VC at @changeventures - backing top Baltic founders. Co-founder of @nodeswat. Pursuing opportunities to mend a few dents in the universe. Humour x empathy.

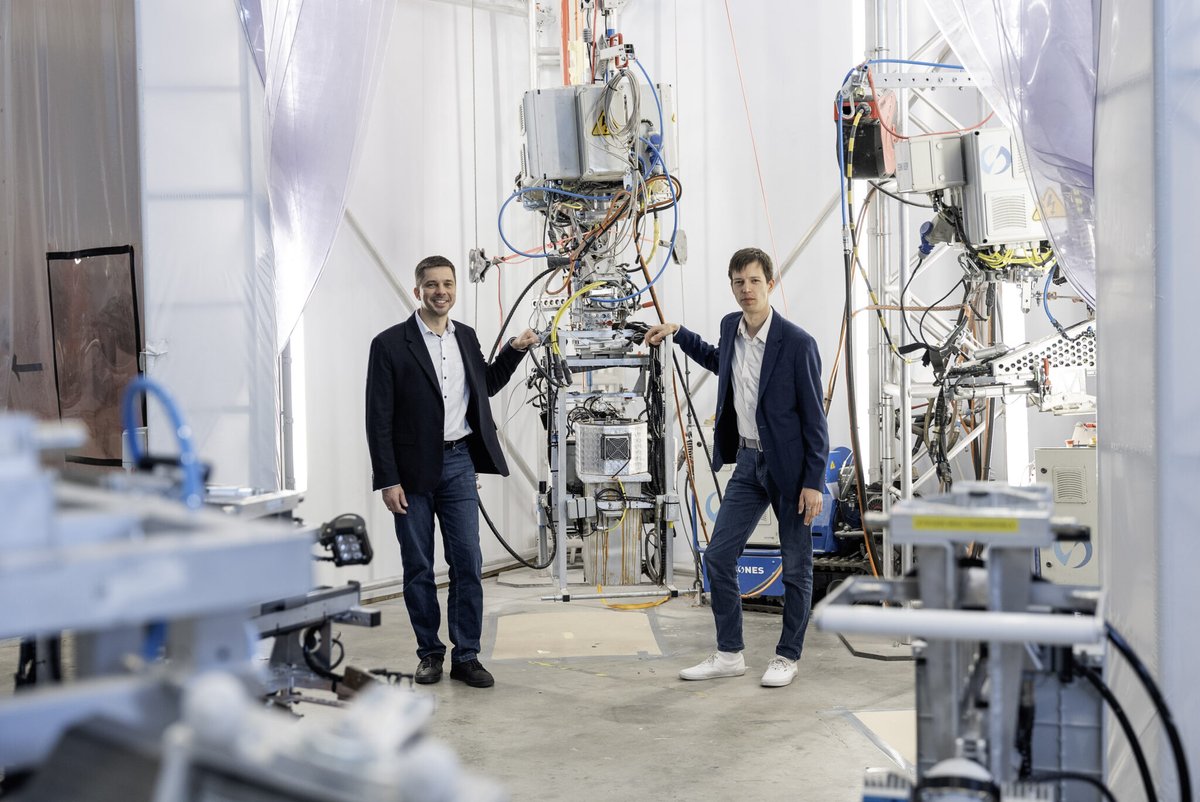

We are excited for our portfolio company @aerones_com who announced their $62M oversubscribed funding round today, co-led by Activate Capital and @S2Ginvestments. Another step towards scaling the market leader in robotic wind turbine inspection & repairs

https://t.co/BBBVVaJDA9

@fintechjunkie I can confirm your insightful posts have lately shown up less on my feed. Seems like Elon’s team is gathering intel to address this very issue. Maybe worth a reply from you? https://t.co/qxTKIBHubk

Entrepreneurship is like a high-stakes poker game.

You need to play the hand you're dealt rather than wait for the perfect one.

Accept the risks, make calculated bets, and sometimes, just bluff your way through.

Keep that poker face and dive in!

Entrepreneurship is like a high-stakes poker game.

You need to play the hand you're dealt rather than wait for the perfect one.

Accept the risks, make calculated bets, and sometimes, just bluff your way through.

Keep that poker face and dive in!

A few days ago I pulled out one of my generic pieces of advice because a Founder wasn't moving at startup speed. The advice:

“If something is worth doing, it’s worth doing poorly first.”

I've found it’s very common that many first time Founders are paralyzed by the fear that they'll get negative feedback about their product/idea and as a result they strive for a flawless launch. But the Startup journey doesn’t work that way.

Almost nothing worth achieving comes out perfect on the first try. Solving difficult problems requires iteration which means that feedback isn't failure --- it’s just the starting point. The sooner a Founder accepts that their initial launch might be rough (or even downright bad) the sooner they can take their critical first step.

I asked the Founder about other things in life that they had mastered. I asked about the journey from beginner to master and it was clear that their early attempts were shaky at best. I pointed out that this is how growth happens. Practice isn’t just repetition. It’s a cycle of failing, learning, and tweaking. Every stumble teaches you something, even if it’s just what not to do next time.

The trap is waiting for the “right moment” or the perfect plan. Spoiler: That moment doesn’t exist. Starting poorly beats not starting at all, every time. Waiting for perfection is the fastest way to guarantee failure because it keeps you and your team stuck in a fantasy land instead of iterating in the game.

My advice: Seek market feedback over perfection, get addicted to learning and stop being afraid of failure!

We are excited to release the latest Baltic Startup Funding Report, together with FIRSTPICK. Thanks to the kind founders sharing confidential data with us to help other founders calibrate in an opaque market🙏🙏🙏

https://t.co/iMmY79bDEJ

Painful lesson that I learned as an early stage startup investor is that the exit environment is 10x more important than the entry 📉

So, yes, I’m hopeful that things rebound this year in tech, but I’m counting on 2035 to be a banger year!

10x ARR still remains the standard in venture capital valuations

🤷♀️The question is 10x of what

⤴️If the start-up is growing insanely quickly, VCs will pay 10x your revenues 24 months from now -- vs today

This explains a lot of AI valuations that seem pretty high

"80% of my exit profits have come from pivots. I've been doing this for 10 years, what if I'm just a lucky fool? What if all of this is just random?"

(source: "Mike Maple's Pursuit of Truth through Pattern Breaking")

There are two possible explanations to the fact that a large number of successful VC outcomes are a result of pivots:

- Fund returns are primarily driven by portfolio strategy, and the influence of startup selection is greatly overestimated.

- A specific value of venture capital is that founders are able to change course. They aren't tied to a business plan, market or technology.

Both appear to be true, in that venture capital is a game of finding value in properly managed risk.

The more radical and disruptive a startup appears to be, the greater the exit potential — and the greater the underlying assumption it is built on. The larger that assumption, the more important it is that it be rapidly tested and validated.

Logically, it will often be the case that a startup will find a critical flaw in their assumption, and need to decide between pivoting or folding.

Teams that choose to pivot are acknowledging initial failure, the damaged trust with investors and employees, and the burned capital. Despite that, they have developed the conviction to attack the problem again from a new angle.

In fact, it turns out that 'high tech' startups are more likely to generate revenue after one pivot than they are with zero. That probability falls off again over subsequent pivots, reflecting the importance of identifying that critical flaw.

"Among high tech firms, the odds ratio of achieving revenue is highest after just one radical pivot, whereas among the general cohort the odds ratio is highest after three radical pivots."

(source: "To Pivot or Not To Pivot: On the Relationship between Pivots and Revenue among Startups")

What does this mean for VCs? Should they start selecting for startups that look one degree of separation away from a good idea? Obviously not.

You are looking for markers of competence, from the credibility of their propsition to how coherently they can talk about financials or logistics. You want to find people who love a problem, see their success as inevitable, but aren't dogmatic about how to get there.

A highly competent founder may fail, but they're also the most likely to be able to convert that failure into a successful pivot.

This runs up against two common biases in investment decision making:

1) Where there is a thematic bias on "how to get there". e.g. we can apply this great new technology to this industry and it will manifest a great business.

2) Where the uncertainty of early stage investing is used as justification to avoid the details, rather than using it to better understand founder competence.

An example for the first category is blockchain. It was believed that simply building a ledger for certain industries would create value. Disproving that assumption doesn't really give you fuel for a pivot. The same is true for AI today.

For the second category, consider the contempt that some early stage investors have for "made up" financial projections. You should care whether a founder understands revenue and cost factors if they are spending your money.

If an investment isn't working out, can you work with the founders to help them indentify the critical flaw in their initial assumption that may help them come back even stronger?

If you have selected highly competent and mission-driven founders, the chances are yes, you can.

I have invested in over 250 pre-seed startups, mostly in B2B software. The most successful ones have had some distribution tricks to quickly get their first happy customers.

Here are the Best (and worst) distribution wedges I have seen for Pre-Seed software startups.

If I could only give founders 20 seconds of advice after leading seed round, it’d prob be this: Keep your team small and your burn low while searching for PMF. Focus on learning, not selling. Don’t scale until you have a product customers love and a clear strategy for selling it.

Incredible example of an intense founder making things happen quickly, while also having the humility to accept & react to critical feedback. It's rare to see that combination of traits in a single person

@triinhertmann Word “divorce” originates from the Latin word “divortium” which means “separation”. Or in this case - separation between the advisor and his / her riches.

Startup went out to raise a $2m pre-seed, pre product. Didn’t happen so they raised $500k instead. Took a year to get to market and just signed a big customer. Looking back the team is really happy that they didn’t raise the $2m despite being cash strapped. They all agree that they would have spent the 💰faster than they should.

Hear, hear! Hence the preferred emphasis on the GTM strategy over “unique” idea. Also, most competitive landscape slides include obvious incumbents, but lack many of the newcomers who are not as famous (yet).

The inconvenient truth for most startups is that their ideas are obvious and they have many competitors selling very similar solutions.

The trick is distribution and messaging. Not product features.