60/5

Onto Innovation rides AI-driven demand for process-control metrology and inspection. Q1 2026 revenue of $292M and EPS of $1.42 both beat, and management guided Q2 to $320–330M — ~28% year-over-year growth at midpoint — with full-year revenue seen up more than 30%.

Its Dragonfly G5 platform qualified at a leading 2.5D-logic customer with 10+ customers in the pipeline, positioning advanced-packaging revenue for 50%+ growth in 2026. Shares have returned more than 130% over the year, which holds the score mid-band on valuation.

🔘EXEL — Biopharma / Oncology — 4.57/5

Exelixis paired Q1 2026 revenue of $611M (+10% YoY) with a non-GAAP EPS beat ($0.87 vs $0.77). Its flagship CABOMETYX is the #1 prescribed TKI in renal-cell carcinoma, and the global cabozantinib franchise grew 12.5% to $764M.

The next leg is zanzalintinib, with seven pivotal trials underway or planned and an FDA decision pending in metastatic colorectal cancer. A PEG of ~0.40 and a ~7.3% free-cash-flow yield underpin a name whose shares recently reached a 52-week high.

🔘TXN — Semiconductors / Analog — 4.54/5

Texas Instruments posted its eighth consecutive quarter of sequential growth, with Q1 2026 revenue of $4.83B and EPS of $1.68 beating by ~7% and ~24%. The Analog segment rose 22% year-over-year and the data-center market 90%, helped by 300mm manufacturing scale and an 80,000-product catalogue.

Eight upward EPS revisions came against none down, and shares gained ~77% over twelve months. The score is tempered by a rich multiple — a trailing P/E in the mid-50s.

🔘NEXA — Metals & Mining — 4.52/5

Nexa Resources is an integrated zinc miner-and-smelter with by-product exposure to copper, silver, lead and gold. In Q4 2025 net revenue rose 22% and adjusted EBITDA climbed 53% year-over-year on firmer metal prices and better operations.

The valuation is the standout — a forward P/E near 4.3 and EV/EBITDA near 2.6, roughly a 70% discount to its sector — against a 2026 backdrop of tight zinc inventories and resilient demand, with the Aripuanã and Cerro Pasco projects adding optionality.

—

For research purposes only. This is not an investment idea, not investment advice, not a recommendation, and not an offer or solicitation. Quantillion Research Scores (1–5) are an internal qualitative synthesis of data — not a rating of any security or regulated entity. Past performance is not an indicator of future performance.

Quantillion Atlas — daily digest

🟡 Tech deflates on AI reality check; geopolitical risk premium holds firm

Today's macro pulse: Broadcom's earnings miss crystallized growing skepticism around AI monetization timelines, dragging semiconductor names and the broader Nasdaq lower, while persistent US-Iran tensions kept the dollar bid and pushed the yen to intervention territory.

• Broadcom slides 14% as AI guidance disappoints. Revenue missed consensus despite soaring AI chip sales, suggesting the market had already priced in a more aggressive ramp. The selloff cascaded through the semiconductor complex, pulling the Nasdaq and S&P 500 lower at the open — a clear signal that AI-adjacent names face increasingly asymmetric expectations risk.

source: https://t.co/DshYaxZydG

• Yen breaches 160 as Gulf tensions supercharge the dollar. The greenback hovered near a two-month high, driven by escalating US-Iran rhetoric and widening rate differentials. USD/JPY pushed through 160 — a level that historically triggers verbal and actual intervention from the BoJ. FX vol is repricing accordingly.

source: https://t.co/DshYaxZydG

• US commits to tariff caps in EU and Japan trade deals. Trade Representative Greer confirmed the US will honor ceiling rates in bilateral negotiations, offering a modestly constructive signal for global trade flows. The statement de-risks near-term escalation scenarios, though implementation timelines remain vague.

source: https://t.co/DshYaxZydG

• Options market positions for Treasury selloff into July. Rate traders are adding exposure to higher yields, betting the current macro mix — sticky inflation, fiscal expansion, and geopolitical premium — will push long-end rates higher through the summer. Duration remains a contested trade.

source: https://t.co/DshYaxZydG

• Israel-Lebanon ceasefire renewal lifts European equities, caps natgas. The fragile truce agreement provided a marginal risk-on impulse for European indices and eased natural gas pricing, though gold continued to extend gains on broader safe-haven demand ahead of US payrolls data.

source: https://t.co/DshYaxZydG

Summary

Markets lean risk-off as the AI narrative encounters valuation gravity and geopolitical crosscurrents persist across the Gulf and rate markets. The mixed 🟡 aggregate sentiment reflects a session where isolated positives on trade diplomacy were insufficient to offset the tech-led drag and dollar strength heading into payrolls.

Quantillion Atlas — Researched Return (Jan 01–Jun 03, 2026, YTD)

Return: +1.53%

Sharpe: 0.35

Volatility: 8.16%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Broadcom #Semiconductors #FXVolatility

Quantillion Research — June additions

Five names from this month's research universe, ranked by our internal Research Score (1–5).

🔘DINO — Refining / Energy — 4.89/5

HF Sinclair turned in a Q1 2026 few saw coming: EPS of $0.69 against a $0.07 forecast — an ~886% beat — on revenue of $7.12B.

Adjusted EBITDA jumped 112% year-over-year to $426M, with adjusted net income of $127M versus a $50M loss a year earlier, as the refining segment swung to positive EBITDA and renewables flipped from −$17M to +$133M.

The valuation stays modest — a PEG near 0.01 and a ~10.7% free-cash-flow yield — and the company has returned $4.9B to shareholders since the 2022 Sinclair acquisition.

🔘CHRD — Oil & Gas E&P — 4.84/5

Chord Energy, the largest acreage holder in the Williston Basin, beat Q1 2026 EPS by ~38% and revenue by ~43% ($1.67B), generated $324M of adjusted free cash flow and returned $145M through dividends and buybacks, with the share count down 12% since end-2023.

Management raised 2026 oil-output guidance to ~161,000 bpd and projects ~$1.4B of full-year free cash flow. It trades at a forward P/E of ~6.6 and EV/EBITDA of ~4.0 — cheap for the cash generation — with shares up ~55% over twelve months.

🔘EXPE — Online Travel — 4.79/5

Expedia delivered EPS of $1.96 in Q1 2026, ~41% above forecast, on revenue up 15% to $3.43B and gross bookings of $35.5B. Adjusted EBITDA margin reached 15.8% — the highest first-quarter margin in 15 years — while B2B bookings grew 22% and consumer bookings rose 10%, the fastest pace in twelve quarters.

The board authorized a new $5B repurchase. With a PEG of ~0.55, a ~15% free-cash-flow yield and 15 upward EPS revisions against 5 down, growth and valuation are pulling the same way.

🔘CRDO — Semiconductors / Connectivity — 4.74/5

Credo has become a critical supplier into AI data-center buildouts, where its active electrical cables are valued for reliability — effectively zero failures across billions of operating hours.

Revenue grew ~64% year-over-year in the quarter cited in our source data, with full-year growth then guided above 100%, as the customer and product base broadens beyond its original niche.

It ranks #2 among semiconductor names in our data, with the score held below the top of the band on an elevated valuation after a very large run.

🔘CYD — Industrials / Engines — 4.69/5

China Yuchai posted FY2025 revenue up 38.9% to RMB 24.7B (~$3.5B) and net profit up 66.3% to RMB 537M, as total engine sales grew 29.4% to 461,309 units on an 80%+ jump in heavy-duty truck engines.

It holds over 45% of China's bus-engine market and runs a 600,000-unit annual production base.

The stock trades at a PEG of ~0.28 despite a ~175% twelve-month gain — explosive growth at a low multiple, tempered by the cyclicality of its end markets.

—

For research purposes only. This is not an investment idea, not investment advice, not a recommendation, and not an offer or solicitation. Quantillion Research Scores (1–5) are an internal qualitative synthesis of data — not a rating of any security or regulated entity. Past performance is not an indicator of future performance.

#US #research

Quantillion Atlas — daily digest

🟡 Record highs meet hawkish resistance — markets pause to recalibrate

Today's macro pulse: Wall Street pulled back from fresh all-time highs as Fed hawkishness on inflation collided with continued AI-driven momentum in semiconductors and a broad risk-off rotation in crypto.

• Marvell surges 22% on Nvidia CEO's trillion-dollar endorsement. Jensen Huang publicly labeled Marvell the "next trillion-dollar company," triggering a massive re-rating. The move reinforces the broadening of AI infrastructure spending beyond Nvidia into custom silicon and networking plays.

source: investing

• Fed's Hammack flags potential rate hikes if inflation persists. Cleveland Fed President Hammack explicitly warned that tighter policy remains on the table should disinflation stall, pushing back against market pricing of near-term cuts. The hawkish tone adds a ceiling to risk appetite at current valuations.

source: investing

• Bitcoin breaks below $70,000 as sell-off deepens. The largest cryptocurrency extended its drawdown, breaching the $70K psychological level. Deleveraging pressure and reduced institutional inflows suggest the risk-off mood is spreading beyond equities into digital assets.

source: seeking alpha

• Oil drops on progress in US-Iran negotiations. Crude prices declined as Iran reviewed a proposed US agreement, raising the probability of eventual sanctions relief and additional supply. Gold moved inversely, gaining ~1% as lower oil eased inflation expectations and bolstered the rate-cut narrative.

source: investing

• Victoria's Secret surges on turnaround confirmation. The retailer lifted full-year guidance after a strong Q1, validating the multi-quarter brand repositioning. The stock's sharp move higher underscores market willingness to reward execution in consumer discretionary despite macro headwinds.

source: investing

Summary

A mixed session: AI semiconductor momentum and select earnings beats provided upside, but hawkish Fed rhetoric and crypto weakness capped broad risk appetite. The 🟡 mixed read reflects a market in consolidation mode near all-time highs, awaiting clearer signals on inflation trajectory and monetary policy direction.

Quantillion Atlas — Researched Return (Jan 01–Jun 01, 2026, YTD)

Return: +2.09%

Sharpe: 0.46

Volatility: 8.18%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Semiconductors #FedPolicy #Bitcoin

Quantillion Research — June openers

Five names from this month's research universe, ranked by our internal Research Score (1–5).

🔘SNEX — Capital Markets — 4.98/5

Fiscal Q2 2026 net income rose 143% year-over-year to a record $174M, and EPS beat estimates by more than 50%. Return on equity reached 26.5%, well above the firm's own 15% target, while the stock trades at a PEG of only ~0.46 — growth and valuation pulling the same way.

The franchise is also strengthening structurally: S&P raised StoneX's credit rating in April 2026, and the R.J. O'Brien acquisition is already contributing ~$32M of annual synergies against a $50M target. Shares are up ~101% over twelve months, and the board approved a 3-for-2 split.

🔘INSW — Tankers / Energy — 4.92/5

A rare combination of cheap, profitable and improving. International Seaways trades at a P/E of ~7 with a PEG near 0.1, while operating margin sits around 46% and return on assets near 20% — efficiency that is unusual for the sector. Q1 earnings beat by ~45%, liquidity stands at $918M, and net debt is below 7% of fleet value, leaving the balance sheet conservatively positioned.

The capital-return profile is substantial: a dividend yield of ~11% and more than $1B returned to shareholders since 2020. Current Q2 bookings of ~$100k/day sit far above a ~$15k/day cash breakeven.

🔘ARM — Semiconductors — 4.75/5

Revenue grew ~23% year-over-year, with licensing revenue up 29% in the latest quarter and gross margin around 97% — a royalty model that scales with the whole industry's chip volume.

Contracted demand for Arm's AI-focused chips already exceeds $2B across the next two fiscal years, and management's stated ambition is ~$25B of annual revenue by 2031 versus ~$5B today, helped by a rising data-center share and partnerships spanning Meta, Nvidia and major cloud providers.

Shares are up more than 220% year-to-date, near a 52-week high. The score sits below the top of the band on valuation: the multiple already prices in much of that trajectory.

🔘FSLR — Solar / Clean-Energy Tech — 4.68/5

Revenue rose ~27% year-over-year, net income hit a record $347M (+65% YoY), and module volumes shipped climbed 31%. Despite that momentum the stock carries a PEG of only ~0.63 — a low price for the growth rate.

Forward visibility is unusually clear: an order backlog of 47.9 GW worth roughly $14.4B, new US manufacturing capacity coming online, and trade measures that weigh on overseas competitors. Shares are up ~94% over twelve months, recently touching an 18-year high.

🔘OXY — Oil & Gas — 4.6/5

Growth is broad-based: Q1 2026 EPS came in at $1.06 against $0.59 expected — nearly double — free cash flow rose ~52% year-over-year to $1.7B, and production ran above guidance.

The deleveraging story is the standout: debt was cut from $20.8B to $13.3B in just six months, lowering annual interest expense by hundreds of millions and freeing real value for shareholders. Shares are up ~42% over the past twelve months.

—

For research purposes only. This is not an investment idea, not investment advice, not a recommendation, and not an offer or solicitation. Quantillion Research Scores (1–5) are an internal qualitative synthesis of data — not a rating of any security or regulated entity. Past performance is not an indicator of future performance.

#research #stocks #US

Quantillion Atlas — daily digest

🟡 Mixed signals: ceasefire optimism collides with sticky inflation and recession risk

Today's macro pulse: Markets are torn between US-Iran ceasefire extension hopes compressing oil risk premia and a string of inflation prints that keep central banks boxed in.

• Oil drops 2% on US-Iran ceasefire extension reports. Crude fell sharply as reports surfaced that Washington and Tehran reached a ceasefire extension deal, pulling the geopolitical risk premium out of energy markets. The dollar softened in response, while equities edged higher at the open on reduced tail risk.

source: https://t.co/DshYay063e

• Chicago PMI surges, signaling manufacturing expansion. The Chicago PMI printed well above expectations, marking robust expansion in the manufacturing sector — a rare bright spot amid otherwise cooling activity data. The reading reinforces the view that US industrial production is holding up despite elevated rates.

source: https://t.co/DshYay063e

• Canada enters technical recession. Q1 GDP contracted on an annualized basis, marking two consecutive quarters of decline. The unexpected contraction raises pressure on the Bank of Canada to ease, even as the Fed remains on hold.

source: https://t.co/DshYay063e

• Euro zone inflation stays above ECB target for third month. May CPI remained stubbornly above 2%, with German core prices accelerating even as headline eased to 2.7%. The data complicates the ECB's path to further cuts and keeps European rates vol elevated.

source: https://t.co/DshYay063e

• US equity funds draw strong weekly inflows on AI/tech rally. Fund flow data showed sustained inflows into US equities, driven by the ongoing AI theme. Dell surged on Q1 results, and Nvidia's $1T AI infrastructure vision kept semiconductor sentiment bid.

source: https://t.co/DshYay063e

• Fed's Bowman flags energy shock as inflation risk. Governor Bowman warned that an extended energy shock from the Iran conflict could shift the policy outlook toward tighter conditions, pushing back against market expectations for near-term easing.

source: https://t.co/DshYay063e

Summary

The session reflects a market caught between geopolitical de-escalation tailwinds and persistent inflation headwinds — the 🟡 mixed read is warranted. Risk assets are marginally bid on ceasefire hopes and AI momentum, but sticky price data and hawkish Fed rhetoric cap the upside.

Quantillion Atlas — Researched Return (Jan 01–May 28, 2026, YTD)

Return: +1.59%

Sharpe: 0.37

Volatility: 8.26%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Ceasefire #Inflation #TechRally

Quantillion Atlas — daily digest

🟡 Cross-asset repricing on Gulf escalation; PCE keeps the Fed pinned

Today's macro pulse: Renewed US-Iran military exchanges dominated flows, lifting crude and the dollar while pressuring gold and capping equity upside alongside a firmer-than-desired April PCE print.

• US-Iran hostilities escalate, oil jumps. Tit-for-tat airstrikes — including IRGC targeting a US airbase after strikes near Bandar Abbas — pushed crude nearly 2% higher. The EU flagged tightening jet fuel markets if Strait of Hormuz disruptions persist, adding a structural supply-risk premium. Bernstein's long-term anchor remains ~$75/bbl, but near-term skew is to the upside.

source: https://t.co/DshYaxZydG

• Gold slides despite haven bid. Counterintuitively, gold fell as the dollar's geopolitical rally and renewed rate-hike pricing outweighed safe-haven demand. The metal remains caught between competing forces — inflation hedge vs. higher real rates.

source: https://t.co/DshYaxZydG

• April PCE firmer, GDP slips. Core PCE came in above comfort levels while GDP growth decelerated — a stagflationary signal that complicates the Fed's easing path. Williams noted productivity shifts are hard to identify in real time, underscoring data-dependence without forward guidance.

source: https://t.co/DshYaxZydG

• UBS: markets may overprice Fed hawkishness. UBS argued current rate expectations embed too much tightening risk, suggesting the terminal rate is closer to consensus than futures imply. If correct, duration-sensitive assets have room to recover — a view worth monitoring against incoming labor data.

source: https://t.co/DshYaxZydG

• Dollar firms near April highs. The greenback consolidated at its strongest since April on safe-haven flows and sticky inflation. JPMorgan AM maintains a structural long-term bearish USD view on fiscal dynamics, but near-term momentum favors the dollar.

source: https://t.co/DshYaxZydG

• Best Buy guides above consensus on resilient gadget demand. Upbeat quarterly sales guidance cited steady consumer electronics demand and marketplace growth — a notable counterpoint to tariff-driven margin anxiety across retail. Shares rallied pre-market.

source: https://t.co/DshYaxZydG

Summary

Markets ended in a holding pattern — geopolitical risk premium in energy offset by sticky inflation that narrows Fed optionality. The aggregate sentiment score (+0.03) captures a tape pulled in opposing directions: commodity supply fear vs. monetary policy constraint. Equities drifted below recent highs with no catalyst to break the impasse.

Quantillion Atlas — Researched Return (Jan 01–May 26, 2026, YTD)

Return: +1.67%

Sharpe: 0.39

Volatility: 8.32%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #USIran #PCEInflation #OilPrices

🇺🇸 Equities

"$600 billion in US equity issuance in 2026" grabs attention and feeds the doom narrative. But relative to the total value of US equities, it is not that large. Big number, yes, but scale matters

👉 https://t.co/blMxcoFA78

h/t @GoldmanSachs#IPO#stocks $spx #spx

Quantillion Atlas — daily digest

🟡 Markets tread water as Hormuz diplomacy offsets rate anxiety

Today's macro pulse: Potential progress on a US-Iran deal to reopen the Strait of Hormuz drove crude sharply lower, while rising US mortgage rates and muted equity indices kept overall sentiment flat.

• Oil slides on Hormuz reopening signals. Iranian state TV reported a draft deal with the US to restore pre-war shipping traffic through the Strait of Hormuz within a month, sending crude prices lower. Separately, the US shipped SPR oil to California for the first time during the conflict — a measure of supply stress even as diplomacy advances.

source: https://t.co/DshYay063e

• US banking sector flashes strength. FDIC data showed a first-quarter profit uptick across US banks. JPMorgan's CEO flagged investment banking fees rising 10%+ in Q2 and up to $20B in M&A pipeline, while BofA's CEO projected trading revenue climbing 15% in the current quarter.

source: https://t.co/DshYay063e

• Meta rises on premium subscription rollout. Shares gained after the company announced a paid subscription tier, adding a direct monetization layer beyond advertising — a structural revenue diversifier if adoption scales.

source: https://t.co/DshYay063e

• Applied Digital surges on $3.6B AI factory plan. The "Delta Forge 1" AI data center commitment signals continued capital deployment into GPU infrastructure, reinforcing that AI capex shows no sign of decelerating despite broader macro caution.

source: seeking alpha

• US mortgage rates hit 9-month high. Rising rates are compressing housing affordability again, a headwind for the consumer-driven recovery thesis. The move aligns with sticky inflation expectations and a repricing of Fed rate-hike probabilities.

source: https://t.co/DshYay063e

• Banxico slashes 2026 growth forecast to 1.1%. The Bank of Mexico cut its GDP outlook from 1.6%, reflecting persistent weakness in the domestic economy and tighter financial conditions across EM. The peso remains under pressure.

source: https://t.co/DshYay063e

Summary

A mixed session driven by two competing narratives: geopolitical de-escalation in the Persian Gulf pulling energy lower, and persistent rate and inflation concerns capping equity upside. The 🟡 neutral aggregate reflects a market awaiting decisive catalysts before committing directionally.

Quantillion Atlas — Researched Return (Jan 01–May 26, 2026, YTD)

Return: +1.67%

Sharpe: 0.39

Volatility: 8.32%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Hormuz #AIinfra #Rates

Quantillion Atlas — daily digest

🟡 Mixed signals: AI momentum lifts equities while fresh Middle East strikes keep commodities volatile

Today's macro pulse: Markets are caught between two forces — persistent AI-driven equity optimism and renewed geopolitical risk from US military strikes on Iran, sending oil higher and gold lower in a classic risk-repricing session.

• Oil jumps 3% on fresh US-Iran strikes. Brent crude rallied as new US military action against Iran overshadowed earlier hopes for a Strait of Hormuz reopening deal. A tanker explosion off the Oman coast added to supply-route anxiety, reinforcing the geopolitical risk premium in energy markets.

source: investing

• Wall Street opens higher as AI trade dominates. US equities gained at the open with semiconductor and AI names leading — Broadcom, SanDisk, and Micron all surging. The market's willingness to look through Middle East escalation underscores the durability of the current tech bid.

source: investing

• Gold slips 1% as real-rate dynamics reassert. Spot gold declined as fresh strikes dampened near-term peace hopes, paradoxically weighing on the metal as inflation fears shifted rate-cut expectations. Separately, Uzbekistan resumed gold exports after a six-month halt, adding a marginal supply-side headwind.

source: investing

• ECB flags energy shock as key policy variable. Board member Sleijpen signaled the central bank will do "whatever needed" to return inflation to target, with the persistence of the energy shock identified as the decisive factor for the next rate decision. The hawkish lean adds to EUR support near term.

source: investing

• BP ousts chair Manifold over governance failures. The board removed its chairman following unspecified governance issues, adding to a turbulent period for the energy major amid ongoing strategic pivots. Corporate governance risk is being repriced across European oil & gas.

source: investing

Summary

A bifurcated session: equities lean constructive on durable AI and semiconductor momentum, while commodities reprice geopolitical risk from the US-Iran theatre. The 🟡 mixed aggregate sentiment reflects this push-pull — neither bulls nor bears hold full conviction heading into the week.

Quantillion Atlas — Researched Return (Jan 01–May 22, 2026, YTD)

Return: +1.29%

Sharpe: 0.31

Volatility: 8.42%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Oil #AI #ECB

Quantillion Atlas — daily digest

🟢 Risk-on tilt as Hormuz reopening bets reshape cross-asset flows

Today's macro pulse: Prospect of a US-Iran framework deal dominated price action across crude, FX, and equities, triggering a broad repricing of geopolitical risk premium.

• Brent drops below $100 on Iran deal optimism. Oil slid to a two-week low as Secretary Rubio flagged a "pretty solid framework" for reopening the Strait of Hormuz. Brent crude broke below the psychologically important $100/bbl level, with European natural gas prices following suit. Supply normalization expectations are pulling forward, though skeptics note structural bottlenecks may limit the magnitude of any sustained move lower.

source: https://t.co/DshYaxZydG

• Global equities rally on geopolitical de-escalation. European markets opened higher, India's Nifty 50 gained 1.32%, and TSX futures jumped as risk appetite broadened. The relief rally was most pronounced in energy-importing economies where the oil risk premium unwind translates directly into improved macro outlooks.

source: https://t.co/DshYaxZydG

• Dollar slumps as safe-haven demand fades. The greenback weakened across major pairs as improving geopolitical sentiment eroded defensive positioning. Asian currencies firmed broadly, with the Indian rupee additionally supported by the RBI Governor's explicit warning on further intervention.

source: https://t.co/DshYaxZydG

• Gold climbs despite risk-on backdrop. Gold prices rose, decoupling from the typical risk-on playbook. The move was largely dollar-driven — the weaker greenback mechanically supports USD-denominated commodities — rather than reflecting renewed safe-haven demand.

source: https://t.co/DshYaxZydG

• Bank of Israel resumes rate cuts. The BoI cut rates with inflation remaining stable despite the regional conflict backdrop, signaling confidence in anchored expectations. The decision provides a dovish data point for EM central bank watchers tracking the global easing cycle.

source: https://t.co/DshYaxZydG

• Hedge fund tech allocations hover near record. Goldman Sachs data shows hedge fund technology positioning remains near all-time highs, underscoring persistent conviction in the AI capex cycle despite elevated valuations. Crowding risk warrants monitoring.

source: https://t.co/DshYaxZydG

Summary

Markets are pricing in a material reduction in Middle East risk premium, driving a correlated move: equities up, oil and gas down, dollar weaker, EM currencies firmer. The 🟢 risk-on lean is clear, though execution risk on any Iran deal remains high and the asymmetry favors caution on chasing the initial move.

Quantillion Atlas — Researched Return (Jan 01–May 22, 2026, YTD)

Return: +1.29%

Sharpe: 0.31

Volatility: 8.42%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #IranDeal #CrudeOil #RiskOn

Quantillion Atlas — daily digest

🟡 Thin conviction: equities grind higher as bond stress and geopolitical fog persist

Today's macro pulse: Markets navigated a tug-of-war between resilient equity momentum and rising global bond yields, with US-Iran peace talks injecting uncertainty across rates, commodities, and FX.

• US-Iran talks dominate cross-asset pricing. Treasury yields declined as Iran reviewed a peace proposal, while oil prices rose on skepticism that a breakthrough is imminent — UAE officials put deal odds at 50-50. The dollar hovered near a six-week high on haven demand, and Qatar dispatched a negotiating team to Tehran to help finalize terms.

source: https://t.co/DshYaxZydG

• Flash US PMI flags stagflationary undertones. May's preliminary PMI data showed subdued growth and job cuts alongside a surge in input prices — a combination that complicates the Fed's path and reinforces the case for an extended hold on rates.

source: seeking alpha

• Global equity fund flows reverse after eight-week streak. Investors halted buying as rising sovereign bond yields repriced the risk-free rate globally, compressing equity risk premiums. The rotation into duration-sensitive assets appears to be stalling.

source: https://t.co/DshYaxZydG

• Higher yields pressure AI momentum names. Morgan Stanley noted that while earnings fundamentals still support selective exposure to AI plays, the rate environment is compressing multiples on the highest-duration growth stocks. DA Davidson separately reiterated Buy ratings on Datadog and Take-Two, citing AI positioning and GTA VI timeline confirmation.

source: https://t.co/DshYaxZydG

• Chinese ADRs slide on regulatory crackdown. Futu Holdings plunged after receiving an investigation and penalty-related letter from China's securities regulator, dragging the broader Chinese ADR complex lower and reigniting concerns about Beijing's unpredictable posture toward cross-border brokerage operations.

source: seeking alpha

• European banks provision €1.5B+ for Middle East exposure. Lenders are building reserves against potential losses tied to regional instability, adding another drag on European financial sector earnings at a time when ECB policy uncertainty and growth divergence already weigh on the outlook.

source: seeking alpha

Summary

The session's mixed tone 🟡 (mean sentiment +0.08) reflects a market caught between supportive equity earnings and deteriorating macro signals — stagflationary PMI data, rising yields, and geopolitical ambiguity around Iran. Risk appetite persists but conviction is thin; the bond market remains the arbiter to watch.

Quantillion Atlas — Researched Return (Jan 01–May 21, 2026, YTD)

Return: +1.43%

Sharpe: 0.34

Volatility: 8.45%

Max Drawdown: 5.89%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #IranTalks #BondYields #PMI

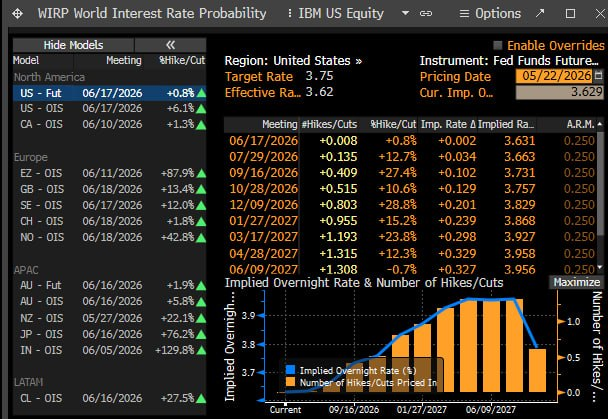

Everyone is focused on the usual soft-landing story, but the rates market is quietly starting to tell a different story.

Oil is still high, inflation pressure is not really gone, and WIRP is already showing that the market is no longer pricing only cuts. There is now a real probability of Fed hikes coming back into the curve for 2026–2027.

That matters.

Because if energy keeps feeding into inflation, the Fed may not have the clean path to cut rates that many investors are still hoping for.

This setup feels much closer to 2022 than people want to admit: oil pressure, sticky inflation, rates repricing, duration risk, sector rotation, and more volatility.

Most people will see this too late.

But these are exactly the moments when the best opportunities appear - when the market is still pretending nothing has changed, while the data is already moving.

Source: Bloomberg

#oil #FED #Brent #futures #US

Quantillion Atlas — daily digest

🟡 Mixed signals: geopolitical risk offsets resilient US data

Today's macro pulse: Iran's Supreme Leader insisting enriched uranium remain domestically has upended near-term peace deal expectations, sending oil sharply higher and dragging equities lower — even as US economic data prints surprisingly strong.

• Iran uranium standoff sends oil surging, equities retreating. Reuters reports Iran's Supreme Leader has demanded enriched uranium stay in-country, effectively stalling US-Iran negotiations. Crude jumped on renewed supply disruption risk, while Wall Street opened lower as investors reassess the geopolitical premium. UBS raised its oil price forecasts citing persistent supply-side concerns.

source: https://t.co/DshYaxZydG

• US manufacturing hits four-year high in May. The S&P Global flash PMI showed manufacturing activity at its strongest since mid-2022, while weekly jobless claims fell, reinforcing the narrative of a resilient US economy. The data complicates the Fed's easing calculus and supports the dollar's near-term bid.

source: https://t.co/DshYaxZydG

• US commits $2 billion to quantum computing. The federal government announced proposed funding awards to IBM, D-Wave, Rigetti, and GlobalFoundries, taking equity stakes in the process. Quantum computing shares spiked — a clear signal of accelerating government industrial policy in frontier tech.

source: seeking alpha

• ARM surges to all-time high; SoftBank follows. ARM Holdings hit record levels, pulling parent SoftBank higher in sympathy. The move extends the semiconductor rally driven by AI infrastructure buildout, though NVIDIA's post-earnings reaction was notably muted — margins at 75% but no China in forward guidance.

source: https://t.co/DshYaxZydG

• Parker-Hannifin to acquire Circor for $2.55B. The industrial conglomerate agreed to buy KKR-owned Circor, continuing the trend of strategic consolidation in industrials amid a manufacturing upcycle. The deal underscores strong corporate confidence in the sector's medium-term outlook.

source: https://t.co/DshYaxZydG

• Dollar holds near six-week peak; pound steadies on weak UK PMI. Bank of America maintains a near-term bullish dollar bias as yields stay elevated. Sterling found a floor despite UK business activity falling to a one-year low, with BoE's Taylor signaling less inflation persistence risk than 2022.

source: https://t.co/DshYaxZydG

Summary

Markets are caught between two forces: robust US economic fundamentals and escalating Middle East geopolitical risk repricing energy markets. The 🟡 mixed aggregate sentiment reflects this tension — risk assets face headwinds from higher oil and yields, but underlying economic momentum remains intact.

Quantillion Atlas — Researched Return (Jan 01–May 20, 2026, YTD)

Return: +1.93%

Sharpe: 0.45

Volatility: 8.43%

Max Drawdown: 5.78%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Iran #QuantumComputing #Semiconductors

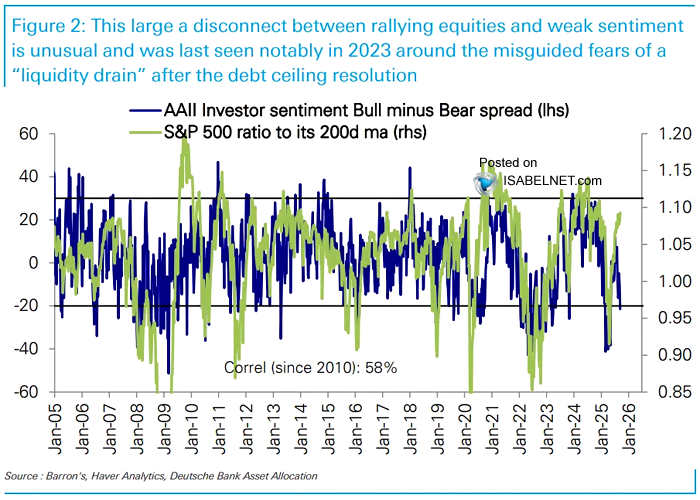

🇺🇸 S&P 500

Historically, very low investor sentiment has not only signaled caution but also suggested further upside in US equities, offering opportunities for contrarian investors

👉 https://t.co/yIk7SZYWVX

h/t @DeutscheBank $spx #spx#sp500#equities#stocks

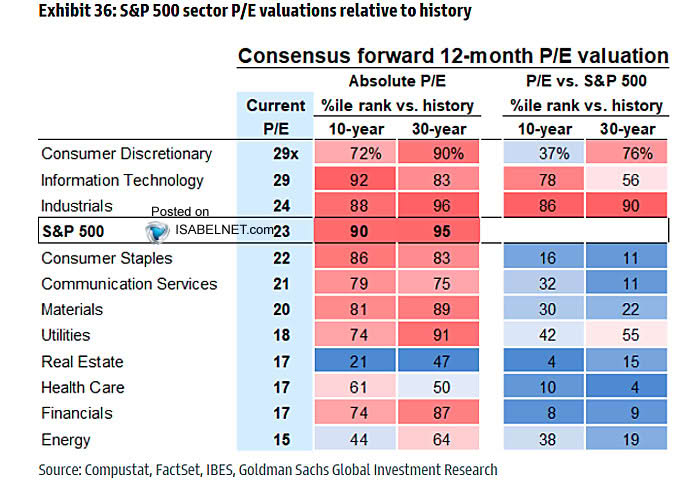

🇺🇸 Valuations

Historical data and sector-specific valuation metrics indicate that several S&P 500 sectors are still overvalued compared with their historical averages

👉 https://t.co/14i5SQWa4L

h/t @GoldmanSachs $spx #spx#sp500#stocks#equities