Trading below net cash ($3.36 vs. $2.57). Minimal debt. FCF breakeven. Gaining market share in a stabilizing industry (+ potential for regulatory tailwinds). New high margin segment w/ two customer wins already secured. Strong operating leverage. Disciplined capital allocation w/ active buybacks and an accretive acquisition pipeline. Insiders own over a third of the company… etc. etc. $PEW

New pitch - GrabAGun Digital - $PEW

Available in bio.

TLDR

_PEW trades at a 20% discount to the cash on its balance sheet

_The core business outgrows its industry 15% a year on average, and is break-even on its way to profitability

_It has a new business line that’s very high margin and could make it a multi-bagger

Without dismissing the possibility of a strategic alternative, $RCMT's recent delays and lack of communication have prob been due to the audit situation first revealed in the latest 10-K as a "material weakness in internal control" that led it to reappoint its old auditor. The issue has now been resolved.

Apart from that, biz momentum is accelerating w/ Energy Services backlog doubling yoy and the company hiring for "multiple concurrent infrastructure programs and projects" related to $CIFR.

On another note, sell-side full-year outlooks have stayed largely unchanged out of conservatism, citing "potential upside in Engineering Services with the building book of business in Energy Services," leaving room for beats through the remainder of the year.

Is $RCMT getting acquired?

Closing the Q3 call, Exec Chairman Bradley Vizi said: "We look forward to our next update in March."

March arrived, but Vizi didn't. For the first time in its history, the company did not host an earnings call: "The Company will not be holding a conference call to discuss these results."

Are they in a quiet period? Mgmt has gone dark. To the best of my knowledge, attempts to contact IR are going unread or unanswered.

The answer might be buried in last year's proxy filings. For the first time since his appointment eight years ago, the company amended and restated Vizi's Executive Severance Agreement.

Under the amendment, Vizi's golden parachute multiplier in the event of a Change in Control was increased from 2.0x to 2.99x his highest annual bonus over the preceding 5 years, plus the subsequent year at target (previously just a 3-year lookback).

Canceled call + radio silence + revised CIC payouts. Something big is going on.

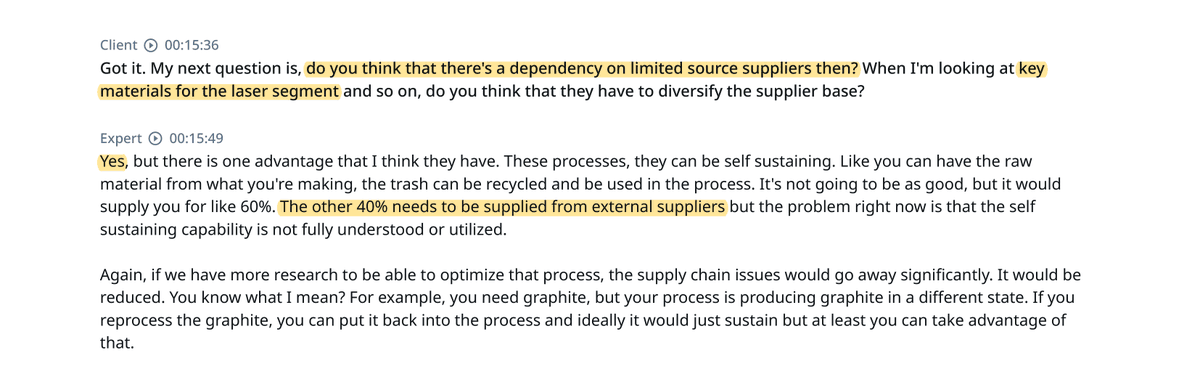

$SCIA looks interesting again after a breakout quarter. Trading at single digit run-rate EPS w record backlog, no debt and 99%+ of revs tied to the photonics industry.

SCIA's sputtering targets (mainly ITO) show up in dozens of peer-reviewed studies next to Coherent's excimer lasers. Acc to an industry expert, Coherent sources ~40% of its materials externally.

Mgmt attributed a big part of the breakout quarter to new products launched last year. They introduced two, but they consistently flag one: a new ITO formulation.

$Usio Announces First Quarter 2026 Financial Results

• Revenue Up 16%, Beats Consensus by 9%

• Adjusted EBITDA1 of $0.8 Million Beats Consensus by 12%

• All-time Record Quarterly Revenue, Processing Volume and Transactions

• Total payment dollars processed through all payment channels up 28% versus the prior year period

Earnings release: https://t.co/1uljGSGxQp

Re next week's earnings, $USIO is an interesting setup.

In 2025, the company posted 2.5% revenue growth vs. its historical run-rate of at least 10%, primarily due to a single client event, the loss of a major reverse-ATM program at an amusement park customer (likely Six Flags), which masked its otherwise strong underlying performance.

Despite the one-off loss of this high-volume client, USIO quickly restored its rev run-rate by Q3 2025 and now faces relatively easy comps throughout 2026.

While the rev recovery was fast, there was a jump in opex, w mgmt now expecting expenses to be "flat with maybe some moderate growth," adding that "you shouldn't see that type of jump."

At the last conf call in late March, w most of Q1 already gone, mgmt said its highest-margin ACH segment showed no signs of slowdown, "as it looks like Q1 could be painless and ACH's best quarter ever. As you can tell, I'm excited about Q1 and all of 2026."

"I think we've been pretty clear in our message that Q1 for ACH is going to be another record, which will be our third consecutive quarter of setting all-time records for ACH. We're in the real-time payments department, and from this debit, that will also set a record. Card processing will also set a record, so that includes payfac. So Q1 is going to be exciting."

In the longer term, there are "three large card issuing projects," w two expected to come online in Q3 for a more backend-weighted 2026. "You will see those programs go live in the third and fourth quarter and give us a nice jump at the end… we've got tons of deals that are in implementation that if we could flush them all today, we'd be very excited for the year and probably raising guidance."

Let's see.

Re next week's earnings, $USIO is an interesting setup.

In 2025, the company posted 2.5% revenue growth vs. its historical run-rate of at least 10%, primarily due to a single client event, the loss of a major reverse-ATM program at an amusement park customer (likely Six Flags), which masked its otherwise strong underlying performance.

Despite the one-off loss of this high-volume client, USIO quickly restored its rev run-rate by Q3 2025 and now faces relatively easy comps throughout 2026.

While the rev recovery was fast, there was a jump in opex, w mgmt now expecting expenses to be "flat with maybe some moderate growth," adding that "you shouldn't see that type of jump."

At the last conf call in late March, w most of Q1 already gone, mgmt said its highest-margin ACH segment showed no signs of slowdown, "as it looks like Q1 could be painless and ACH's best quarter ever. As you can tell, I'm excited about Q1 and all of 2026."

"I think we've been pretty clear in our message that Q1 for ACH is going to be another record, which will be our third consecutive quarter of setting all-time records for ACH. We're in the real-time payments department, and from this debit, that will also set a record. Card processing will also set a record, so that includes payfac. So Q1 is going to be exciting."

In the longer term, there are "three large card issuing projects," w two expected to come online in Q3 for a more backend-weighted 2026. "You will see those programs go live in the third and fourth quarter and give us a nice jump at the end… we've got tons of deals that are in implementation that if we could flush them all today, we'd be very excited for the year and probably raising guidance."

Let's see.

Interesting move on $CVV, now trading back below its est. $7.50+ liquidation value.

• ~$23 million pro forma cash after the SDC division sale.

• Real estate valued at $30+ million value. The 355 Building was listed for $28.5 million in 2022 and the company has retained its Saugerties facility.

• A new data center theme first appeared in Q2 2025, with mgmt adding three slides just last month expanding on the data center opp.

• Validated tech from a just announced collaboration with Stony Brook University.

• Potential linkage to an SiC wafer manufacturer that recently received $2 billion from $NVDA, adapting its epitaxy tech for data center use cases.

Disc: Long.

InfoArb + Special Situation + 1st mover advantage = Why microcaps!

Last Friday: Tip comes in on $CVV

This Monday: Email alert on special situation set-up, so our subs are informed ~$6.20

Wednesday: Full report ~$6.50

Thursday: $.6.78; Friday: $8.27

Wish it always worked this way, but odds are best in microcaps

From $RCMT Q3 call: "We see opportunities to get more involved on the data center front selectively… the most obvious opportunity is the interconnect aspect of it because the reality is each of these major data centers requires substations to be built, and that’s obviously directly in our wheelhouse.

…even just adding 1 or 2 incremental core clients a year, it can really move the needle… historically, [utility] capex spend might have been $2 billion or $3 billion. Now it’s at maybe $5 billion or $6 billion. And then some of them are moving up another level to… $8 billion to $10 billion a year. And the lion’s share of that is going towards hardening the grid.

So it’s an exciting time for sure."

So it turns out $RCMT is part of a $20B+ data center buildout for the world's top hyperscalers, including Amazon and Google.

The company is currently hiring for an "industrial-scale data center" client. Based on verbatim text overlap and exact footprint matches, I've linked this partner to $CIFR.

Referring to the data center opp, RCM's mgmt said that "even just adding 1 or 2 incremental core clients a year, it can really move the needle."

The first incremental core client has been landed. And its pipeline equates to nine "brand new giant Manhattan skyscrapers."

@TalkSoonCapital "1. Represents a nondiscretionary safe by a plan established by the Reporting Person on December 7, 2023 in a manner intended to satisfy the requirements of Rule 10b5-1."

Is $RCMT getting acquired?

Closing the Q3 call, Exec Chairman Bradley Vizi said: "We look forward to our next update in March."

March arrived, but Vizi didn't. For the first time in its history, the company did not host an earnings call: "The Company will not be holding a conference call to discuss these results."

Are they in a quiet period? Mgmt has gone dark. To the best of my knowledge, attempts to contact IR are going unread or unanswered.

The answer might be buried in last year's proxy filings. For the first time since his appointment eight years ago, the company amended and restated Vizi's Executive Severance Agreement.

Under the amendment, Vizi's golden parachute multiplier in the event of a Change in Control was increased from 2.0x to 2.99x his highest annual bonus over the preceding 5 years, plus the subsequent year at target (previously just a 3-year lookback).

Canceled call + radio silence + revised CIC payouts. Something big is going on.

Something strange going on with $RCMT. Excerpt from today’s GEO morning email… maybe not a big deal.. but still interesting. Stuff you see by actually reading PR and scripts… not just relying on AI. Been fun collaborating with @realLigerCub

So it turns out $RCMT is part of a $20B+ data center buildout for the world's top hyperscalers, including Amazon and Google.

The company is currently hiring for an "industrial-scale data center" client. Based on verbatim text overlap and exact footprint matches, I've linked this partner to $CIFR.

Referring to the data center opp, RCM's mgmt said that "even just adding 1 or 2 incremental core clients a year, it can really move the needle."

The first incremental core client has been landed. And its pipeline equates to nine "brand new giant Manhattan skyscrapers."

So it turns out $RCMT is part of a $20B+ data center buildout for the world's top hyperscalers, including Amazon and Google.

The company is currently hiring for an "industrial-scale data center" client. Based on verbatim text overlap and exact footprint matches, I've linked this partner to $CIFR.

Referring to the data center opp, RCM's mgmt said that "even just adding 1 or 2 incremental core clients a year, it can really move the needle."

The first incremental core client has been landed. And its pipeline equates to nine "brand new giant Manhattan skyscrapers."

The market is slow...

$WATT - "In parallel, the Company is advancing a growing number of proof-of-concept initiatives across retail, manufacturing, and foodservice, including grocery and a quick-service restaurant operator. Several of these programs are structured to scale from initial site deployments to broader multi-location rollouts in the near term."

Re $WATT, the Walmart deployment may not even be the largest:

"This is the largest public deployment of Ambient IoT [...] and the second largest overall after the other open secret project with a major online retailer (Amazon)." - ABI Research

Public infra from Wiliot shows POCs w/ McDonald's, Whole Foods, Mondelez, and 7-Eleven, among others. McDonald's btw seems to already be running here: https://t.co/sCEeNuQ9Pm

Source: view-source:https://t.co/U5l2jcZSk7

Beyond the $22B IVAS/SBMC program advancing through prime contractor selection, $VTSI is bidding on a separate $50M contract expected to land by September. Management says their tech has already "exceeded requirements."

![realLigerCub's tweet photo. From $RCMT Q3 call: "We see opportunities to get more involved on the data center front selectively… the most obvious opportunity is the interconnect aspect of it because the reality is each of these major data centers requires substations to be built, and that’s obviously directly in our wheelhouse.

…even just adding 1 or 2 incremental core clients a year, it can really move the needle… historically, [utility] capex spend might have been $2 billion or $3 billion. Now it’s at maybe $5 billion or $6 billion. And then some of them are moving up another level to… $8 billion to $10 billion a year. And the lion’s share of that is going towards hardening the grid.

So it’s an exciting time for sure."](https://pbs.twimg.com/media/HG2P66ma4AAAgYg.jpg)

![realLigerCub's tweet photo. Re $WATT, the Walmart deployment may not even be the largest:

"This is the largest public deployment of Ambient IoT [...] and the second largest overall after the other open secret project with a major online retailer (Amazon)." - ABI Research

Public infra from Wiliot shows POCs w/ McDonald's, Whole Foods, Mondelez, and 7-Eleven, among others. McDonald's btw seems to already be running here: https://t.co/sCEeNuQ9Pm

Source: view-source:https://t.co/U5l2jcZSk7](https://pbs.twimg.com/media/HDD8xU_XoAAp_IG.png)