$GME Q1 2026 EARNINGS REPORT:

1. Operating income reached $143.3 million, compared to just $10.8 million a year ago. ✔️

2. Net income came in at $389.6 million, up from $44.8 million last year. ✔️

That represents roughly a 770% increase year-over-year.

3. Revenue grew 14% YoY to $835.3 million.

Many expected continued sales declines but GameStop posted solid top line growth this quarter 😮💨

4. SG&A expenses declined to $201.6 million from $228.1 million despite higher sales.

5. GameStop ended the quarter with $9.7 billion in:

Cash

Marketable securities

Digital assets

Related receivables

Derivative collateral

Including:

$8.4B cash and marketable securities

$1.0B derivative collateral

$0.4B digital assets

• THE BREAKING NEWS HERE:

6. The Board approved a new $2.0 billion share repurchase authorization through June 2029.

At a share price around $21:

$2B could retire roughly 95 million shares

More than 20% of the current share count

This does not mean they will immediately buy shares, but management now has the authority to do so whenever they see fit.

Three things matter most:

Revenue growth returned.

Operating profit surged.

A $2B buyback authorization was approved.

The bear thesis that GameStop is simply a declining retailer becomes much harder to defend when the company is producing record operating profits while sitting on nearly $10 billion of liquidity and assets. ✍🏻

GameStop reports highest quarterly net income in company history of $389.6 million. Highest first quarter operating income in GameStop’s history of $143.3 million. Net sales grew 14% year-over-year, driven by collectibles. Cash, marketable securities, digital assets and related receivables, and collateral pledged for derivative asset of $9.7 billion.

https://t.co/BAu3T6V9w4

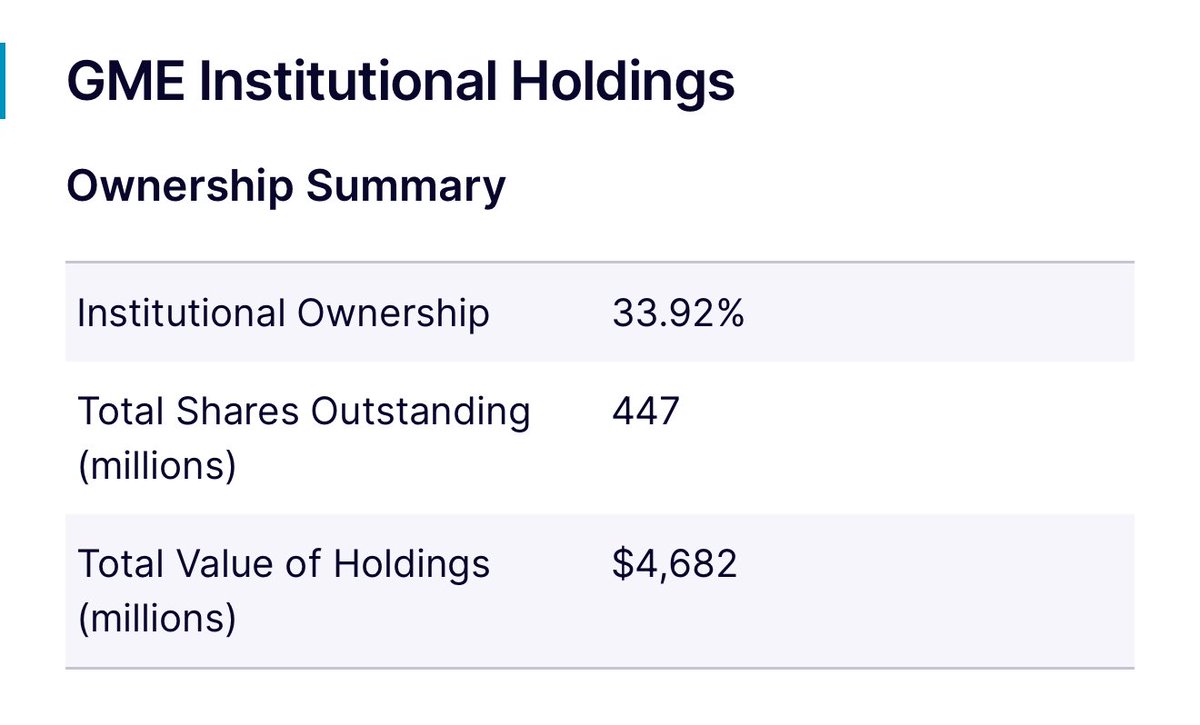

On May 13th, $XRT had 3.5 million FTDs.

That same day, the total number of XRT shares outstanding was 3 million.

There were more FTDs on a single day than shares outstanding.

The Hollow Men

American capitalism is rotting from the head down. We have replaced the "Owner-Operator"—the risk-taker-with a new, parasitic class of corporate bureaucrat: The Risk-Free Insider.

By "Insider," I am not referring to a specific title. I am referring to the entire administrative state that has captured the modern corporation. This includes the Directors who exist solely to collect fees, the Executives who exist solely to collect bonuses, and the Managers who exist solely to hire consultants.

These are the hollow men of the boardroom. They are masters of PowerPoint. They wear the right suits. They say the right buzzwords about "governance" and "ESG." But they are mercenaries fighting a war with someone else’s ammunition.

In a functioning economy, authority is tied to liability. If you make a bad decision, you lose your own money. That fear of loss is the only thing that keeps a business honest. It forces you to cut waste, obsess over the customer, and stay late to fix what is broken.

Today, we have severed that link.

We have rigged the game so that heads, the Insider wins; tails, the shareholder loses.

If the stock goes up, the Insider collects a massive performance bonus. If the stock crashes due to their own incompetence, they are fired with a "Golden Parachute" worth tens of millions. They are gambling with the house’s money, and they never leave the table poorer than they arrived.

This looting starts in the boardroom.

We have normalized a "Country Club" culture where directors are selected based on social profiling rather than their ability to build a business. The modern board member is often a professional tourist—paid an average of $350,000 a year.

Let’s be brutally honest about what that number represents. The average director is paid nearly five times the GDP per capita of the United States. They earn more for attending four quarterly lunches than the vast majority of Americans earn in five years of hard labor.

And for what?

Most of these directors are "over-boarded," sitting on three or four boards simultaneously. They treat directorships as a gig economy for the elite. They fly in, rubber-stamp a compensation package they didn't read, and fly out. They collect checks from companies they do not understand, do not use, and certainly do not love.

They are not there to ask hard questions. They are there to be collegial. They are there to protect the other Insiders.

And what happens when these boards hire executives who also have no personal capital at risk?

We get the Delegation Economy.

When a Risk-Free Insider faces a crisis—bloated expenses, a broken supply chain, or a stale product—they do not roll up their sleeves. They hire a consultant. They pay a strategy firm millions of shareholder dollars to produce a 100-page deck telling them what they already know.

This is not management. It is intellectual money laundering.

They use shareholder capital to buy an insurance policy for their own careers. If the plan fails, they can blame the consultants. They delegate the work because they are terrified of the responsibility. They would rather preside over a slow, comfortable decline than risk a bold mistake.

While American Insiders are busy optimizing their severance packages, our global competitors are optimizing their products. They are not slowed down by bureaucracy. They are not waiting for a slide deck. They are outworking us.

If we continue to fill our C-suites with administrators instead of operators, we will lose our edge. We will see iconic American franchises hollowed out by fees, managed for the benefit of the Insiders, while the true owners—the shareholders—are left holding the bag.

The time for polite governance is over.

If we want to save the American economy from mediocrity, we must demand a return to the "Owner’s Mentality." We need leaders who treat shareholder capital with the same reverence they treat their own savings. The era of the Risk-Free Insider must end.

Final Stop GameStop: The Jig is Up

In Part 1, I outlined how he arrived on the scene – we had a talk in 2019 about GameStop and investing. The Chewy founder then made a big splash as an activist with a Form 13D filing later in 2020.

He has held on with the diamondest hands.

Ryan, the current Executive Chairman, CEO and owner of now about 9% of GameStop stock, ascended to this dual role in September 2023.

Let’s take a look at the business as it stands today.

Here I will introduce the Scion Analyst Template, in parts. This is a Microsoft Word template I put together for my wayward analysts early in 2006. The idea was to get everyone thinking my way about analyzing stocks.

I will now, as I would have in 2006, analyze GameStop stock by working through the template one section at a time.

https://t.co/zlBh9sWfGK

Is this why the @SECGov pushed short reporting requirements to 2028??

“75% of ALL equity trades are executed by 5 firms

Citadel 25%

Virtu 20%

Hudson River Trading 15%

Jane Street 10%

SIG 5%..”

@FlyEaglesFly529

Ban Payment for Order Flow

@Hamnakedshorts@POTUS

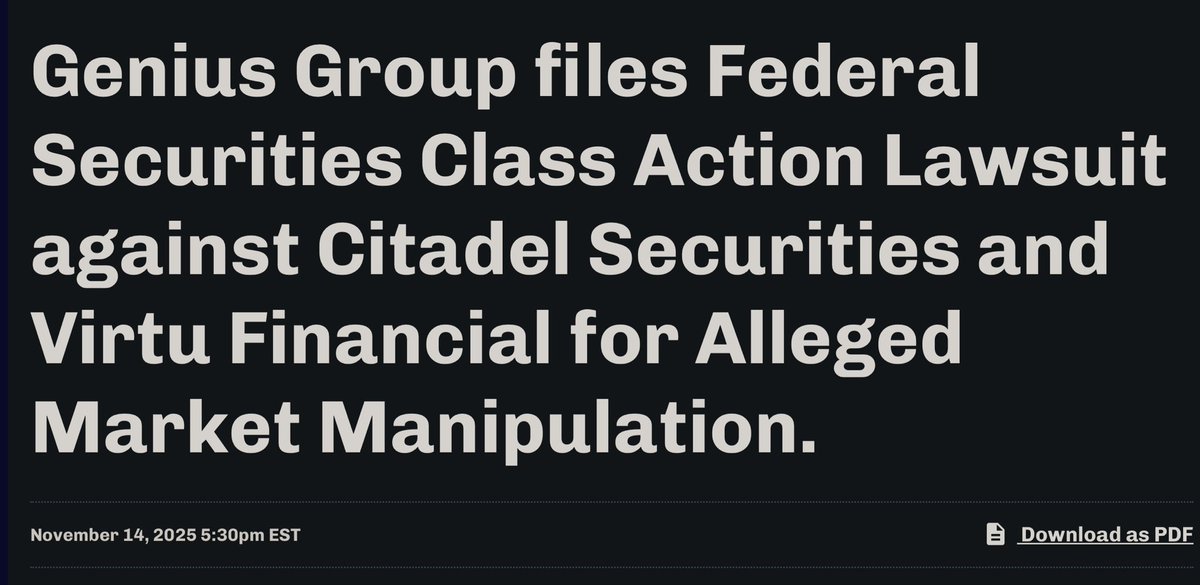

Latest $GNS news - Genius Group Limited (NYSE American: GNS) (“Genius Group” or the “Company”), a leading AI-powered, Bitcoin-first education group, today announced it has filed a Class Action Complaint in the United States District Court for the Southern District of New York alleging that Citadel Securities LLC, and Virtu Americas LLC (the "Defendants") engaged in a long-running market manipulation scheme that includes spoofing and naked short selling of the Company’s shares and related acts in violation of Section 10(b), Sections 9(a)(2) and 9(e) and Section 20(a) of the Securities Exchange Act of 1934.

The Company believes the lawsuit sets a number of precedents with regards to the protection of shareholder interests and the Company. As such, the Company is taking action to recover damages caused due to alleged market manipulation:

> This lawsuit is a Class Action Complaint filed on behalf of the Company and ALL of its investors who sold Genius Group stock at artificially deflated prices as a result of Defendants’ alleged abuses.

> Pursuing a class action will help the Company facilitate a recovery not just for Genius Group’s losses, but for all its harmed shareholders as well.

> The Company will ask the Court to appoint it “lead plaintiff” in the class action, so that the Company can effectively manage the litigation and diligently work to protect its shareholders’ interests.

The class action complaint filed today that Defendants engaged in longstanding and widespread manipulative trading scheme centered on repeatedly “spoofing” Genius Group stock. “Spoofing” is a manipulative and illegal trading practice that involves submitting and then cancelling buy or sell orders without any genuine intent to execute them.

The purpose of these “baiting orders” is to mislead other market participants about the level of supply and/or demand for a security, or about the degree of price volatility associated with a security, and thereby influence market prices for that security.

The complaint alleges that for a period of at least three years – between April 12, 2022 and May 30, 2025 (the “Class Period”) – Defendants repeatedly entered thousands of spoofing trades designed to create the false impression that there was both excess supply and excess volatility in Genius stock.

The Company has confirmed that the lawsuit seeks at least the previously reported no less than $250 million in damages (The Company believes actual damages to be far greater)

These manipulative orders were calculated to (and successfully did) deceive or induce other investors to sell their holdings at artificially deflated prices. In particular, the complaint alleges:

>> On 98% of all trading days during the Class Period, Defendants repeatedly entered spoofing trades designed to manipulate the price of Genius stock. Defendants entered dozens – sometimes thousands – of such trades on a given trading day, canceling them within milliseconds of placement.

>> Defendants repeatedly built massive short positions through off-exchange trading over a few trading days, and then bombarded the market with spoofing trades (baiting orders canceled within 100 milliseconds of placement) causing significant declines in the price of Genius Group stock.

>> Less than a minute after these baiting orders were placed, Defendants sold significant volumes of Genius stock shortthrough off-exchange trading.

>> Defendants also engaged in significant naked short-selling, i.e., improper short sales that are unsupported by existing market inventory. Indeed, major declines in Genius Group stock were also accompanied by large spikes in evidence of such activity.

In filing this class action, Genius Group is demonstrating its commitment to its shareholders and the Company intends to work diligently to protect their interests.

Full PR - https://t.co/cWXTfMKPWk

These “OpenAI tokens” are not OpenAI equity. We did not partner with Robinhood, were not involved in this, and do not endorse it. Any transfer of OpenAI equity requires our approval—we did not approve any transfer.

Please be careful.