These two titans of the sport and, in their own words, greatest rivals, have literally redefined the meaning of rivalry. Nobody has ever seen or will ever see this in any competitive sport. Role models and living examples of sportsmanship!

#FedalForever

EVERY Sector of the AI Boom 🚀

AI isn’t a single industry.

It’s creating winners across dozens of sectors and trillions of dollars in investment opportunities.

Here’s the COMPLETE AI Value Chain and the stocks leading each segment 👇

Messi, sin que le pregunten por él, habla de Nadal.

🗣️ "Estoy viendo ahora el documental de Rafa Nadal. Me identifico mucho con él. Los dos siempre queremos dar el máximo"

Leo tiene buen gusto.

⚽🎾Lionel Messi’s admiration for Rafa Nadal highlights the values that define true champions:

Hard work ✔️

Resilience ✔️

Humility ✔️

Constant improvement ✔️

Values that inspire every day at the @rnadalacademy

https://t.co/ecI8p4NIP4

This dip is an opportunity to buy stocks in the data centre value chain:

$AMD — CPU/GPU designer for PCs, servers, AI. Fabless via TSMC.

$VRT — Power and cooling infrastructure for data centers.

$ANET — Makes high-speed networking switches and software for cloud data centers.

$MU — Makes DRAM and NAND. Key HBM supplier for AI.

$NBIS — GPU cloud and AI infrastructure. Former Yandex spinoff.

$VST — Power generation operator. Leverages data center electricity demand.

When $SPY crashes 10%-20% this summer, everything will be on sale.

Add these 16 stocks for the reversal of a lifetime:

1. $NOW — AI automates every enterprise workflow at scale

Buy zone: $85–$100 | Near 52-week lows, massive AI re-rating

2. $BE — Fuel cells powering AI data centers off the grid

Buy zone: $200–$220 | $ORCL deal de-risks demand story

3. $ASTS — Satellite broadband direct to your phone, globally

Buy zone: $65–$70 | Post-earnings flush, thesis intact

4. $GOOG — Gemini + TPUs + Search = AI moat unmatched

Buy zone: $300–$320 | Key support, 52-week low area

5. $LITE — Optical switches are the nervous system of AI

Buy zone: $600–$700 | Pulled back from $1,000+, still growing 85% YoY

6. $MU — HBM memory is the oxygen inside every AI server

Buy zone: $700–$750 | Key support after Broadcom-induced selloff

7. $SNDK — NAND flash storage exploding on AI inference demand

Buy zone: $1,100–$1,200 | Bull flag on the weekly chart

8. $TE — Data center power infrastructure, critical AI backbone

Buy zone: $6–$7 | Oversold, government energy tailwinds building

9. $RKLB — Launch provider + space systems for AI-connected satellites

Buy zone: $80–$90 | Pulled back hard, $816M SDA contract intact

10. $AAOI — 800G transceivers shipping to hyperscalers at scale

Buy zone: $120–$130 | Volatile beta, best entry on deep dips

11. $NVDA — Designs the GPUs that run every AI model on earth

Buy zone: $165–$175 | 52-week support zone, Jensen demand still intact

12. $ONDS — Drones + autonomous rail powering AI-enabled defense

Buy zone: $7–$8 | Near prior base breakout level

13. $IONQ — Trapped-ion quantum computers for post-classical AI computing

Buy zone: $27–$40 | 52-week range low, government funding tailwind

14. $AMD — EPYC + MI300X chipping away at NVDA's AI market share

Buy zone: $350–$360 | Key technical support from prior consolidation

15. $ARM — Architecture inside every AI chip ever designed

Buy zone: $220–$240 | Pulled back from highs, royalty model scales forever

16. $ORCL — Cloud infra + AI database layer for the enterprise

Buy zone: $130–$140 | Near 52-week lows pre-earnings catalyst

Remember, when $SPY sells off, you should the strong companies and hold for a massive move back towards $820+ by year end.

♻️ RESHARE this post and write 1 comment, I'll DM you my $SPY contract I'm getting for 1000% winner

Rafa 🤝 Zizou

Rafael Nadal et Zinédine Zidane réunis pour un relais inoubliable lors de la cérémonie d'ouverture des Jeux Olympiques de #Paris2024 🔥

Aujourd'hui, la légende de @rolandgarros fête ses 40 ans 🎂

#JeuxOlympiques

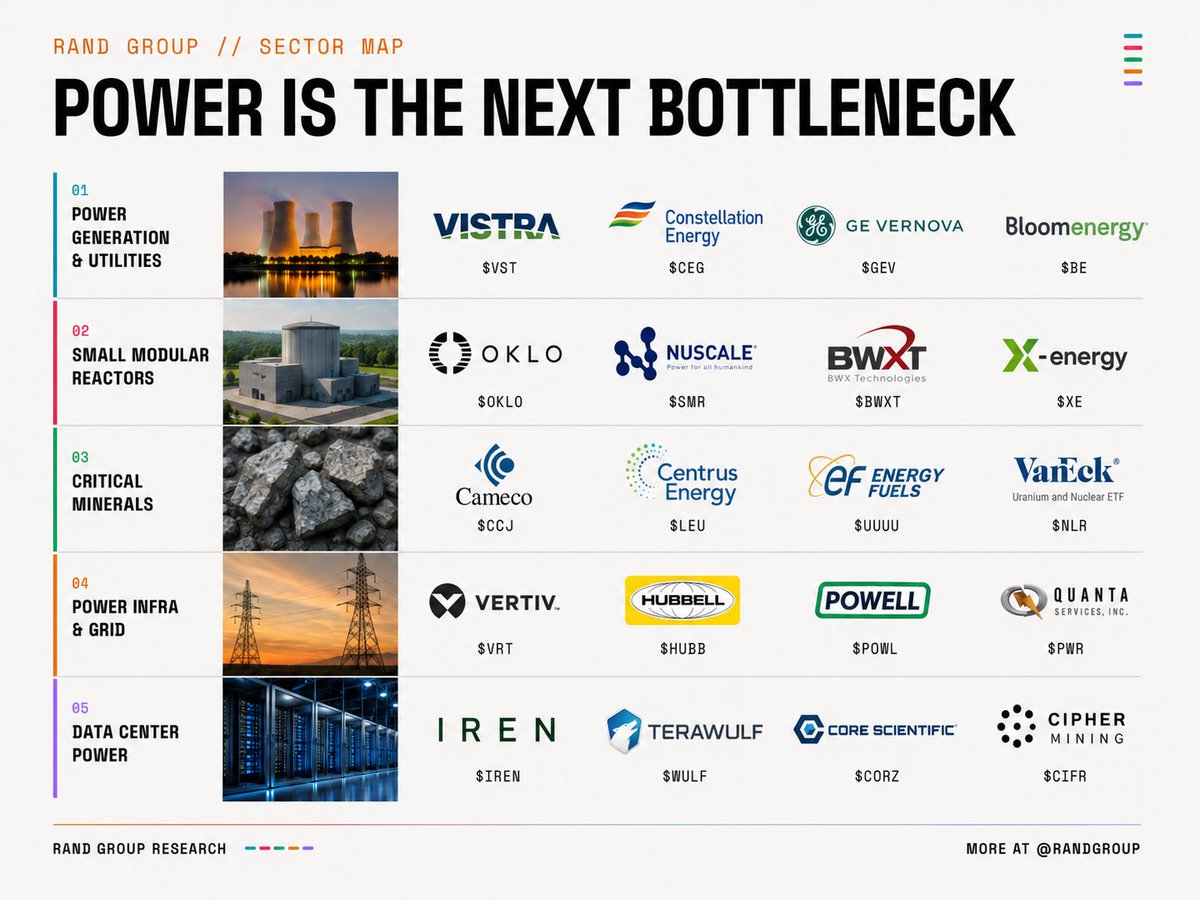

Every hedge fund I respect is suddenly talking about the same thing, and... it is not the chips.

It is the one bottleneck that breaks the entire AI story if it is not solved. Around 20 public companies sit on it. I put them all in one map across 5 layers.

Let's dive into it 🧵

Here is the thing nobody priced in two years ago. We spent a decade with flat electricity demand in this country. Utilities planned around it. Then AI showed up asking for gigawatts at a time.

The Electric Power Research Institute now thinks data centers could eat 9% to 17% of all US electricity by 2030, up from roughly 4% in 2023. Former Google CEO Eric Schmidt told Congress the sector may need 67 more gigawatts by the end of the decade. That is not a tweak to the demand curve. That is a new industrial revolution landing on a grid built for a different century. Every company below sits somewhere between a power plant and a server rack. This is the map.

🔌 POWER GENERATION & UTILITIES

Start at the source. These are the companies that actually make the electrons. For years this was the most boring corner of the market: regulated returns, slow growth, dividend investors only. Then the hyperscalers started signing power contracts directly with generators, and the whole category repriced.

$VST Vistra

This is the one I watch most closely in the group. Vistra signed Meta to a power purchase agreement for roughly 2,600 megawatts at its PJM nuclear sites, which tells you everything about where this is going: tech giants are now buying nuclear output directly. Q1 2026 adjusted EBITDA hit a record for a first quarter at $1.494 billion. They have hedged almost all of their 2026 generation, and they have bought back about 30% of the company since late 2021. A generator that trades like a buyback machine with an AI tailwind bolted on.

$CEG Constellation Energy

The largest nuclear fleet in the country, and the company that put nuclear back on the front page when it agreed to restart Three Mile Island for Microsoft. In January it closed the $21.8 billion Calpine acquisition, adding around 23 gigawatts of mostly gas and renewable capacity, and Q1 2026 revenue more than doubled the year before to $11.1 billion. The thesis is simple: when an AI company wants carbon free baseload power tomorrow, there are very few phone numbers to call, and this is one of them.

$GEV GE Vernova

If you only own one name in this entire map, my honest take is that it should probably be this one. GE Vernova makes the gas turbines and the grid equipment, the literal picks and shovels of the buildout. In a single quarter its Electrification segment booked $2.4 billion in data center equipment orders, more than it booked in all of 2025. Total backlog sits around $163 billion and management pulled forward its $200 billion target to 2027. The gas turbine backlog jumped from 83 to 100 gigawatts in one quarter, and they are raising prices into that demand. This is the cleanest expression of the trade.

$BEPC Brookfield Renewable

Note the ticker: this is Brookfield Renewable, $BEPC, not the $BE on most charts (that is Bloom Energy). Brookfield operates about 47 gigawatts and is developing a pipeline north of 200. It signed a framework with Microsoft to deliver over 10 gigawatts, roughly eight times the size of the largest single corporate power deal ever signed before it, plus a multi gigawatt hydro deal with Google. It also owns about half of Westinghouse alongside Cameco. The patient, contracted, dividend paying way to play the same wave.

⚛️ SMALL MODULAR REACTORS

Now the speculative end. The promise here is clean, firm baseload power in a compact box you can site right beside a data center. The catch: almost none of these are producing commercial power at scale yet, so you are buying a timeline as much as a company. Price that carefully.

$OKLO Oklo

The most exciting and the most expensive name in the room. In May the NRC approved the principal design criteria for Oklo's Aurora powerhouse in under half the usual review time, a real regulatory step forward. The customer pipeline is around 14 gigawatts, anchored by a 12 gigawatt agreement with Switch and a 500 megawatt deal with Equinix, and it added a research partnership with NVIDIA and Los Alamos. Just remember Oklo plans to build, own and operate its reactors and has essentially no revenue yet. This is a call option on a 2028 plus story.

$SMR NuScale Power

The one with the regulatory lead. NuScale has NRC design approval for both its 50 and 77 megawatt modules, which genuinely derisks deployment. It is sitting on about $1.2 billion in liquidity and is working toward a definitive power agreement with TVA through its ENTRA1 partner, with its first project tied to RoPower in Romania. Revenue was a rounding error last quarter because the licensing work wrapped up, so this is still a story about getting the first units in the ground.

$BWXT BWX Technologies

The adult in the room, and the name I would own if I wanted nuclear exposure without buying a lottery ticket. BWXT actually makes money: Q1 2026 revenue of $860 million and net income of $91 million, and it raised full year guidance. It builds reactors for the US Navy, produces medical isotopes, and just acquired Precision Components Group to push into commercial nuclear manufacturing. While the SMR startups sell the future, this one sells into it today.

$XE X-energy

Brand new to the public market. X-energy IPO'd on April 24 at $23 a share, raised about $1.02 billion, and came out around a $12 billion valuation with Amazon as its anchor backer holding nearly a third of the company before the listing. It pairs an 80 megawatt reactor design with its own proprietary TRISO fuel, and its order book already tops 11 gigawatts including Amazon's commitment to as much as 5 gigawatts by 2039, plus Dow and Centrica. Reality check: it lost about $390 million on $109 million of revenue in 2025, and first deployments are not expected until the early 2030s.

⛏️ CRITICAL MINERALS

You can build every reactor on the list above and they are paperweights without fuel. This is the front end of the cycle: mining, enrichment, conversion, and the magnet metals the whole grid runs on. Quick note: I swapped the misfiled Northland slot for Energy Fuels here, which is a genuine US critical minerals producer.

$CCJ Cameco

The blue chip of the uranium world. Q1 2026 net earnings jumped 87% and adjusted EBITDA rose 44% to $509 million on stronger prices and volumes. The kicker is Westinghouse: Cameco owns roughly half of it alongside Brookfield, so it captures both the fuel and the reactor technology side of the renaissance. When people want uranium exposure without a science project, they buy this.

$LEU Centrus Energy

The reshoring play, and a fascinating one. Centrus is the only production ready uranium enricher in America, sitting on a $2.3 billion enrichment backlog, a $900 million HALEU award from the Department of Energy, and a notice from the NNSA that it intends to sole source enrichment work to them. It is pouring over $560 million into its Oak Ridge centrifuge factory and is even exploring a fuel joint venture with Oklo. This is a national security story wearing a stock ticker.

$UUUU Energy Fuels

This is what $UUUU actually is. Energy Fuels runs White Mesa, the only conventional uranium mill operating in the United States, and it is the rare company licensed to produce both uranium and separated rare earth oxides under one roof. Its 2026 uranium guidance implies growth of 50% to 150%, and it is now turning out the dysprosium, terbium and magnet metals that everything from EV motors to grid hardware depends on. Uranium and rare earths, the two supply chains Washington is most desperate to pull back from China, in one company.

$NLR VanEck Uranium and Nuclear ETF

If you would rather own the whole theme in one line instead of picking a winner, this is the basket. $NLR holds the nuclear value chain end to end: reactors, enrichers, miners and the utilities running the plants. A lot of this very map sits inside it, with Constellation, Cameco, Centrus, BWXT and Energy Fuels all among its largest positions. The lazy way to be right about the sector even if you pick the wrong individual stock.

🔧 POWER INFRA & GRID

Between the power plant and the server rack is the least glamorous and maybe most investable layer of all. Transformers, switchgear, cooling, and the crews who build it. The dirty secret of the AI buildout is that the grid itself is the bottleneck. Interconnection queues run years, and the equipment to connect anything is on backorder.

$VRT Vertiv

The purest grid adjacent winner so far. Q1 2026 sales rose 30% to $2.65 billion, with the Americas up 44% on data center demand, earnings per share up triple digits, and guidance raised twice in two quarters. Vertiv makes the power and thermal systems that keep a data center alive, and it just joined the S&P 500. When the chip names sneeze, this one catches it, but the order book keeps validating the story.

$HUBB Hubbell

Boring on purpose, and that is the point. Hubbell makes the electrical and utility hardware, the transformers, metering and grid components, that every new data center and every grid upgrade quietly requires. It will never 10x in a year, but it sells into both the AI buildout and the broader grid replacement cycle at the same time. This is the ballast in the basket.

$POWL Powell Industries

My favorite quiet story in this section. Powell makes custom electrical equipment for utilities, energy and now data centers, and the demand signal is screaming: orders up 97% last quarter, a record $1.8 billion backlog, and right after the quarter closed it landed a single data center order worth more than $400 million, the largest in its history. It did a three for one split this spring and carries no debt. A small cap industrial running into a structural tailwind.

$PWR Quanta Services

The labor. Quanta physically builds and upgrades the grid, the part of this problem that no software fixes. Q1 2026 revenue rose 26% to $7.87 billion and its backlog hit a record $48.5 billion. If all of the generation and transmission above actually gets built, a meaningful slice of it gets built by crews like these. The pick and shovel play on the wires themselves.

🖥️ DATA CENTER POWER

The wild card, and the highest beta corner of the map. These started as bitcoin miners, which means they already owned the one thing everyone now wants: large blocks of interconnected power and the land around it. They pivoted to hosting AI compute, signing leases with the hyperscalers and the neoclouds. Enormous growth, real execution, and serious single customer risk. Size accordingly.

$IREN IREN

The furthest along. Formerly Iris Energy, IREN has a Microsoft AI cloud partnership worth billions, a power pipeline around 4.5 gigawatts, and high performance computing on track to make up the majority of its revenue by the end of the year. It already trades like an infrastructure company rather than a miner, because increasingly that is what it is.

$WULF TeraWulf

TeraWulf describes itself as a power company that happens to build digital infrastructure, which I think is exactly the right framing for this whole row. It has locked in over $12.8 billion of contracted compute revenue through long term leases with the Google backed Fluidstack and Core42, anchored by its Lake Mariner site and scaling toward a gigawatt of power. Its leasing revenue more than doubled year over year. Controlled power, leased to AI, on a multiyear contract.

$CORZ Core Scientific

The contrarian one. CoreWeave tried to buy Core Scientific in an all stock deal, and in a rare moment of shareholder backbone, the holders voted it down in late 2025. So it stays public, and it kept the prize: roughly $10 billion or more of contracted revenue with CoreWeave across about 590 megawatts, while converting its old mining sites into AI colocation. You are betting the company creates more value alone than the buyout offered.

$CIFR Cipher Mining

The earliest stage of the pivot, rebranding toward AI as it goes. Cipher signed a hosting deal backed by Google's Fluidstack, with Google taking around a 5% stake, plus a 300 megawatt arrangement tied to AWS, building toward a contracted compute backlog around $9 billion. Highest risk, least proven, most torque if the leases convert to cash on schedule.

⚡️FINAL THOUGHTS

Step back from the tickers and a pattern jumps out. The market is paying up for the same insight at five different points on the same wire.

The stability lives at the bottom and the middle. Cameco, Hubbell, Quanta Services and BWX Technologies make money today and sell into a buildout that is contracted for years. They will not triple overnight, but they do not need a single thing to go right that has not already happened.

The growth lives at the edges. GE Vernova is the rare name that has both, scale and acceleration, which is why I keep coming back to it. The reactor startups and the former miners are where the imagination is, and also where the disappointment will be when timelines slip, because timelines always slip in nuclear and in construction.

The clearest read of all is that the AI story quietly handed the baton from the chip layer to the power layer, and most people are still watching the wrong race. You cannot run the model without the electrons, and the electrons are the scarce thing now.

I will say the obvious part out loud: this is a map, not advice. I am pointing at where the money is moving, not telling you what to buy. Do your own work on every one of these, especially the speculative names where a single contract or a single regulator can move the whole thesis.

If this saved you a week of research, do me a favor and bookmark it, then send it to the person in your group chat who only owns Nvidia. The power bottleneck is the second half of that trade.

Happy @RafaelNadal Day to tennis fans around the world 💙

And to celebrate the legend's 40th birthday, we've got 40 hours of Nadal playing on the Fast channel - access it via https://t.co/5yu0xiEN62!

My favorite humanoid stocks ranked:

1. $AMBA (Ambarella) — Best pure-play edge AI vision for robotics. 37% revenue growth, 60% gross margins,$100M+ robotic pipeline, still under $5B market cap. The risk is concentration and scale. The upside is being the de facto vision processor as robots proliferate.

2. $6324.T (Harmonic Drive) — Irreplaceable. There is no substitute for strain wave reducers in high-precision robot joints. 75% market share with Nabtesco. Hard to replicate. If humanoid robots ship in any volume, this company prints money.

3. $ALGM (Allegro MicroSystems) — Near-monopoly in motor current sensing, priced like an auto cyclical. 30-50 sensors per humanoid at automotive-tier P/E multiples. The market hasn’t re-rated this for robotics yet.

4. $VPG (Vishay Precision Group) — The purest humanoid hardware play. Precision load cells and force sensors with a 1.21 book-to-bill. Risk: trading at 255x current earnings on ~$320M revenue. If humanoid volumes slip, this gets crushed. But if they don’t, VPG is the most direct bet on robot touch.

5. $MOG.A (Moog) — Aerospace-grade precision actuators with a credible humanoid crossover. Already up 83% on the thesis but the volume ramp hasn’t started. Defense + robotics optionality.

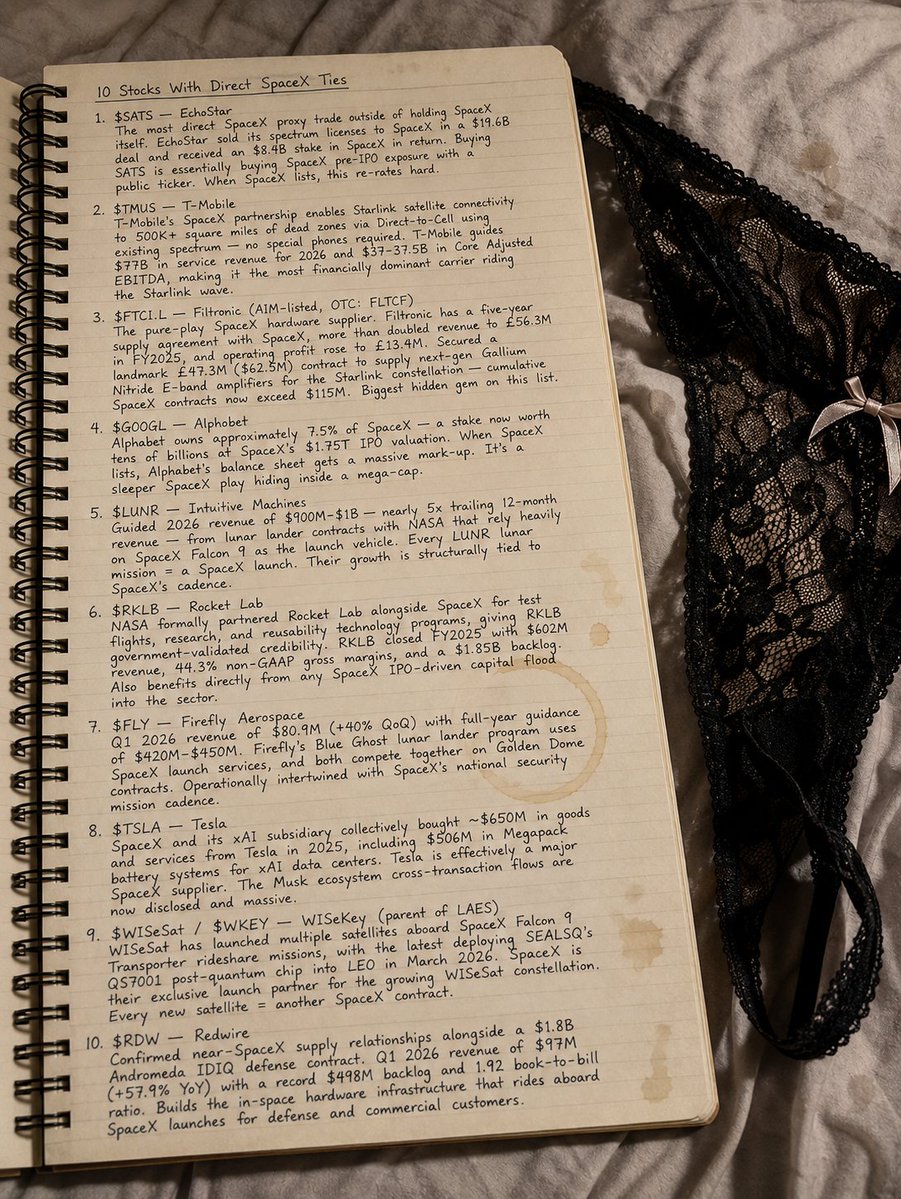

My girlfriend says she'll buy and hold $SPCX like marriage when it IPO on June 12.

She'd have $40,000,000 if she held $NVDA since its IPO with $10,000.

There's 10 stocks with direct SPACEX partnerships:

1. $SATS — EchoStar

The most direct SpaceX proxy. Sold spectrum licenses to SpaceX in a $19.6B deal and received an $8.4B SpaceX equity stake in return. Buying SATS = buying pre-IPO SpaceX exposure with a public ticker.

2. $TMUS — T-Mobile

SpaceX partnership delivers Starlink Direct-to-Cell coverage across 500K+ square miles of dead zones no special hardware needed. Guides $77B in service revenue and $37–37.5B EBITDA for 2026. Most financially dominant carrier riding the Starlink wave.

3. $FLTCF — Filtronic (OTC / AIM: FTC.L)

Pure-play SpaceX hardware supplier. Five-year supply agreement with SpaceX; revenue more than doubled to £56.3M in FY2025 with £13.4M operating profit. Landmark £47.3M contract to supply next-gen GaN E-band amplifiers for Starlink cumulative SpaceX contracts now exceed $115M. Biggest hidden gem on this list.

4. $GOOGL — Alphabet

Owns ~7.5% of SpaceX worth tens of billions at SpaceX's $1.75T IPO valuation. When SpaceX lists, Alphabet's balance sheet gets a massive mark-up. Sleeping SpaceX exposure inside a mega-cap.

5. $LUNR — Intuitive Machines

Guiding 2026 revenue of $900M–$1B nearly 5x trailing revenue from NASA lunar contracts that rely on SpaceX Falcon 9 as the launch vehicle. Every LUNR mission = a SpaceX launch. Growth is structurally tied to SpaceX cadence.

6. $RKLB — Rocket Lab

NASA formally partnered Rocket Lab alongside SpaceX for test flights and reusability research. FY2025: $602M revenue, 44.3% non-GAAP gross margins, $1.85B backlog. Also benefits directly from any SpaceX IPO-driven capital surge into the sector.

7. $FLY — Firefly Aerospace

Q1 2026 revenue $80.9M (+40% QoQ), full-year guidance $420M–$450M. Blue Ghost lunar lander launches on SpaceX rockets. Both compete together on Golden Dome contracts operationally intertwined.

8. $TSLA — Tesla

SpaceX and xAI bought ~$650M in Tesla goods in 2025, including $506M in Megapack battery systems. Tesla is effectively a major SpaceX supplier. The Musk ecosystem cross-transaction flows are now publicly disclosed and massive.

9. $WKEY — WISeKey (parent of $LAES)

WISeSat has launched multiple satellites aboard SpaceX Falcon 9 Transporter missions, with the latest embedding SEALSQ's QS7001 post-quantum chip into LEO. SpaceX is their exclusive launch partner — every new satellite = another SpaceX contract.

10. $RDW — Redwire

Q1 2026: $97M revenue (+57.9% YoY), record $498M backlog, 1.92 book-to-bill ratio. Builds in-space hardware that rides aboard SpaceX launches for defense and commercial customers. Winning large IDIQ defense contracts alongside SpaceX.

♻️ RESHARE this post and make 1 comment for my list of 1000% movers like $ASTS and $IONQ.