How Britain Engineered History’s Greatest Financial Heist

By @shreehistory

I. The Stroke of Midnight

At the stroke of midnight on August 14, 1947, as the world watched the Union Jack descend over New Delhi and the saffron, white, and green of a new nation unfurl, history recorded a triumph of self-determination. The British Empire, exhausted by war and weakened by the inexorable tide of nationalism, was relinquishing its crown jewel. The romanticized narrative of the 20th century tells us that Britain granted India its freedom, an act of political magnanimity marking the end of colonial dominion.

But beneath the pageantry of lowering flags, the soaring rhetoric of Jawaharlal Nehru’s "Tryst with Destiny," and the chaotic tragedy of Partition, a very different kind of transfer was taking place. It was not a transfer of political power, but of financial liability.

In the quiet, wood-paneled chambers of the British Treasury and the Reserve Bank of India, a ledger was being closed. To the accountants and chancellors in London, Indian independence was less a geopolitical retreat and more a Chapter 11 bankruptcy filing, a meticulously orchestrated maneuver by which Britain effectively declared independence from its own creditor.

The colonizer owed the colonized a staggering fortune. And the colonizer was broke.

II. The First Extraction and the Silencing

To understand the audacity of the financial maneuvering of 1947, one must look back to the blueprint drafted three decades earlier, during the First World War. The great financial heist of the mid-century was not an anomaly; it was the perfection of a formula born in the trenches of Europe, paid for in the fields of Bengal.

When the First World War erupted in 1914, Britain found itself in desperate need of men, material, and money. It turned to its empire. India was coerced into contributing hundreds of millions of pounds to the British war effort, alongside the lives of over a million Indian soldiers. To finance this, the British Raj effectively commandeered India’s export earnings and heavily increased taxation, flooding the domestic economy with paper currency while draining its physical gold reserves. Britain abandoned the gold standard, but India was forced to maintain it, absorbing the inflationary shock.

By the war's end, the economic strain on the Indian populace was immense. Prices of essential goods had skyrocketed, and the returns on the capital extracted for the war were nowhere to be seen. As the Indian public began to realize the scale of this economic theft, dissent began to boil. Nationalist leaders pointed to the economic drain, exposing the arithmetic of imperial exploitation.

London’s response was not to remedy the extraction, but to legislate silence. In 1919, the British government passed the Anarchical and Revolutionary Crimes Act, widely known as the Rowlatt Act. The Act allowed for the incarceration of suspects without trial and curbed the free press, specifically targeting the dissemination of seditious materials, which in practice meant anyone explaining how the British were bankrupting the country. When protests erupted against this silencing, the British military responded with the Jallianwala Bagh massacre in Amritsar, killing hundreds of unarmed civilians.

The message was unequivocal: the colony would pay, and it would suffer in silence. The economic truth was to be suppressed by force. It was a precedent that would prove vital 28 years later, when the sums involved would be exponentially larger.

III. The Blank Check of World War II

By the time the Second World War began, the British Empire was already financially strained. The defense of the Middle East, Southeast Asia, and the British Isles required capital that London simply did not possess. Once again, the British turned to the vast, seemingly bottomless reservoir of the Indian economy.

To fund the massive mobilization of troops, the provisioning of armies, and the purchase of raw materials, the British Raj essentially wrote itself a blank check against the Indian taxpayer. India was declared a "non-self-governing territory" contributing to the war effort, but instead of paying India in hard currency for the goods and labor extracted, Britain credited the Reserve Bank of India with pounds sterling. These were not transferable funds; they were essentially IOUs, piling up in London as "Sterling Balances."

The human cost of this capital extraction was catastrophic. The most visceral manifestation of this economic drain was the Bengal Famine of 1943. While the British Treasury accumulated sterling balances, the diversion of grain and the financial extraction policies led to the starvation of an estimated two to three million people in Bengal. The Indian taxpayer was literally funding the survival of the British Empire with their lives and their livelihoods.

By 1945, the sheer scale of this extraction was breathtaking. Britain owed India roughly £1.3 billion. To comprehend the magnitude of this sum, one must view it not through the lens of modern consumer inflation, but as a share of the economy. In 1947, £1.3 billion represented roughly 13.5 percent of Britain’s entire Gross Domestic Product. If the British Treasury were forced to write a check for that proportion of its economy today, it would need to find approximately £350 billion.

It was a sum so massive that paying it in full would have instantly bankrupted post-war Britain, a nation that was, at that very moment, surviving on American Marshall Plan aid and rationed bread. The colonizer owed the colonized. And the colonizer had no intention of paying in full.

IV. The Safety Valve and the Negotiation

Facing the prospect of domestic economic collapse, the British government executed an audacious maneuver. The transfer of power in 1947 was not merely a political act; it was a financial release valve.

There is a historical curiosity, often unspoken in popular narratives, that complicates the story of India’s independence. The Indian National Congress (INC), the primary vehicle of Indian nationalism and independence, was not born from a grassroots peasant uprising, but was initially floated by a British colonial official, Allan Octavian Hume, in 1885. Historians have long debated the "safety valve" theory: the idea that Hume and the Viceroy engineered the creation of the INC to provide a controlled, institutional outlet for the rising frustrations of the Western-educated Indian elite, preventing a violent, uncontrollable rebellion.

While the INC evolved into a formidable force for independence under Mahatma Gandhi and Nehru, the institutional DNA of the organization was steeped in British legal and political frameworks. When it came time to negotiate the financial settlement of 1947, the lingering effects of this "safety valve" dynamic became apparent.

The negotiations over the Sterling Balances were brutal, conducted behind closed doors by the British Labour government’s Chancellor of the Exchequer, Sir Stafford Cripps, and the Indian delegation led by Nehru and Sardar Vallabhbhai Patel. Britain argued that a sudden withdrawal of £1.3 billion would crash the pound sterling, bankrupt the Sterling Area, and trigger a global financial crisis. The threat was explicit: if India demanded its money, the ensuing chaos would ensure India received nothing.

India was in a state of profound vulnerability. The subcontinent was engulfed in the horrific trauma of Partition; millions of refugees were on the move, and the new government was struggling to establish basic administrative continuity. In this moment of existential crisis, the Indian leadership accepted terms that effectively castrated its own wealth.

The 1947 agreement dictated that the vast majority of the £1.3 billion would be "blocked." Only a fraction was immediately released; the remaining £1.15 billion was locked in London, to be doled out in agonizingly slow installments over a decade or more. Worse, the agreement stipulated that these blocked balances would earn little to no interest. By accepting this compromise, the post-colonial government effectively agreed to a structural haircut on the asset, surrendering the real-time economic utility of the money to save the British economy from default.

The safety valve had, once again, operated exactly as designed.

V. The Alchemy of Devaluation

With India's massive claim successfully trapped in the vaults of the Bank of England, Britain weaponized the only tool it had left: the currency itself.

Having forced India to accept deferred payments, Britain engineered a stealth default through the alchemy of foreign exchange. On September 18, 1949, just over two years after Indian independence, the British government unilaterally announced a massive devaluation of the pound sterling. The pound’s value against the US dollar was slashed overnight from $4.03 to $2.80, a devaluation of 30.5 percent.

Because India’s sterling balances were, by the very terms of the 1947 agreement, denominated in pounds, this overnight maneuver was an economic earthquake. It instantly vaporized almost one-third of the purchasing power of the money owed to India. If India wanted to use those sterling balances to buy American machinery, Canadian wheat, or Swiss capital goods, they would find that nearly a third of their money had vanished into the ether.

Britain, on the other hand, enjoyed a sudden, massive windfall. The real value of the debt owed to India was slashed by a third with the stroke of a pen. India was bound by the Sterling Area agreement and had to devalue the rupee proportionately, tying its currency to the declining fortunes of the British pound and further devastating its import capacity. It was a financial ambush, executed with the cold precision of an actuary.

VI. The Central Bank’s Quiet Payout

As if this financial evisceration was not sufficient, the final insult was administered at the very heart of India’s financial system.

The Reserve Bank of India (RBI), the nation's central bank, had been established in 1935 under British colonial rule as a privately owned entity. Its shareholders were a mix of private banks, financiers, and investors, a group that included substantial British and colonial-era capital.

Just after independence, the Indian government recognized the strategic necessity of nationalizing the central bank. The RBI (Transfer to Public Ownership) Act was passed in 1948, and the bank was officially nationalized on January 1, 1949.

The terms of this nationalization reveal a profound asymmetry in the post-colonial transition. When the Indian government took ownership of the RBI, it did not simply seize the assets. It compensated the private shareholders handsomely. Under Section 4 of the 1948 Act, the compensation was calculated not at a discounted state rate but based on the average market price of the shares on the Bombay Stock Exchange during the months preceding the Act. Because RBI shares, with a face value of one hundred rupees, were trading at a premium of roughly fifty percent on the open market, the total payout from the Indian exchequer to the 500,000 private shares was approximately 7.5 crores.

But the generosity of the settlement did not end with a cash buyout. Under Section 4(2) of the Act, the shareholders were given the option to take their compensation in Government of India promissory notes bearing a guaranteed interest rate of three percent per annum. This was a staggering mechanism of financial alchemy. The British and colonial-era investors were effectively allowed to convert their equity in India's central bank into risk-free sovereign debt backed by the newly independent Indian taxpayer. They could hold these 3 percent government papers and collect a perpetual stream of interest, ensuring that the extraction of wealth from the subcontinent continued long after the political transfer of power.

The juxtaposition is staggering, bordering on the absurd. Private shareholders of India’s central bank were paid out in full, at peak market valuations, and handed guaranteed interest-bearing bonds. Meanwhile, the Indian public, who had already paid for Britain’s survival in two world wars through forced extraction and inflation, was left holding devalued, blocked IOUs that had just lost a third of their value in the currency markets.

The private investors were made whole. The Indian public was made paupers.

VII. The Durgapur Paradigm: The Empire Strikes Back

The long shadow of this financial subjugation played out in the subsequent decades, dictating the trajectory of the newly independent nation’s development.

By the late 1950s, India had launched its Second Five-Year Plan, an ambitious push to industrialize. But the country was facing a severe balance-of-payments crisis. The sterling balances had been largely drawn down to pay for essential imports, and the country was running out of foreign exchange. India needed to build three major steel plants to fuel its industrialization. The Soviet Union stepped in to fund the Bhilai Steel Plant; West Germany funded the Rourkela plant. Britain, eager to maintain its commercial foothold, wanted the contract for the Durgapur Steel Plant.

Rather than releasing any lingering goodwill or acknowledging the massive debt still technically being dribbled out, Britain offered a new arrangement. In 1958, the UK government extended a fresh £100 million loan, a "new" line of sterling credit, to India.

This was not a repayment of the wartime debt; it was fresh financing. The British government essentially told India: We will lend you this new money, but you must use it to buy British goods. The money flowed straight back into the pockets of a British consortium of steelmakers, subsidizing the post-war British heavy engineering industry.

The Indian taxpayer, who had already funded the British war machine, was now taking on new debt to buy British machinery, because the money they were originally owed had been blocked, devalued, and structurally dismantled. The cycle of financial dependency had been perfectly preserved.

VIII. Amnesia and the True Cost of the Union Jack

Today, the historical amnesia surrounding these events is profound. The narrative of 1947 is frozen in the amber of political triumph: the lowering of the flag, the end of empire, the dawn of a new era. Mainstream histories focus on the geopolitical maneuvering, the tragedy of Partition, and the drafting of a constitution. The great financial heist remains obscured in the shadows of central bank archives and Treasury minutes.

The Indian population has been kept largely in the dark about the arithmetic of their own subjugation. The textbooks speak of the political transfer of power, but rarely of the transfer of financial liability. The £350 billion equivalent that was extracted, blocked, devalued, and systematically stripped of its value is a phantom limb in the national memory.

When the viceroys departed, Britain did not just walk away from the subcontinent; it walked away from an invoice it could not afford to pay. It declared independence from its own empire. Through a masterclass in financial engineering, leveraging the Rowlatt-era instinct for suppression, the "safety valve" of institutional compromise by a party supposedly fought for freedom and did deals behind the doors, the blunt instrument of currency devaluation, and the quiet payouts of risk-free bonds to colonial shareholders, Britain managed to offload the cost of its own survival onto the very people it had colonized.

Independence was not a gift. It was a getaway car. And the true price of the Union Jack's descent was paid not by the British taxpayer, but by the millions of Indians whose sweat and starvation funded an empire, only to be handed a worthless IOU in return.

References and Further Reading

Bhattacharya, S. (1997). The Colonial State and the Monetary System in India. Oxford University Press.

Bhowani, B. R. (1965). India's Sterling Balances. International Monetary Fund (IMF) Staff Papers, Vol. 12, No. 1, pp. 1-42.

Chandavarkar, A. (1989). The Imperial Bank of India and the Reserve Bank of India: A Study in Central Banking Transition. Oxford University Press.

Datta, B. (1949). The Devaluation of the Rupee. The Indian Economic Journal, Vol. 1, No. 1, pp. 1-12.

Hume, A. O. (1885). The Indian National Congress: A Retrospect.

Keynes, J. M. (1946). The Balance of Payments of the United Kingdom.

Mukerjee, M. (2010). Churchill's Secret War: The British Empire and the Ravaging of India during World War II. Basic Books.

Reserve Bank of India. (1948). The Reserve Bank of India (Transfer to Public Ownership) Act, 1948. RBI Historical Archives.

Sarkar, S. (1989). Modern India: 1885-1947. Macmillan.

Tomlinson, B. R. (1979). The Political Economy of the Raj 1914–1947: The Economics of Decolonization in India. Macmillan.

(All rights reserved. You must get written permission if you want to republish)

Twitter users can share, repost, like, comment but please provide attribution to @shreehistory who did all this research.

श्री राम मन्दिर दान प्रकरण से जुड़ी FIR से प्रतीत होता है कि ट्रस्ट को @narendramodi और @myogiadityanath की छवि से ज्यादा चंपत राय, अनिल मिश्रा और गोपाल राव की इमेज की चिन्ता है। इस मामले में बार-बार यही सन्देश जा रहा है कि सरकार की मंशा साफ नहीं है।

My column: In Tibet, China is attempting the systematic erasure of a people's culture, language and identity by targeting their children.

It has forcibly placed more than one million Tibetan children into state-run, Mandarin-language boarding schools, which are built on a neo-imperial premise: "Control the child and you control the future."

This is not simply a human-rights scandal, but a geopolitical project with far-reaching implications for Asia’s future balance of power and India’s security. https://t.co/2rV0aKClJR

Since 2023, Ujjain has been at the centre of a series of major infrastructure and urban development projects announced by the Madhya Pradesh government.

An Indian Express investigation has found that during this period, members of Chief Minister Mohan Yadav’s family purchased 168 acres of land in and around the city. Much of this land is located in areas that have benefited from new road projects or changes allowing residential and commercial development.

The report found that 111 acres are situated near key road projects announced by the government. Some family members have also secured contracts linked to the development of these areas.

The findings have renewed questions over potential conflicts of interest, with the opposition alleging that planning decisions favoured areas where the Chief Minister’s family held land. The family said it has been in the real estate business since 2010 and cannot stop conducting business because it is related to the Chief Minister.

Express investigation by: Jay Mazoomdaar

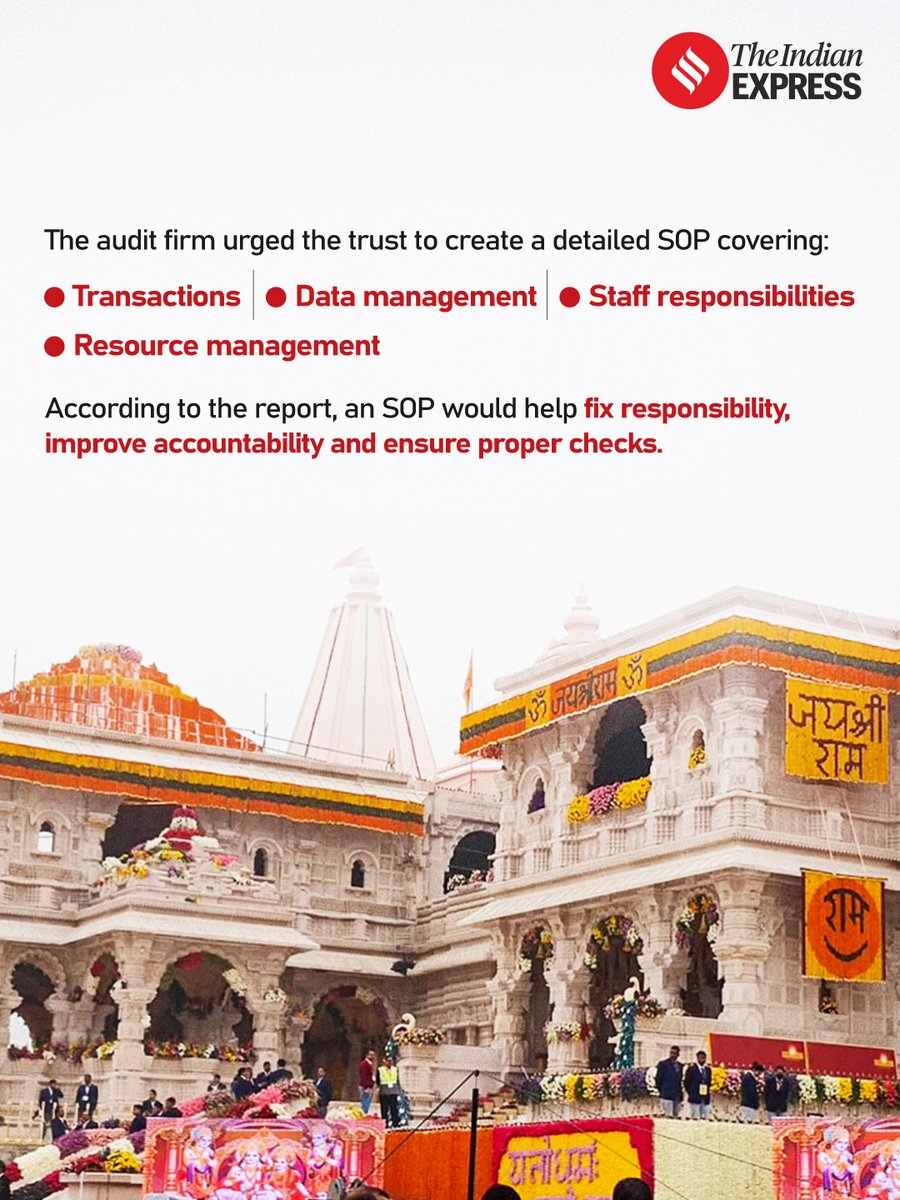

Six years before an SIT began probing allegations of irregularities in Ram Temple donations, a private audit firm had warned of serious gaps in the trust’s systems.

A 2020 audit flagged the absence of a systematic record of donations, weak data management and the lack of a standard operating procedure (SOP).

The report cautioned that poor oversight could lead to accountability and reporting issues.

Written by: Shyamlal Yadav

Click on the 🔗 below to read full article.

https://t.co/Exq4yT84bD

मोहन यादव के परिजनों के जमीन का कारोबार पुराना है मगर उसमें होने वाली बरकत में जो उछाल पिछले 5 साल में आया है, वह विचारणीय है। पिछले 5 साल में 253 एकड़ जमीन खरीदी। उसके पहले कुल 82 एकड़ जमीन थी। मोहन जी के परिजनों के पास फिलहाल 335 एकड़ जमीन है।

अगर सरकार को लग रहा है कि वह मीडिया मैनेजमेंट के माध्यम से जनभावनाओं को मैनेज कर सकेगी तो दुखद है। यूपीए-2 में ऐसी ही सोच तत्कालीन आलाकमान की थी। आज भी पीएम @narendramodi देश के सबसे लोकप्रिय नेता हैं, मगर वह इन्दिरा गांधी भी थीं। हर लोकप्रियता का एक ब्रेकिंग प्वाइंट होता है।

A (gentle) shout-out to Objective Journalism: The same Jay Mazoomdaar broke the Robert Vadra land scam in Express 12 years ago, and last year, called out Trump’s lie about USAID funding Indian elections.

🚨#𝐄𝐱𝐩𝐫𝐞𝐬𝐬𝐈𝐧𝐯𝐞𝐬𝐭𝐢𝐠𝐚𝐭𝐢𝐨𝐧 | Our investigation found that Madhya Pradesh Chief Minister Mohan Yadav's family and their real estate firms acquired at least 137 plots spanning 168 acres in Ujjain for ₹45 crore in two years since December 2023 — mostly in areas benefiting from road projects and land-use changes his government announced. Here is a quick look at how much land each of his family members own

🔗 https://t.co/FEMW9VBzrO

#ExpressInvestigation | At the core of the Yadav family’s land holding structure are Mohan Yadav’s first cousins Govind and Nilesh Yadav.

Other land purchasers in the Yadav family — either directly or through family-owned realty companies — include Mohan Yadav himself, his wife Seema, son Vaibhav, daughter-in-law Shalini, brothers Narayan and Nandlal, sister Kalavati, Narayan’s wife Rekha, and their son Abhay.

https://t.co/Fl8EvdUsP5

मोहन यादव के चचेरे भतीजे ने एक्सप्रेस से पूछा है कि सीएम उनके परिवार से हैं तो क्या वे कारोबार बन्द कर दें! मेरा सुझाव है कि कारोबार बन्द मत कीजिए बल्कि और जमकर कीजिए.....क्योंकि देश को 2047 तक विकसित भारत बनाना है।

@IndianExpress

Most of us grow up with the stories of Mahabharata.

Yet, we never understand it well enough and know the true account of this incredible epic.

With this online course by @BhandarkarI, we seek to introduce you to the epic world of the greatest epic in the world.

ALAS, THE WORST FEARS APPEAR TO BE COMING TRUE. THERE APPEARS TO BE A SCAM IN THE NAME OF RAM LALLA. AND HERE'S WHY IT IS MORE THAN AN ACT OF CRIMINAL IMPROPRIETY.

The latest is that the SIT is preparing legal action against Champat Rai aide Tinnu Yadav in the Ram Mandir donation theft probe, sources say. Cases may also be registered against donation-counting staff and bank officials. Arrests are possible. Complainant Anil Mishra alleges no receipt was issued for donated gold and claims he was later told the gold had already been melted down.

It is deeply painful to be reporting these details. The Ram Mandir isn't just a bricks-and-mortar tribute to a deity. It is much more than that. It is a symbol that consecrates the reclamation of Hindu civilizational heritage. A heritage that was first endangered by settler colonisation and later by a political ideology that wrongly portrayed any attempt to reclaim or appreciate the grandeur of Hindu civilization as an assault on secularism.

That is precisely why these allegations are so troubling. One would have thought that the symbols of this great project to reclaim Hindu heritage would have been safest in the hands of those who led the movement. It is now incumbent upon these self-styled "guardians of the faith" to prove themselves by ensuring they do not become complicit in the very acts of vandalism and desecration they have long fought against.

This book was published in 1916 by Benaras Hindu University...

Not available now. All the copies got destroyed. One copy was available in the library of California University, which has been digitised by Microsoft. It is a beautiful introduction to Hinduism, without any school affiliations. It is especially suited to youth. You may go through at leisure. It has 304 pages and share it further with your known younger generation kids. This is a rare book on “Sanatana Dharma” - Please READ and share it to our youth group as much as possible... https://t.co/pKkRmqtP6d

Shri Nitin Gadkari ji had promised INDIA petrol would be available at Rs 15/ litre, once blended with Ethanol! We understand he gave "big talks" but atleast give us a discount on petrol blended with Ethanol & not charge ₹160/ litre for pure petrol. Also: EV policy?

#EthanolScam

टोडाभीम तहसील के तहसीलदार साहब रिकॉर्डिंग करने से नाराज़ हो गए और एक महिला को मरने पीटने लगे, महिला का आरोप है गलत तरीके से हाँथ लगाया तहसीलदार साहब ने, तहसीलदार साहब का कोई कुछ नहीं बिगड़ सकता क्योकि तहसीलदार साहब का नाम दिनेश मीणा बताया जा रहा है

The RSS’s legal status has once again come under scrutiny after Congress leader Priyank Kharge questioned why the organisation continues to function without registration. The RSS maintains that registration is not legally required, arguing that Indian law does not make it compulsory for associations of individuals to register and that its legal status has been recognised by courts and governments over the years.

While the debate is not about the legality of the RSS, it centres on whether an organisation of such scale and influence should remain outside the registration framework followed by most modern institutions. The RSS traces its origins to 1925 as a social movement focused on character-building rather than a conventional organisation, and has long operated through a decentralised structure with participation-based membership.

The issue continues to draw attention because of the RSS’s nationwide presence, century-long existence, and influence through a wide network of affiliated organisations, most of which operate through registered trusts, societies or unions.

Click on the 🔗 below to read the article.

https://t.co/RSv8WgfJ3O